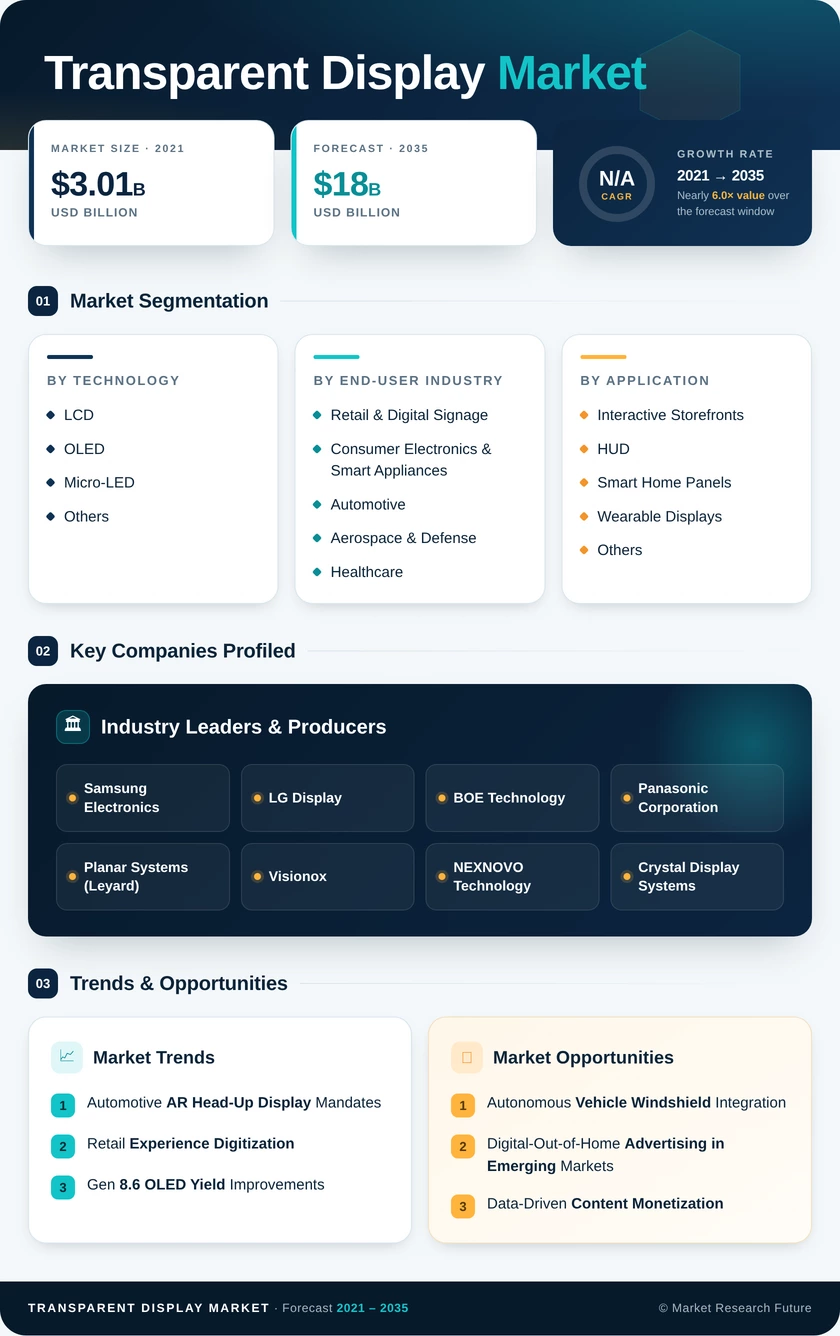

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment (2025) | Fastest Growing Segment (2026–2035) |

| Technology | LCD, OLED, Micro-LED, Others | LCD | Micro-LED |

| End-User Industry | Retail & Digital Signage, Consumer Electronics & Smart Appliances, Automotive, Transparent Display Market, Healthcare | Retail & Digital Signage | Automotive |

| Application | Interactive Storefronts, HUD, Smart Home Panels, Wearable Displays, Others | Interactive Storefronts | Head-Up Displays (HUD) |

| Display Size | Less Than 10 Inches, 10–39 Inches, 40 Inches and Above | 40 Inches and Above | 40 Inches and Above |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | Asia-Pacific | Asia-Pacific |

Market Segmentation Overview

By Technology

| Sub-Segment | Key Trend |

| LCD | Cost-driven adoption in high-volume retail signage |

| OLED | Premium positioning in automotive and luxury retail |

| Micro-LED | Rapid brightness and lifespan gains driving commercial interest |

| Others (E-Paper, Electroluminescent) | Low-power niche applications in harsh environments |

LCD remains the workhorse technology for large-scale transparent signage deployments, while OLED serves premium verticals demanding superior contrast and flexibility. Micro-LED is rapidly closing the cost gap and is expected to surpass OLED in revenue share by the early 2030s as die-transfer yields improve.

By End-User Industry

| Sub-Segment | Key Trend |

| Retail & Digital Signage | Omnichannel strategies driving interactive storefront investment |

| Consumer Electronics & Smart Appliances | Smart-home hubs and transparent refrigerator panels |

| Automotive | AR head-up display integration across luxury and mid-tier vehicles |

| Transparent Display Market | Transparent cockpit canopy modernization programs |

| Healthcare | Operating theater and cleanroom visualization overlays |

Retail remains the anchor demand segment, but automotive is closing fast. Defense procurement cycles are longer but contract values per unit are significantly higher, providing stable revenue contributions across the forecast horizon.

By Application

| Sub-Segment | Key Trend |

| Interactive Storefronts | Experiential commerce and pedestrian engagement |

| Head-Up Displays (HUD) | Safety regulation incentives and autonomous driving convergence |

| Smart Home Panels | IoT integration and ambient computing |

| Wearable Displays | AR glasses miniaturization |

| Others | Industrial process monitoring, museum installations |

Interactive storefronts command the largest share today due to rapid deployment timelines and high advertiser ROI. Head-up displays represent the fastest growth path as automotive OEMs move from concept to series production.

By Display Size

| Sub-Segment | Key Trend |

| Less Than 10 Inches | Wearable devices and compact instrument clusters |

| 10–39 Inches | Appliance panels, automotive HUD, point-of-sale |

| 40 Inches and Above | Large-format retail, transit, and architectural installations |

Large-format panels above 40 inches dominate revenue because per-unit prices are substantially higher and replacement cycles extend to 7–10 years. Sub-10-inch panels are growing in unit volume as AR eyewear and smartwatch categories expand, though revenue contribution remains modest relative to large-format installations.

By Geography

| Sub-Segment | Key Trend |

| North America | Defense and luxury retail driving premium demand |

| Europe | Automotive OEM integration and smart-city programs |

| Asia-Pacific | Panel manufacturing dominance and smart-city rollouts |

| South America | Transit advertising and organized retail expansion |

| Middle East & Africa | Mega-project construction and tourism infrastructure |

Asia-Pacific leads both in production capacity and consumption, supported by government digitization initiatives and the world's largest OLED and Micro-LED fabrication base. North America and Europe follow as mature demand markets with strong verticals in defense, automotive, and premium retail.