Vascular Closure Devices Market Summary

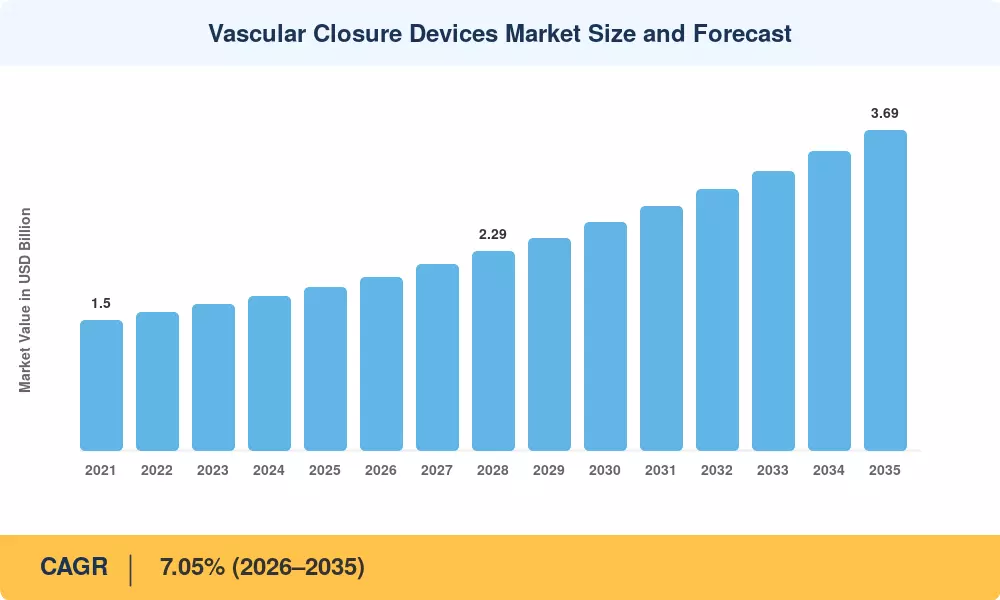

The Vascular Closure Devices Market size was valued at USD 1.88 Billion in 2025, and the market is projected to grow from USD 2.00 Billion in 2026 to USD 3.69 Billion by 2035, registering a CAGR of 7.05% during the forecast period 2026–2035. That trajectory is anchored less to a single catalyst than to a convergence of two: the FDA's continued clearance pace for large-bore access closure platforms supporting transcatheter aortic valve replacement (TAVR), and CMS outpatient payment expansions that have pulled a meaningful share of elective catheterization volume into ambulatory settings. Hospitals and cath labs alike are responding by standardizing device-based closure over manual compression, particularly where access sites now routinely approach 22–25 Fr.

Below the headline number is a real technology shift. Active approximator systems and bioabsorbable collagen plugs are gradually supplanting legacy manual and figure-eight suture closure, compressing ambulation time from hours to less than sixty minutes. Industry capital flows mirror the pivot – financing rounds for closure devices and corporate R&D investments are said to have surpassed USD 400 million throughout 2023-2025, with manufacturers racing to reduce deployment time and eliminate operator-dependent variability from large-bore cases.

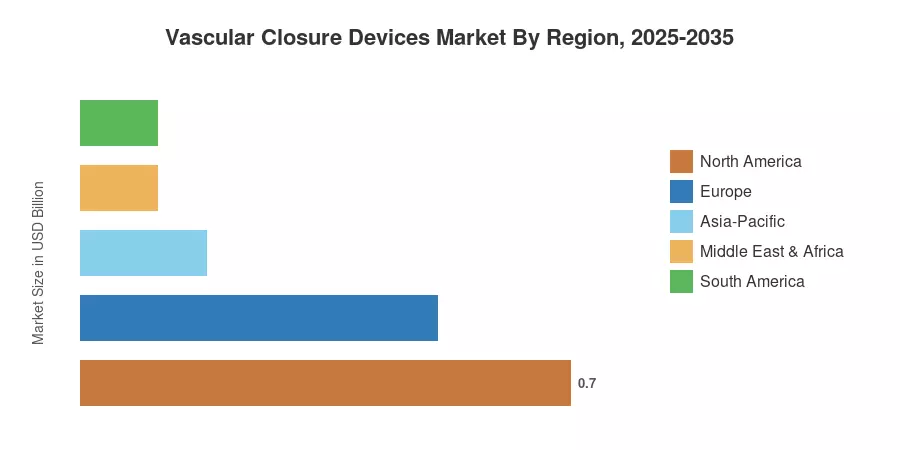

North America accounts for the lion’s share of the Vascular Closure Devices Market, due to its extensive cath lab infrastructure and favorable reimbursement. Asia-Pacific is the fastest-expanding region, with China and India scaling up interventional cardiology capacity. Europe is the second largest contributor after North America, driven by the launch of products compliant with MDR and growth in the structural heart program. As the global expansion of large-bore procedures continues, the gravity center for vascular closure, both competitive and clinical, is poised to shift from the edges of the operating room to the heart of the procedural protocol.

Key Report Takeaways

• By Technology

- Active approximators led the Vascular Closure Devices Market with a 50.6% revenue share in 2025, reflecting clinician preference for mechanical, suture-mediated closure in higher-volume cath labs.

- Passive approximator (collagen plug) systems are forecast to expand at a 7.5% CAGR through 2035 as bioabsorbable formulations gain traction in lower-acuity cases.

- Collagen-based materials accounted for an estimated USD 0.88 billion of the Vascular Closure Devices Market in 2025.

• By Sector

- Interventional cardiology represented 35.2% of procedure-linked demand in 2025, the largest single procedural category.

- Neurovascular procedures are projected to post the fastest segment CAGR, at 9.9% through 2035, as endovascular stroke intervention volumes rise.

- Femoral access sites of 8 Fr or smaller held a 56.3% share in 2025, though large-bore femoral access (≥12 Fr) is the quickest-growing access category.

• By Geography

- North America retained the largest regional position in the Vascular Closure Devices Market in 2025, supported by dense TAVR and EVAR program density.

- Asia-Pacific is forecast to grow at a 9.6% CAGR through 2035, the fastest of any region.

- Hospitals captured a 51.0% end-user share of the Vascular Closure Devices Market in 2025.

Market Size and Forecast (2021–2035)

Figures below are based on a base-year (2025) calibration of USD 1.88 billion, projected forward at a 7.05% CAGR, and reconciled against historical procedural-volume data for 2021-2024. The Vascular Closure Devices Market will see a minor slowdown during 2021-2023 because of the postponement of elective procedures amid the pandemic, with a gradual recovery kicking in from 2024 onwards.