Trade Surveillance Systems Market Summary

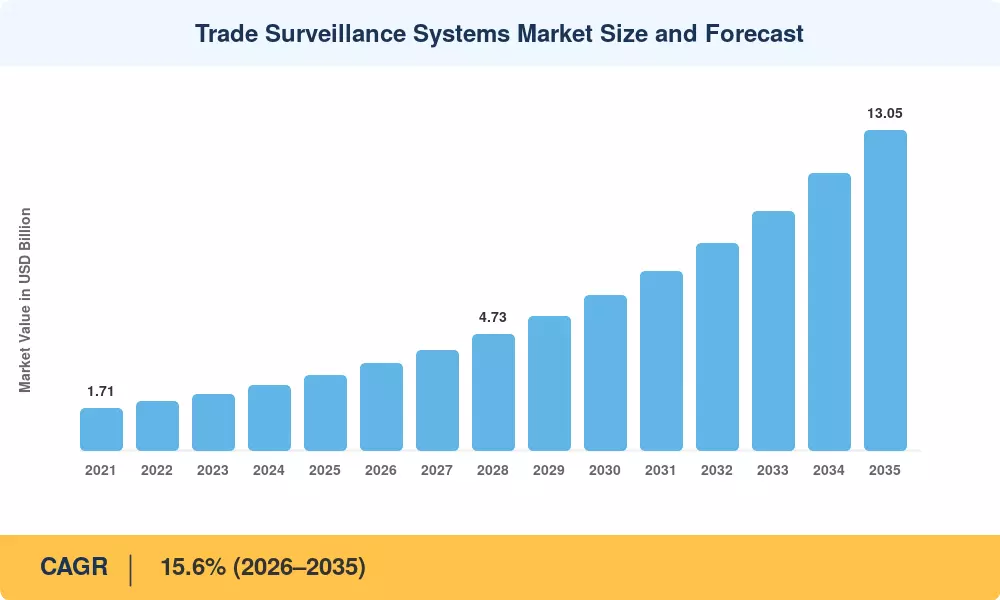

The Trade Surveillance Systems Market reached USD 3.06 billion in 2025 and is projected to grow from USD 3.54 billion in 2026 to USD 13.05 billion by 2035, registering a CAGR of 15.6% during the forecast period. Two policy-level catalysts underpin this expansion: the United States' Consolidated Audit Trail (CAT), which now ingests more than 58 billion order events daily across equity and options markets [1], and the European Securities and Markets Authority's ongoing MiFID II reporting revisions, which extended real-time transaction monitoring to systematic internalizers and organized trading facilities in late 2024 [2]. Institutions that once relied on end-of-day batch reviews are shifting budgets toward platforms capable of processing upwards of 150,000 transactions per second with sub-millisecond alert latency.

AI-driven architectures that include natural language processing, graph analytics, and reinforcement learning are replacing legacy rule-based engines, reducing false positives by up to 40% when compared to earlier generations of systems [3]. According to a poll, major sell-side banks allotted an expected USD 12.5 billion to compliance technology upgrades in 2024, with market manipulation detection capabilities ranking among the top three investment priorities [4]. This change is being accelerated by cloud-native installations, which provide mid-tier companies access to institutional-grade surveillance without requiring multimillion-dollar infrastructure expenditures.

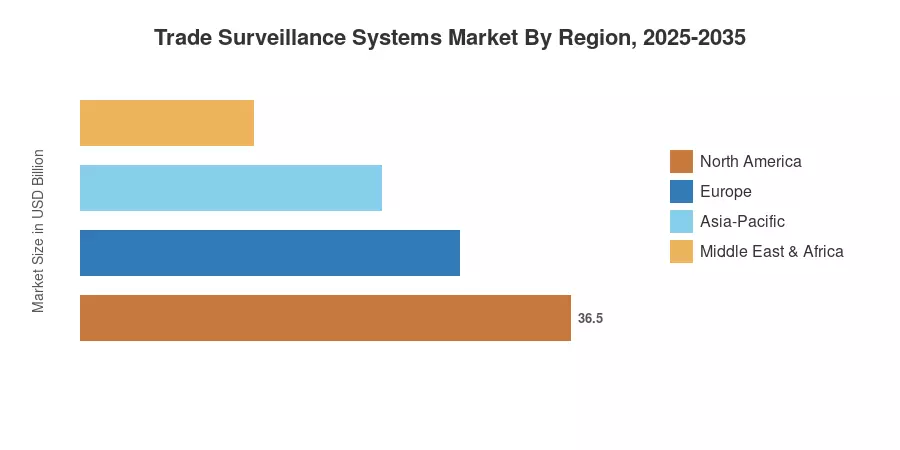

With 36.5% of worldwide revenue, North America has the greatest regional share thanks to FINRA's growing cross-market surveillance mandate and the SEC's strict enforcement stance. The fastest-growing region is Asia-Pacific, which is expected to develop at a compound annual growth rate (CAGR) of 19.0% through 2035 as regulators in South Korea, Japan, and India tighten control over digital asset exchanges and derivatives. Due to changing EMIR and MAR rules, Europe has the second-largest proportion. The market for trade surveillance systems is expected to increase steadily in double digits as financial markets become more intricate, digitized, and closely monitored.

Key Report Takeaways

• By Component

- Solutions dominated the Trade Surveillance Systems Market with a 57.2% revenue share in 2025, reflecting demand for integrated analytics engines and dashboard toolkits.

- Services are forecast to expand at a 19.4% CAGR through 2035 as managed surveillance and professional consulting engagements gain traction among mid-tier firms.

• By Deployment

- Cloud deployment is projected to grow at a 20.5% CAGR from 2026 to 2035, outpacing on-premise installations as hybrid architectures address data-sovereignty concerns.

• By Trading Type

- Equities accounted for 34.6% of the Trade Surveillance Systems Market in 2025, driven by high-frequency trading volumes and regulatory scrutiny of order-book manipulation.

- Buy-side institutions record the highest end-user CAGR at 19.6%, as asset managers internalize compliance functions previously outsourced to prime brokers.

• By Region

- North America held a 36.5% share of the Trade Surveillance Systems Market in 2025, anchored by SEC and CFTC enforcement activity.

- Asia-Pacific exhibits the fastest regional CAGR of 19.0%, led by SEBI's algorithmic-trading surveillance framework in India and Japan's Financial Instruments and Exchange Act amendments.

Market Size and Forecast (2021–2035)

Market Research Future estimates are derived from a bottom-up methodology combining vendor revenue disclosures, regulatory spending surveys, and financial institution IT budget analyses. Historical values (2021–2024) are calibrated against audited annual reports and SIFMA/World Federation of Exchanges data, while forecast figures employ a compound growth model anchored to identified drivers and restraint offsets.