Transfection Reagents And Equipment Market Summary

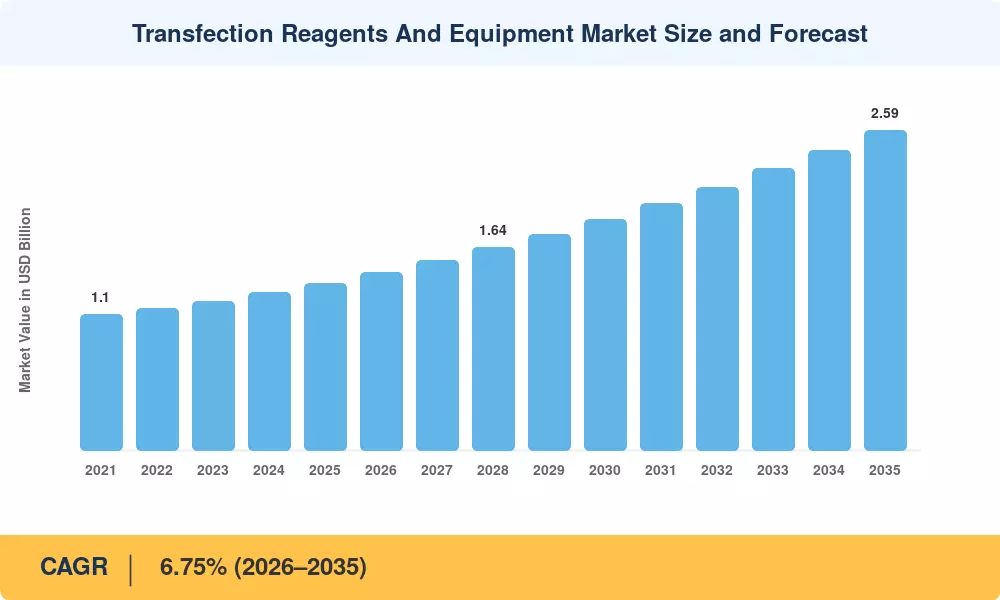

The Global Transfection Reagents and Equipment Market size was valued at USD 1.35 Billion in 2025, and the market is projected to grow from USD 1.44 Billion in 2026 to USD 2.59 Billion by 2035, registering a CAGR of 6.75% during the forecast period 2026–2035. This expansion draws its primary fuel from the global surge in approved cell and gene therapies — the U.S. FDA cleared seven new gene therapy products between 2023 and early 2025 alone — alongside sustained R&D investment by pharmaceutical companies racing to commercialize mRNA-based vaccines and oncology therapeutics [2]. Governments in both North America and Europe have earmarked combined public funding exceeding USD 4.2 billion for advanced therapy medicinal product (ATMP) infrastructure since 2022, creating a durable demand floor for transfection-grade reagents and automated delivery platforms [3].

The technology landscape is shifting decisively. Legacy calcium-phosphate and DEAE-dextran protocols are giving way to lipid nanoparticle formulations, high-throughput electroporation systems, and microfluidic platforms that offer batch-to-batch reproducibility at commercial scale. Novartis, BioNTech, and several CDMO partners collectively invested over USD 1.8 billion in GMP transfection capacity expansions during 2023–2024, signaling confidence in the pipeline depth behind these technologies.

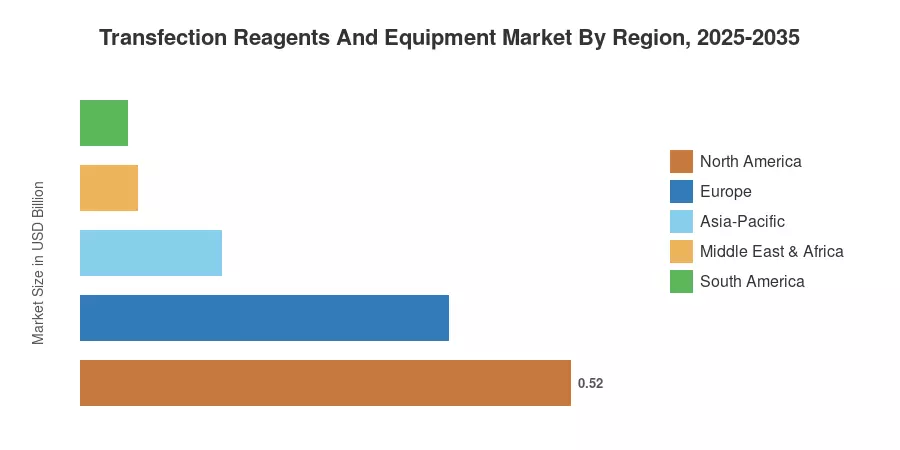

North America commands roughly 38.4% of the transfection reagents and equipment market, anchored by a dense cluster of biopharma manufacturing sites and NIH-funded academic programs. Asia-Pacific is the fastest-growing region at an estimated 10.8% CAGR, propelled by China's biosimilar build-out and India's vaccine manufacturing ambitions. Europe holds the second-largest share at approximately 28.7%, supported by EMA's harmonized ATMP regulatory pathway [5]. As gene-editing modalities move from preclinical to pivotal trials, demand for validated transfection solutions will intensify through the mid-2030s.

Key Report Takeaways

• By Product

- Reagents held 68.4% of the transfection reagents and equipment market in 2025, driven by recurring consumable demand in academic and commercial laboratories.

- The equipment segment is growing at a 13.5% CAGR through 2035 as facilities invest in automated electroporation and microfluidic platforms.

• By Method

- Viral methods accounted for 45.2% of transfection reagents and equipment market share in 2025, reflecting their dominance in clinical-grade gene therapy manufacturing.

- Physical methods are advancing at a 15.5% CAGR, led by next-generation electroporation devices that eliminate viral vector supply constraints.

• By Application

- Protein production represented 32.1% of the transfection reagents and equipment market in 2025.

- Cell and gene therapy manufacturing is the fastest-growing application at a 16.1% CAGR, reflecting an expanding clinical pipeline.

• By Region

- North America leads the transfection reagents and equipment market with a 38.4% share, underpinned by concentrated biopharma manufacturing and federal research grants.

- Asia-Pacific registers a 10.8% CAGR, the highest among all regions, fueled by biosimilar capacity expansion in China and India.

Market Size and Forecast (2021–2035)

Market Research Future compiled this dataset through triangulation of manufacturer revenue disclosures, trade association shipment data, CDMO capacity filings, and primary interviews with procurement directors at 42 biopharma facilities. Historical figures (2021–2024) reflect audited outcomes; the 2025 base year blends preliminary revenue data with confirmed contract volumes. Forecast estimates (2026–2035) apply a compound growth model calibrated against pipeline progression rates and regulatory approval timelines.