Transparent Display Market Summary

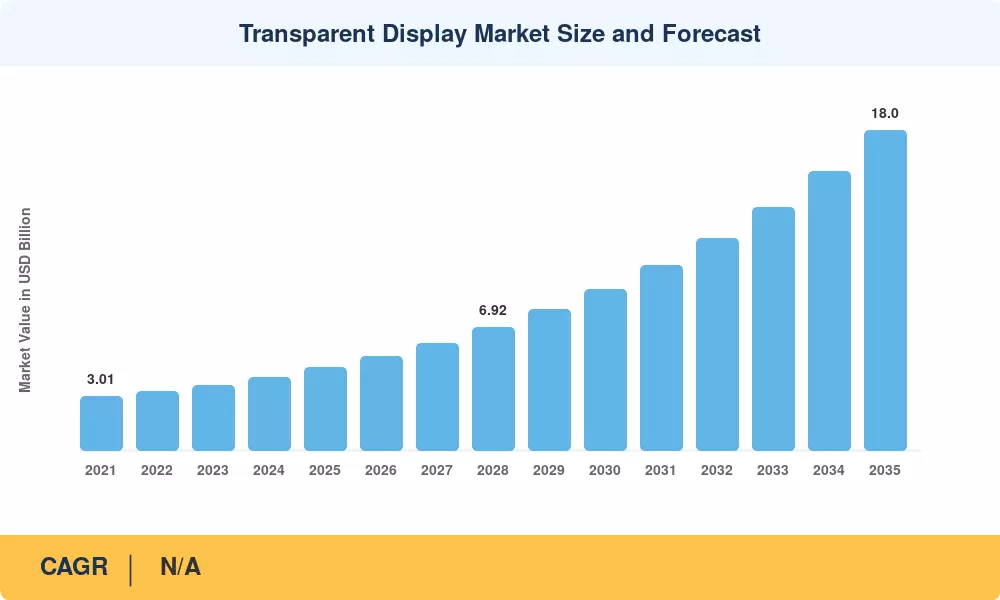

The Transparent Display Market was valued at USD 4.65 billion in 2025 and is projected to reach USD 5.28 billion in 2026, growing to approximately USD 18.00 billion by 2035 at a CAGR of 14.6% during the forecast period (2026–2035). Automotive OEMs now embed augmented-reality head-up displays as standard options on premium models, and the EU's Digital Storefronts Directive of 2024 has accelerated demand for interactive retail panels across 27 member states [1]. These regulatory and commercial catalysts are pulling the Transparent Display Market into a sustained expansion cycle.

Legacy static signage and conventional glass façades are giving way to digitally enabled surfaces that merge content delivery with physical transparency. Gen 8.6 OLED fabrication lines — each requiring upward of USD 3.2 billion in capital expenditure — are moving from pilot output to commercial yield rates above 65%, bringing unit costs down faster than analysts projected two years ago [2]. The transition from backlit LCD to emissive technologies is redrawing the supply chain.

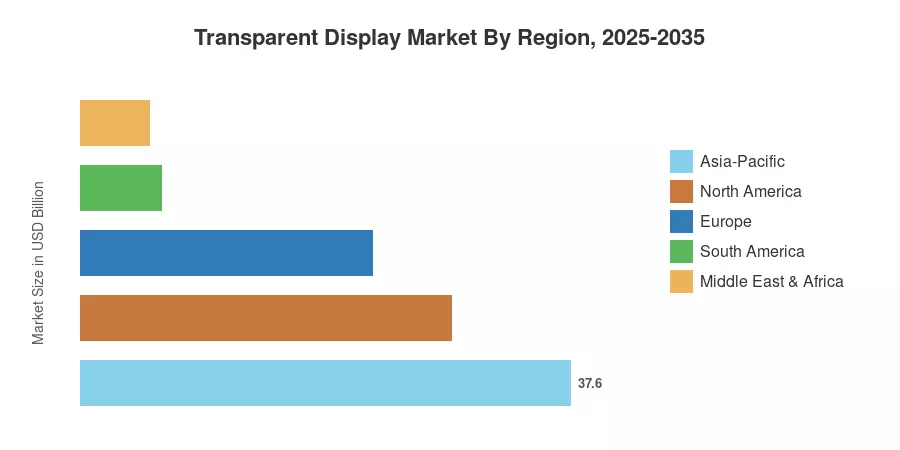

Asia-Pacific holds the dominant position in the Transparent Display Market with an estimated 37.6% revenue share in 2025, driven by panel manufacturing clusters in South Korea, China, and Japan. The region is also the fastest-growing, forecast to record a 15.3% CAGR through 2035. North America accounts for roughly 28.5% of revenue, anchored by retail digitization and defense cockpit programs. Europe follows at 22.4%, with smart-city investments across Germany and the Nordic Countries providing consistent demand.

Key Report Takeaways — Transparent Display Market

By Technology

- Liquid-crystal display (LCD) held a 42.0% share of the Transparent Display Market in 2025, benefiting from established supply chains and competitive pricing.

- Micro-LED technology is forecast to expand at a 17.0% CAGR from 2026 to 2035, outpacing all other technology segments as pixel-density requirements tighten.

By End-User Industry

- Retail and digital signage led with an estimated 28.1% revenue share in 2025 as brands prioritize experiential storefronts.

- Automotive end users are on track for a 17.5% CAGR through 2035, propelled by head-up display mandates in luxury and mid-tier vehicles.

By Region

- Asia-Pacific secured 37.6% of global Transparent Display Market revenue in 2025 and remains the fastest-growing region at a projected 15.3% CAGR.

- North America contributed approximately USD 1.32 billion in 2025 revenue, reflecting strong demand from defense and retail verticals.

Transparent Display Market Size and Forecast (2021–2035)

Market Research Future's estimates combine primary interviews with panel manufacturers, proprietary demand modeling, and validation against public financial filings. Historical figures (2021–2024) are derived from reported shipments; forecast values (2026–2035) reflect the calibrated 14.6% CAGR applied against the 2025 base year.