Torque Sensor Market Summary

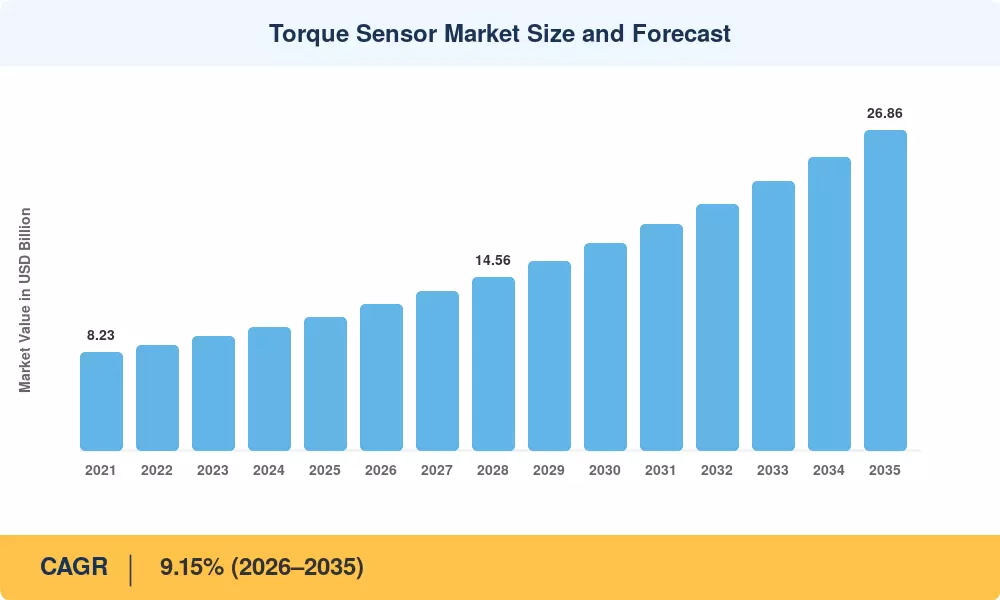

The Torque Sensor Market was valued at USD 11.20 billion in 2025, with the forecast period opening at USD 12.22 billion in 2026 and reaching an estimated USD 26.86 billion by 2035 at a compound annual growth rate of 9.15%. Two structural forces are propelling the expansion: the global shift toward electrified vehicle powertrains — which now require continuous torque feedback for steering, braking, and drivetrain calibration — and Industry 4.0 mandates that tie machine-health monitoring directly to production quality targets. Government EV incentive programs across the EU, China, and the United States have collectively committed over USD 120 billion in subsidies and tax credits through 2030, each generating downstream sensor demand [1][2].

Legacy mechanical coupling-based measurement is giving way to digital, wireless, and magnetoelastic sensing platforms that deliver higher bandwidth and electromagnetic-interference resilience. Collaborative-robot installations surpassed 80,000 units globally in 2024, and each cobot typically embeds two to six torque sensing elements — a content-per-machine ratio that barely existed five years ago [3]. Predictive-analytics integration has further shifted the value proposition from raw accuracy toward data-rich, network-ready sensor architectures.

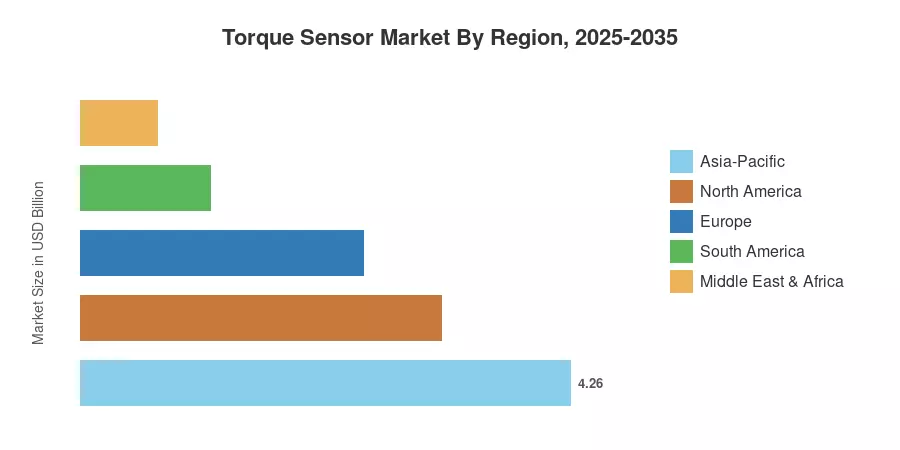

Asia-Pacific commands roughly 38% of the Torque Sensor Market, underpinned by automotive production clusters in China, Japan, and South Korea. South America is the fastest-growing region with an expected 10.1% CAGR, driven by expanding EV assembly in Brazil and Argentina. North America follows with approximately 28% share, supported by aerospace test-stand investment and reshoring of precision-manufacturing capacity. As electrification spreads into micromobility, marine propulsion, and surgical robotics, the addressable Torque Sensor Market will widen considerably through 2035.

Key Report Takeaways

• By Product Type

- Rotational torque sensors held approximately 60% of the Torque Sensor Market in 2025, reflecting dominance in automotive and industrial drivetrain applications

- Reaction torque sensors are on track for a 12.0% CAGR through 2035, fueled by cobot and medical-device calibration demand

• By Technology

- Strain-gauge devices accounted for roughly 45% of revenue in 2025, anchored by OEM test-stand standardization

- Surface acoustic wave sensors are poised for the fastest technology-level CAGR at approximately 11.85%

• By Application

- Automotive represented about 44.5% of the Torque Sensor Market in 2025, led by electric power-steering and ADAS integration

- Medical and healthcare robotics will expand at roughly 12.4% CAGR through 2035, the quickest application segment

• By End-User Industry

- OEM test-stand and QA operations captured around 41% of the Torque Sensor Market in 2025

- In-process monitoring is growing at an estimated 12.5% CAGR, reflecting real-time quality-assurance adoption

• By Region

- Asia-Pacific led with 38% share in 2025; South America is projected to record the fastest regional CAGR of 10.1%

Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework combines bottom-up revenue modeling from supplier shipments, top-down cross-referencing against industrial-automation CapEx databases, and primary interviews with OEM procurement leads. Historical figures (2021–2024) are validated against customs-trade data and published annual reports; forecast values (2026–2035) apply a calibrated CAGR of 9.15%.