Tungsten Carbide Market Summary

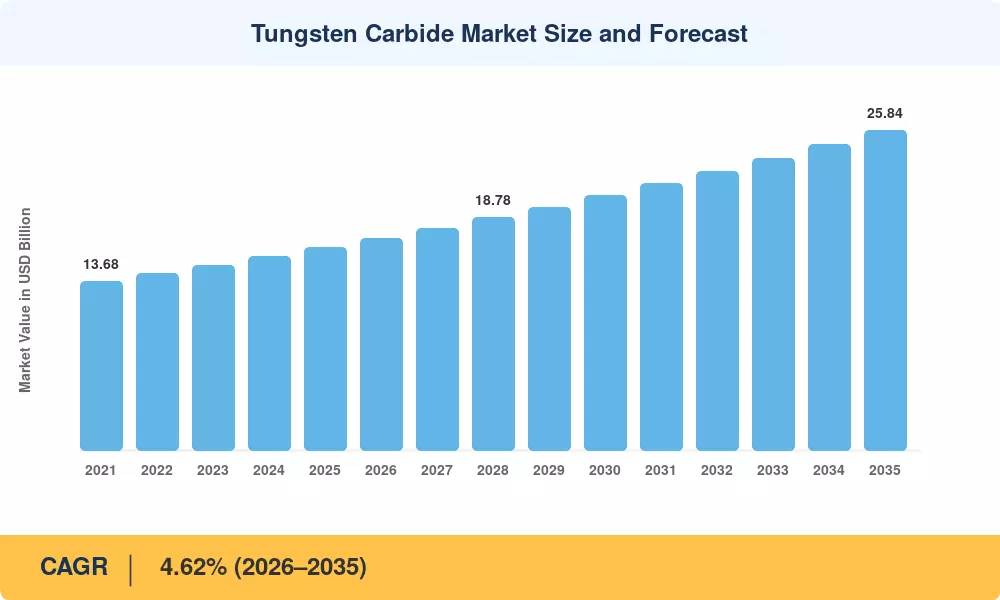

The Tungsten Carbide Market reached an estimated USD 16.38 billion in 2025, with forecasts projecting a rise from USD 17.14 billion in 2026 to USD 25.84 billion by 2035, expanding at a CAGR of 4.62% over the forecast period. Two catalysts anchor this trajectory: first, surging capital expenditure in global mining and construction — the World Bank estimates USD 2.4 trillion in annual infrastructure spending across developing economies through 2030 [2] — and second, defense rearmament budgets that now exceed USD 2.2 trillion globally, fueling demand for high-hardness materials in munitions, armor-piercing inserts, and precision cutting equipment [3].

A technology shift is changing the way cemented carbide materials reach end customers. Legacy single-layer coated inserts are being replaced with multilayer PVD and CVD stacks, doubling or tripling tool life and halving per-unit consumption costs, even while raw carbide powder volumes increase. The 2024 Critical Minerals Strategy of the U.S. Department of Defense planned USD 439 million for local tungsten processing, reflecting a wider strategy to de-risk supply chains away from Chinese concentrate [4]. At the same time, South Korea’s Ministry of Trade established a KRW 1.2 trillion subsidy scheme for the manufacturing of wear-resistant materials and strong metal alloys through 2028 [5].

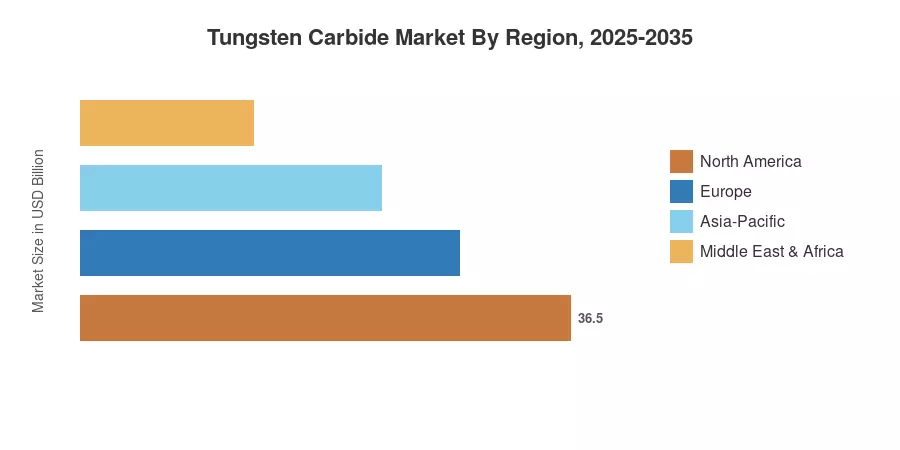

Asia-Pacific dominates around 55% of the Tungsten Carbide Market, with China alone producing more than 60% of the worldwide tungsten concentrate output. North America is the second-largest region with a share of about 19%. This growth is due to the high demand for industrial carbide tools in automotive and aerospace machining. Europe is not far behind, increasing at a competitive rate since the EU Critical Raw Materials Act demands recycling objectives for cutting tool materials exceeding 25% by 2030 [6]. In the next decade, enterprises that balance price-competitive sourcing of carbide powder with tariff-insulated, controlled supply corridors will be rewarded.

Key Report Takeaways

• By Product Type

- Cemented carbide held approximately 64% of the Tungsten Carbide Market in 2025, reinforced by its dominance in metal machining tools and mining applications

- Coatings are on track for the fastest growth at a 5.78% CAGR through 2035, as multilayer PVD/CVD technologies extend insert longevity for precision cutting equipment

- Alloys contributed USD 2.14 billion in 2025, anchored in wear-resistant materials demand from oil and gas drilling

• By Application

- Mining and construction led the Tungsten Carbide Market with a 35% share in 2025, driven by global infrastructure capex and rising hard rock extraction volumes

- Aerospace and defense will expand at a 5.61% CAGR through 2035, supported by rearmament spending and next-generation turbine blade tooling

- Automotive applications generated approximately USD 3.28 billion in 2025, tied to EV powertrain machining and lightweight component finishing

• By Geography

- Asia-Pacific dominated the Tungsten Carbide Market at roughly 55% share in 2025, led by China's integrated mine-to-insert supply chain

- North America is projected to grow at a 4.48% CAGR through 2035, spurred by reshoring initiatives and defense procurement of mining tool materials

- Europe accounted for USD 2.79 billion in 2025, with Germany and the Nordics driving demand for high hardness materials in automotive tooling

Tungsten Carbide Market Size and Forecast (2021–2035)

Market Research Future (MRFR) market sizing involves conducting primary interviews with carbide powder manufacturers, cutting tool OEMs, and distributors of mining equipment in 22 countries. The data obtained from these interviews is validated through trade flow databases (UN Comtrade, USGS Mineral Commodity Summaries) and public financial statements of the top 15 cemented carbide material producers. Historical statistics (2021-2024) are actuals; 2025 is the base-year estimate; 2026-2035 are forecast estimates at a calibrated CAGR of 4.62%.