Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| By Grade | Rutile, Anatase | Rutile (72.1% share, 2025) | Anatase (4.65% CAGR) |

| By Process | Chloride, Sulfate | Sulfate (59.5% share, 2025) | Chloride (4.89% CAGR) |

| By Application | Paints & Coatings, Plastics, Paper & Pulp, Cosmetics, Other Applications | Paints & Coatings (55.8% share, 2025) | Plastics (4.67% CAGR) |

| By End-User Industry | Titanium Dioxide Market, Automotive & Transportation, Packaging, Other Industries | Titanium Dioxide Market (40.3% share, 2025) | Packaging (4.78% CAGR) |

| By Geography | Asia-Pacific, Europe, North America, South America, Middle East & Africa | Asia-Pacific (37.4% share, 2025) | Asia-Pacific (5.16% CAGR) |

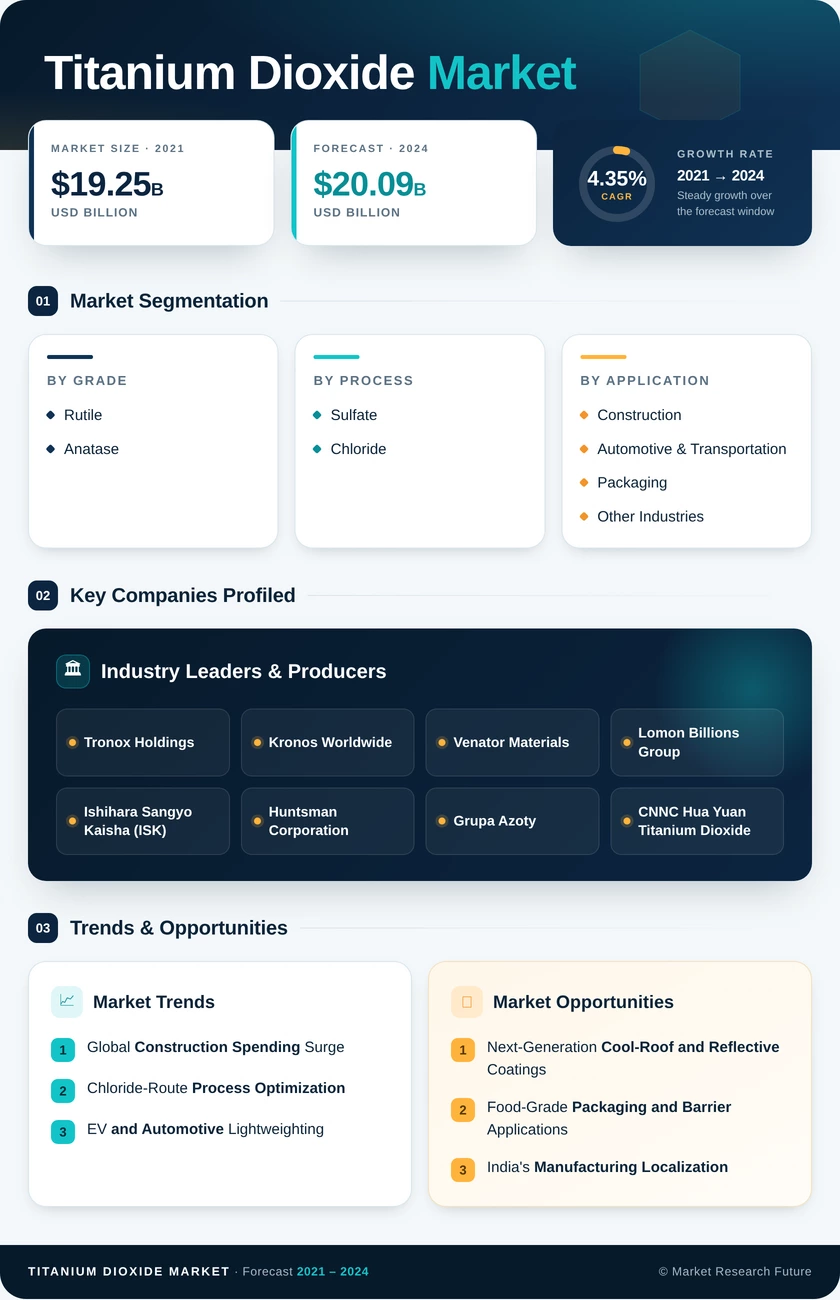

Market Segmentation Overview

By Grade

| Sub-Segment | Key Trend |

| Rutile | Preferred for exterior architectural and automotive coatings due to superior weathering resistance and opacity |

| Anatase | Growing in paper coatings, food-contact packaging, and mineral sunscreen formulations |

Rutile remains the workhorse grade across paint, plastics, and industrial applications, while anatase is establishing itself in niche sectors where softer abrasion characteristics and cost efficiency outweigh pure durability requirements.

By Process

| Sub-Segment | Key Trend |

| Chloride | Expanding share driven by lower environmental footprint and premium-grade output quality |

| Sulfate | Dominant by installed capacity, especially across China's large-scale production facilities |

The chloride-sulfate process split defines the competitive structure of global titanium dioxide manufacturing, with Western producers favoring chloride technology and Asian producers leveraging sulfate-route cost advantages.

By Application

| Sub-Segment | Key Trend |

| Paints & Coatings | Largest application, driven by architectural and industrial maintenance demand cycles |

| Plastics | Fastest-growing application, propelled by EV lightweighting and flexible packaging |

| Paper & Pulp | Stable demand for printability and barrier properties in specialty papers |

| Cosmetics | Rising demand for mineral UV filters replacing chemical sunscreen actives |

| Other Applications | Includes catalysts, ceramics, textiles, and food-grade uses |

Paints and coatings continue to anchor more than half of global titanium dioxide consumption. Still, the plastics segment is gaining ground as automotive electrification and packaging modernization create new demand vectors.

By End-User Industry

| Sub-Segment | Key Trend |

| Titanium Dioxide Market | Largest end-user, tied to global urbanization and infrastructure stimulus |

| Automotive & Transportation | Transitioning toward EV-specific coatings and lightweight polymer applications |

| Packaging | Fastest-growing end-user, driven by food-safety regulations and flexible film demand |

| Other Industries | Includes furniture, marine, aerospace, and specialty industrial applications |

Titanium Dioxide Market's outsized share reflects titanium dioxide's fundamental role in architectural coatings, while packaging's rapid growth trajectory signals diversification beyond traditional paint-centric demand.

By Geography

| Sub-Segment | Key Trend |

| Asia-Pacific | Dominant producer and consumer; China's production base and India's localization drive regional leadership |

| Europe | Regulatory-driven innovation in encapsulated and dust-free product formats |

| North America | Mature market sustained by residential renovation and cool-roof mandates. |

| South America | Infrastructure catch-up cycle, particularly in Brazil's construction and packaging sectors |

| Middle East & Africa | Emerging demand from Vision 2030 mega-projects and heat-reflective building coatings |

Asia-Pacific's combined production capacity and consumption volumes make it the gravitational center of global titanium dioxide trade, though Europe and North America retain technology leadership in chloride-process manufacturing and specialty product development.