Tractors Market Summary

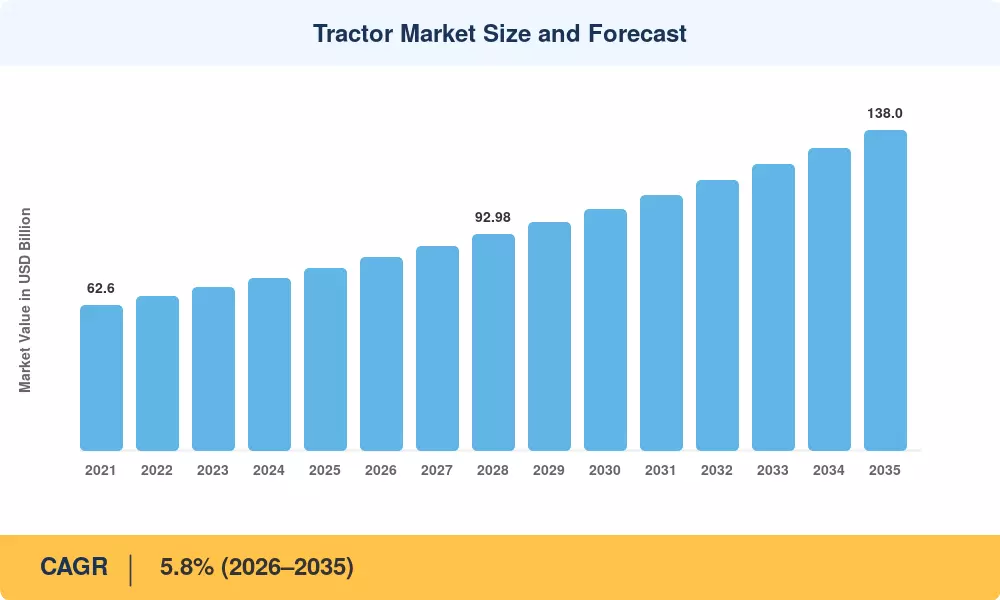

The global Tractor Market stood at an estimated USD 78.5 billion in 2025 and is projected to reach USD 138.0 billion by 2035, expanding at a CAGR of 5.8% during the 2026–2035 forecast window. This growth trajectory is anchored in two converging forces: the mechanization push across South and Southeast Asian agriculture—where India's Sub-Mission on Agricultural Mechanization (SMAM) alone disbursed over USD 480 million in subsidies between 2022 and 2025 [1]—and the fleet-replacement cycle underway in North America and Europe, where emissions-stage mandates (EU Stage V, EPA Tier 4 Final) are accelerating retirement of legacy diesel powertrains [2].

A technology shift is redefining what a tractor can do. Conventional mechanical-linkage machines are giving way to platforms integrated with satellite guidance, variable-rate implements, and real-time data telemetry. Deere & Company invested over USD 1.2 billion in precision-agriculture R&D between 2022 and 2024, while CNH Industrial acquired Raven Industries specifically to embed autonomy into its Case IH and New Holland lines [3]. Electric and hybrid drivetrains, still below 2% of unit sales, drew more than USD 600 million in venture and OEM capital commitments during 2023–2024 alone [4].

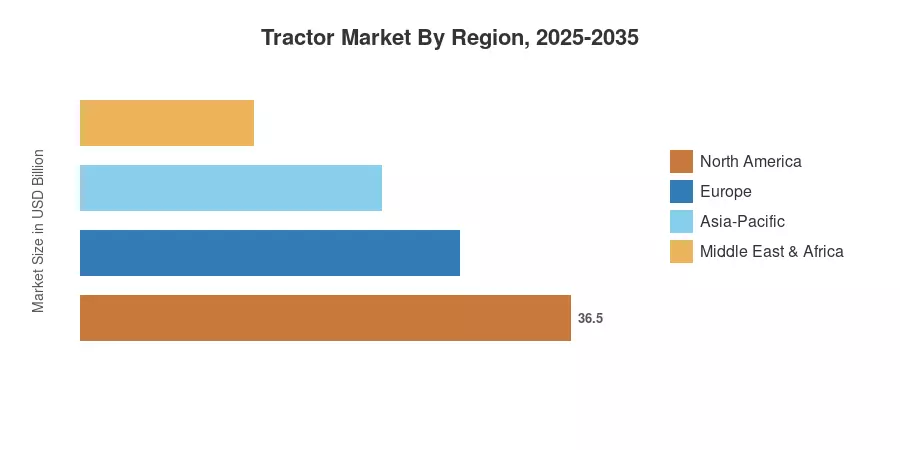

Asia-Pacific dominates the Tractor Market with roughly 42% revenue share, driven by India (the world's largest tractor-selling nation) and China's aggressive rural modernization programs. North America accounts for approximately 25% of global value, anchored by high-horsepower row-crop demand. Europe holds around 22%, with specialty and orchard segments growing steadily. As farm labor shortages intensify globally, the Tractor Market is poised for its most transformative decade since the diesel transition of the mid-twentieth century.

Key Report Takeaways

• By Type

- Utility tractors (40–100 HP) command roughly 38% of the Tractor Market by revenue, reflecting broad applicability across mixed-farming operations worldwide.

- Row-crop tractors (100–200+ HP) are forecast to grow at a CAGR of 6.4% through 2035, propelled by precision-agriculture adoption in grain-belt economies.

- Compact and sub-compact tractors represent a USD 11.2 billion segment in 2025, expanding through lifestyle-acreage and municipal demand.

• By Drive Type

- Four-wheel-drive platforms hold an estimated 54% unit share in the Tractor Market, reflecting the shift toward higher-traction field operations.

- Autonomous and electric tractor platforms are projected to register the fastest segment CAGR at 14.5% through 2035.

• By Region

- Asia-Pacific's dominance in the Tractor Market is reinforced by India's 900,000+ annual tractor unit sales.

- North America contributes approximately USD 19.6 billion in 2025 value, with the U.S. accounting for over 78% of regional revenue.

- Europe's Tractor Market benefits from CAP subsidy reform, incentivizing smart-farming equipment upgrades.

Tractor Market Size and Forecast (2021–2035)

Data for the historical period (2021–2024) is sourced from OEM revenue disclosures, national agricultural-equipment associations (AEM, FederUnacoma, TMA India), and customs trade databases. Forecast values (2026–2035) are generated using a bottom-up, segment-level build validated against macroeconomic agricultural-output projections from the FAO and World Bank [5].