Toluene Market Summary

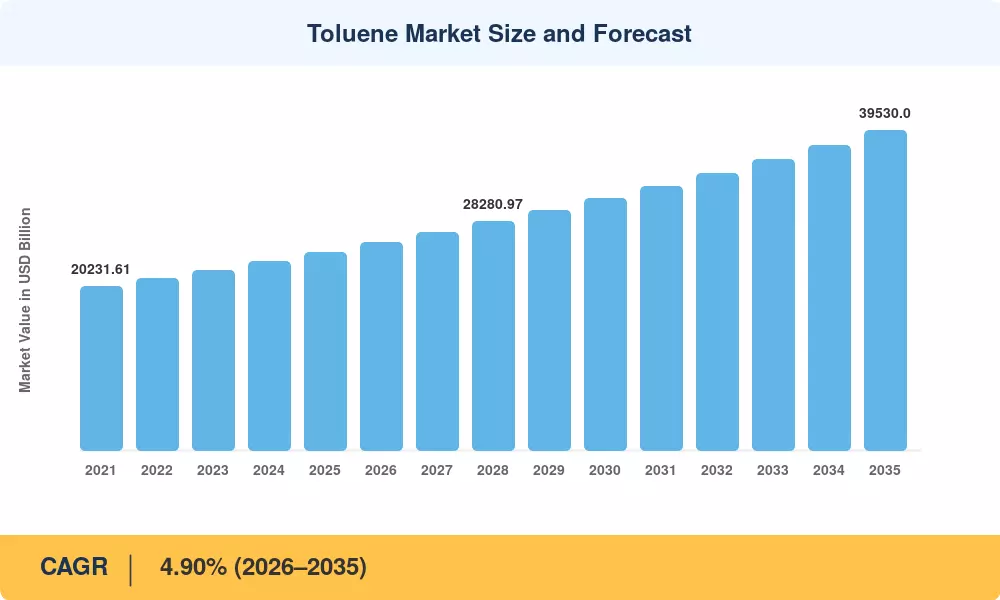

The global Toluene Market stood at USD 24,500 Million in 2025 and is projected to reach USD 25,700 Million in 2026 before climbing to USD 39,530 Million by 2035, registering a CAGR of 4.90% during the forecast period (2026–2035). This expansion is rooted in surging downstream demand for aromatic solvents used in benzene, xylene, and toluene diisocyanate (TDI) production, alongside tightening emissions mandates that compel refiners to upgrade petrochemical processing infrastructure. The U.S. EPA's 2024 revision of National Ambient Air Quality Standards for ozone-forming volatile organic compounds (VOCs) and China's 14th Five-Year Plan allocation of CNY 180 billion toward green chemical manufacturing are two concrete policy catalysts driving capital flows into cleaner toluene production technologies [2][3].

Legacy distillation and catalytic reforming units across aging refinery complexes are giving way to advanced hydrodealkylation and selective disproportionation systems. These technologies yield higher purity industrial solvents while reducing energy intensity by 12–18% per ton of output, according to the International Energy Agency's 2024 Petrochemicals Roadmap [4]. The shift is most pronounced in Asia-Pacific and the Middle East, where greenfield investments in integrated aromatics complexes exceed USD 22 billion committed through 2028.

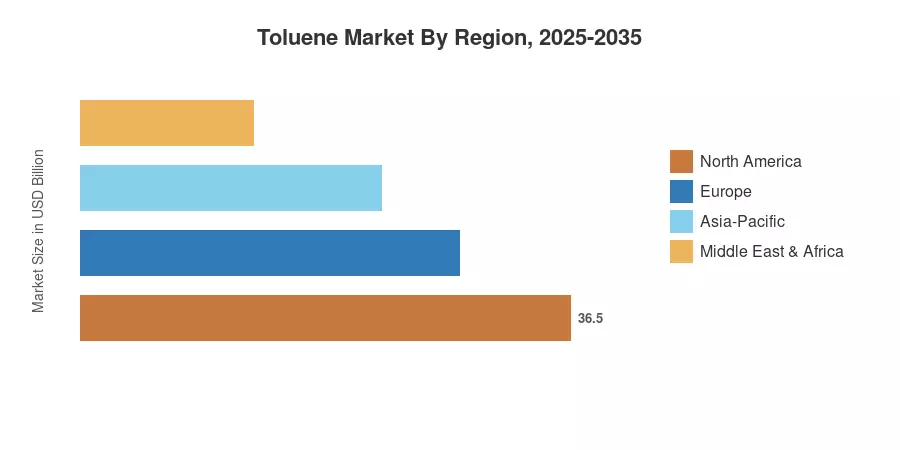

Asia-Pacific commands roughly 50.5% of the Toluene Market, making it the dominant region by a wide margin. It is also the fastest-growing region, expanding at a projected 5.90% CAGR through 2035, fueled by rapid industrialization in India and Southeast Asia North America holds the second-largest share at 20.8%, anchored by shale-derived feedstock advantages and robust chemical processing capacity along the U.S. Gulf Coast. Europe follows closely, where the EU REACH regulation framework continues to shape demand for low-VOC paint and coatings formulations. As downstream industries from automotive to construction intensify their consumption of hydrocarbon compounds, the Toluene Market is positioned for steady structural growth through the next decade.

Key Report Takeaways

• By Derivative

- Benzene and xylene derivatives captured a combined 40.8% revenue share of the Toluene Market in 2025, reflecting their role as primary feedstocks for petrochemical processing chains

- TDI is forecast to expand at a 5.80% CAGR through 2035, driven by polyurethane foam demand in construction and automotive cushioning

• By Application

- The chemical industry accounted for 58.5% of Toluene Market volume in 2025, underscoring toluene's centrality as an intermediate in aromatic solvents production

- Paint and coatings applications are advancing at a 5.15% CAGR, supported by infrastructure spending and rising demand for industrial solvents in protective coatings

• By End-User Industry

- Automotive led end-user demand with a 22.6% share, where toluene serves as a critical fuel additive component and coating solvent

- Construction is the fastest-growing end-user segment at a 5.20% CAGR, propelled by urbanization in Asia-Pacific and green building mandates in Europe

• By Region

- Asia-Pacific captured 50.5% of the Toluene Market in 2025, with China alone representing over half of regional demand

- North America's shale gas advantage sustains competitive feedstock pricing for chemical processing operations

Market Size and Forecast (2021–2035)

MRFR's projections combine bottom-up plant-capacity modeling with top-down demand estimation, triangulated against trade-flow data from UN Comtrade, ICIS, and proprietary refinery throughput surveys. Historical data (2021–2024) reflects actual production and trade volumes; forecast data (2026–2035) applies the calibrated 4.90% CAGR with adjustments for identified capacity additions and regulatory phase-ins.

.webp?v=1783672314)