Ultra WideBand Market Summary

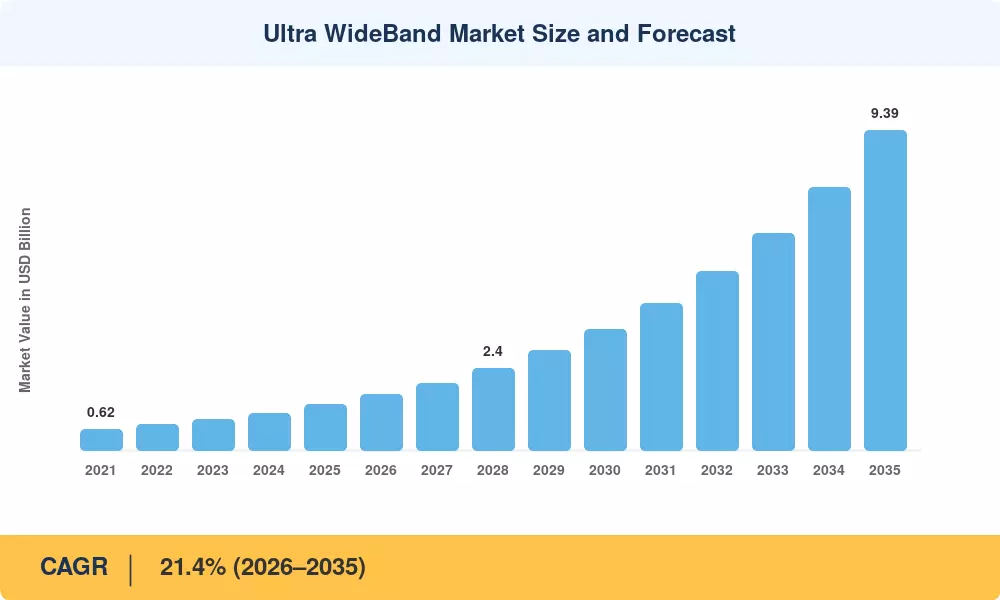

The Ultra-WideBand Market reached a valuation of USD 1.34 billion in 2025 and is projected to grow from USD 1.64 billion in 2026 to USD 9.39 billion by 2035, registering a CAGR of 21.4% across the forecast period (2026–2035). Two catalysts are accelerating this trajectory: European Union Decision 2024/1467, which doubled permissible outdoor UWB range and eliminated provincial certification bottlenecks, and China's MIIT spectrum rules that freed the 7.2–8.5 GHz band for commercial positioning deployments. Combined, these regulatory shifts unlocked large-scale infrastructure rollouts that had previously stalled at the pilot stage [1][2].

A significant technological revolution is currently in progress. The centimeter-level accuracy of UWB is gaining ground in factory automation, port logistics, and digital-key authentication, as legacy Bluetooth Low Energy angle-of-arrival systems, which were previously sufficient for meter-level indoor tracking, are losing ground. Fleet-leasing insurers reduced premiums by up to 12% for vehicles equipped with UWB-based passive-entry systems. In comparison, manufacturers reported a 30–40% reduction in forklift-collision insurance claims when they implemented sub-10-centimeter tracking [3]. Bill-of-materials costs have been reduced to below USD 0.85 per module in high-volume consumer designs as a result of the combined efforts of Apple's second-generation U2 chip, NXP's Trimension platform, and Qorvo's DW3000 family [4].

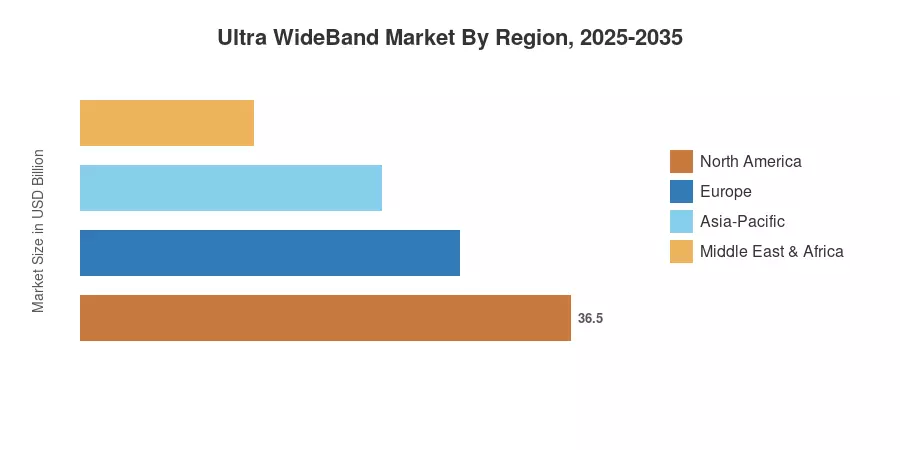

Apple's ecosystem integration and enterprise real-time location system (RTLS) deployments in healthcare and logistics are the primary drivers of North America's approximately 36% share of the global Ultra-WideBand Market revenue. Propelled by the adoption of smartphone OEMs in China and South Korea, as well as smart-factory mandates under India's Production Linked Incentive scheme, the Asia-Pacific region is the fastest-growing region, with an estimated CAGR exceeding 23%. The Car Connectivity Consortium's automotive digital-key standardization is the primary factor driving Europe's second-largest share, which is approximately 28%. The Ultra-WideBand Market is currently at a critical juncture, where the convergence of regulatory clarity, silicon cost reductions, and expanding end-use cases is expected to propel sustained double-digit growth through 2035.

Key Report Takeaways

• By Component

- Hardware accounted for roughly 66.5% of the Ultra-WideBand Market revenue in 2025, reflecting strong chipset and module demand from consumer electronics and automotive OEMs.

- The services segment is poised to register the highest CAGR through 2035, underpinned by managed RTLS deployments and location-as-a-service platforms expanding across warehousing and healthcare.

• By End-User Vertical

- Consumer electronics held an estimated 29.4% revenue share in the Ultra-WideBand Market during 2025, led by smartphone integration and personal item trackers.

- Smart buildings represent the fastest-expanding vertical, driven by regulatory mandates for occupancy analytics and energy optimization in commercial real estate.

• By Region

- North America retained its dominant position with the largest revenue contribution, supported by robust enterprise RTLS adoption and Apple's U.S.-centric supply chain.

- Asia-Pacific is forecast to grow at the steepest CAGR through 2035, fueled by smartphone OEM integration in China and South Korea and India's expanding smart-factory ecosystem.

Market Size and Forecast (2021–2035)

Market Research Future derived historical estimates (2021–2024) from semiconductor shipment data, OEM integration disclosures, and patent-filing velocity analysis. Forecast values (2026–2035) apply a calibrated compound annual growth model validated against chipset production roadmaps, regulatory timelines, and enterprise adoption surveys from 52 countries.