Toilet Paper Market Summary

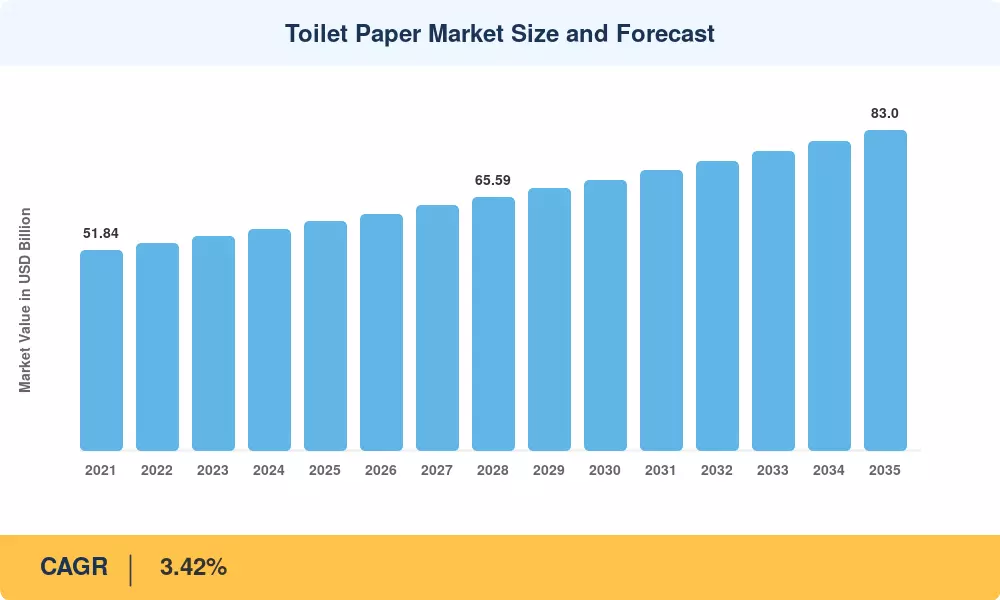

The global toilet paper market reached an estimated USD 59.30 billion in 2025 and is projected to grow from USD 61.33 Billion in 2026 to USD 83.00 billion by 2035, registering a CAGR of 3.42% during 2026–2035. Two structural forces anchor this trajectory: expanding sanitation infrastructure across South and Southeast Asia backed by government hygiene campaigns worth over USD 12 billion collectively [2], and steady private-label penetration in mature retail channels that is reshaping pricing dynamics across Europe and North America [3]. The toilet paper market continues to benefit from consumption patterns that are remarkably recession-resistant, making it one of the most stable verticals in consumer staples.

A quiet transformation is underway in toilet paper pulp and fiber production. Legacy virgin-pulp supply chains—built around boreal softwood sourcing in Canada and Scandinavia—are being challenged by recycled and bamboo toilet paper alternatives that offer comparable softness at lower environmental cost. Investment in bamboo fiber processing capacity topped USD 2.4 billion globally between 2022 and 2025, with China and Vietnam accounting for roughly 60% of new capacity additions [4]. The EU's updated Ecolabel criteria for tissue products, effective from mid-2024, now require a minimum 70% certified-sustainable fiber content, accelerating the shift from virgin to recycled inputs across European converters [5]

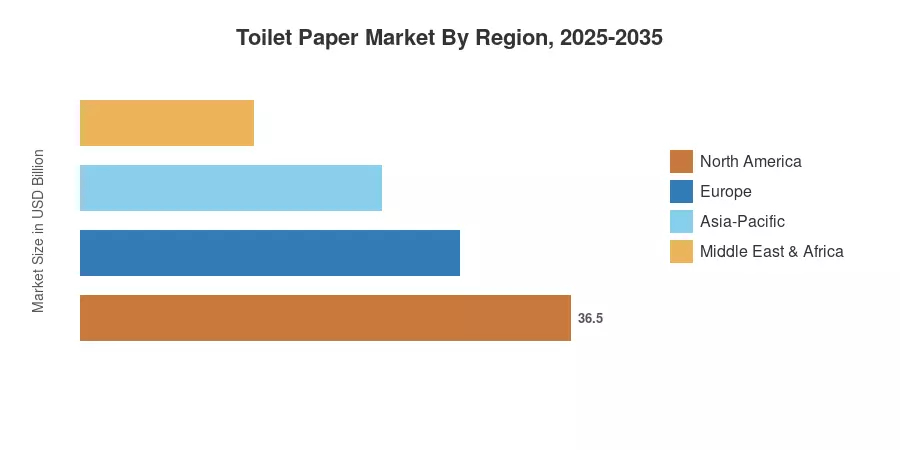

North America held approximately 37.1% of the toilet paper market in 2025, driven by per-capita consumption rates that exceeded 25 kg annually in the United States. Asia-Pacific represents the fastest-growing region with a forecast CAGR of 5.47% through 2035, as urbanization and rising disposable incomes push bathroom tissue and soft paper adoption deeper into tier-2 and tier-3 cities across India and Indonesia. Europe retained the second-largest share at 27.5%, supported by premiumization toward multi-ply premium toilet tissue variants. The decade ahead will reward companies that balance cost-efficient fiber sourcing with sustainability credentials and digital distribution agility.

Key Report Takeaways

• By Product Type

- Rolled formats accounted for 70.2% of the toilet paper market revenue share in 2025, reflecting entrenched consumer preference across all regions.

- Folded tissue is forecast to grow at a 4.62% CAGR through 2035, driven by commercial and hospitality demand for disposable formats.

• By Material Source

- Recycled fiber held 49.5% share of the toilet paper market in 2025, supported by cost advantages and tightening sustainability mandates.

- Bamboo and alternative fibers are expected to register the fastest segment CAGR of 5.34% through 2035.

• By End-User

- Household consumption represented 60.7% of the toilet paper market size in 2025.

- Commercial procurement is advancing at a 4.93% CAGR, boosted by post-pandemic capacity rebuilds in offices, airports, and hospitality venues.

• By Distribution Channel

- Offline retail outlets retained 50.4% share of the toilet paper market in 2025.

- Online channels are projected to expand at a 5.05% CAGR as subscription-based delivery models gain traction.

• By Region

- North America contributed 37.1% of the toilet paper market share in 2025.

- Asia-Pacific is on track for the fastest regional CAGR at 5.47% through 2035.

Market Size and Forecast (2021–2035)

Market estimates combine top-down revenue analysis of publicly listed tissue manufacturers with bottom-up tracking of production volumes across 32 countries. Historical figures (2021–2024) are calibrated against national trade databases, customs data, and manufacturer disclosures. Forecast projections (2026–2035) use MRFR's proprietary demand-modeling framework that integrates demographic trends, per-capita consumption indices, and raw-material cost trajectories.