Veterinary/Animal Vaccines Market Summary

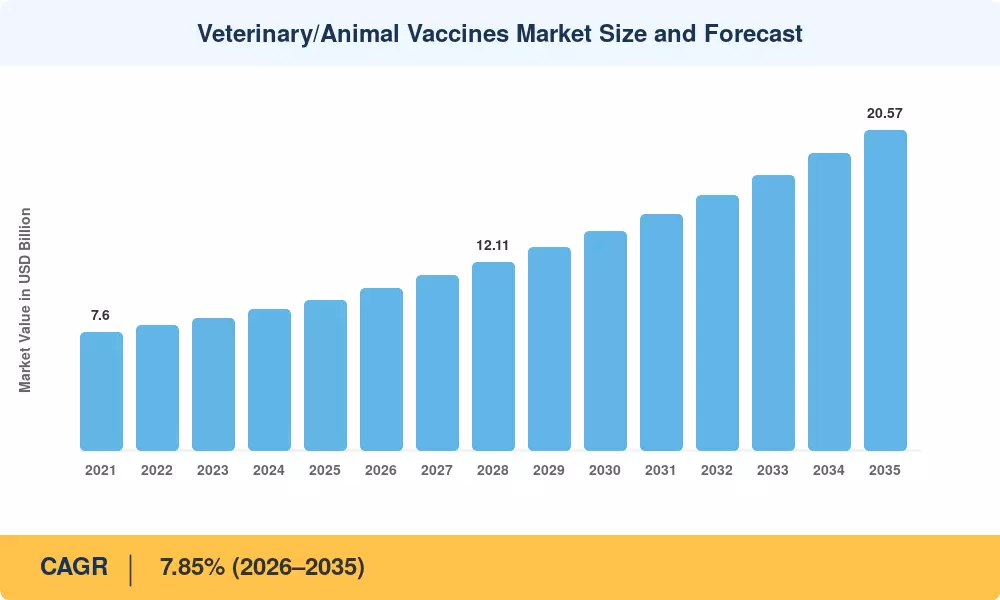

The Veterinary/Animal Vaccines Market size was valued at USD 9.65 Billion in 2025, and the market is projected to grow from USD 10.41 Billion in 2026 to USD 20.57 Billion by 2035, registering a CAGR of 7.85% during the forecast period 2026–2035. Two structural forces are reshaping this trajectory: rising antimicrobial resistance (AMR) has pushed the World Health Organization and the Food and Agriculture Organization to classify preventive immunization as a frontline strategy [1], while recurring outbreaks of highly pathogenic avian influenza (HPAI) and African swine fever (ASF) have converted emergency spending into permanent budget lines across veterinary agencies in the US, EU, and China [2].

Technology-wise, the Veterinary/Animal Vaccines Market is transitioning from conventional killed and live attenuated platforms toward recombinant, DNA, and mRNA vector systems that offer thermostability, multivalent protection, and faster scale-up during panzootic events. The European Medicines Agency's updated guidance on DNA vaccines for veterinary use has accelerated approvals across the continent [3], and the US Department of Agriculture obligated over USD 900 million toward avian influenza preparedness during fiscal years 2024–2025 [4]. These regulatory catalysts, combined with private-sector R&D spending exceeding USD 1.4 billion annually by leading multinationals, signal a platform shift comparable to what the human pharmaceutical sector experienced a decade ago.

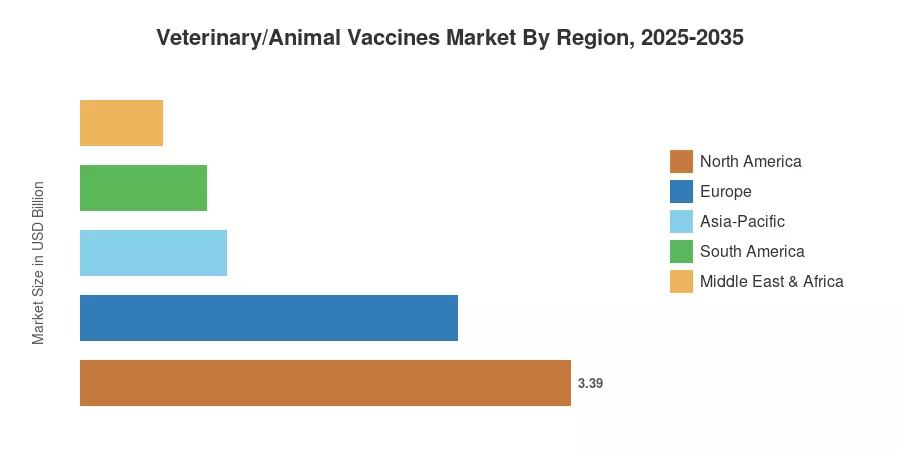

Regionally, North America commanded a 35.1% share of the Veterinary/Animal Vaccines Market in 2025, underpinned by strict USDA vaccination mandates and a large companion-animal population. Asia-Pacific is projected to register the fastest CAGR at 10.50% through 2035, fueled by livestock intensification programs in China and India. Europe held the second-largest share at approximately 27.0%, driven by the EU Animal Health Law's prophylactic vaccination requirements [5]. Over the next decade, convergence of digital livestock management, cold-chain innovations, and expanding e-commerce distribution will redefine how vaccines reach both commercial herds and household pets.

Key Report Takeaways

• By Animal Type

- Livestock vaccines captured 68.0% of revenue share in 2025, driven by mandated vaccination schedules for poultry, swine, and cattle across 140+ countries.

- Companion-animal vaccines are forecast to grow at a 10.62% CAGR through 2035, reflecting increased pet insurance penetration and premiumization of veterinary care.

• By Technology

- Live attenuated platforms held a 54.3% share of the Veterinary/Animal Vaccines Market in 2025, owing to their broad immunogenicity and cost efficiency.

- Recombinant and sub-unit candidates are set to post an 11.67% CAGR through 2035, as thermostable formulations unlock demand in regions with limited cold-chain infrastructure.

• By Region

- North America led with a 35.1% share of the Veterinary/Animal Vaccines Market, backed by USD 900 million in federal outbreak-preparedness allocations.

- Asia-Pacific is projected to achieve a 10.50% CAGR through 2035 as governments in China and India scale national livestock immunization programs.

Veterinary/Animal Vaccines Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated methodology combining bottom-up revenue analysis from company filings, top-down demand modeling using FAO livestock census data, and primary interviews with veterinary procurement officials across 40+ countries. Historical figures (2021–2024) are validated against customs trade databases and national veterinary authority registrations. Forecast projections (2026–2035) apply a scenario-weighted CAGR calibrated to epidemiological trend models and regulatory pipeline analysis.