Video Streaming Software Market Summary

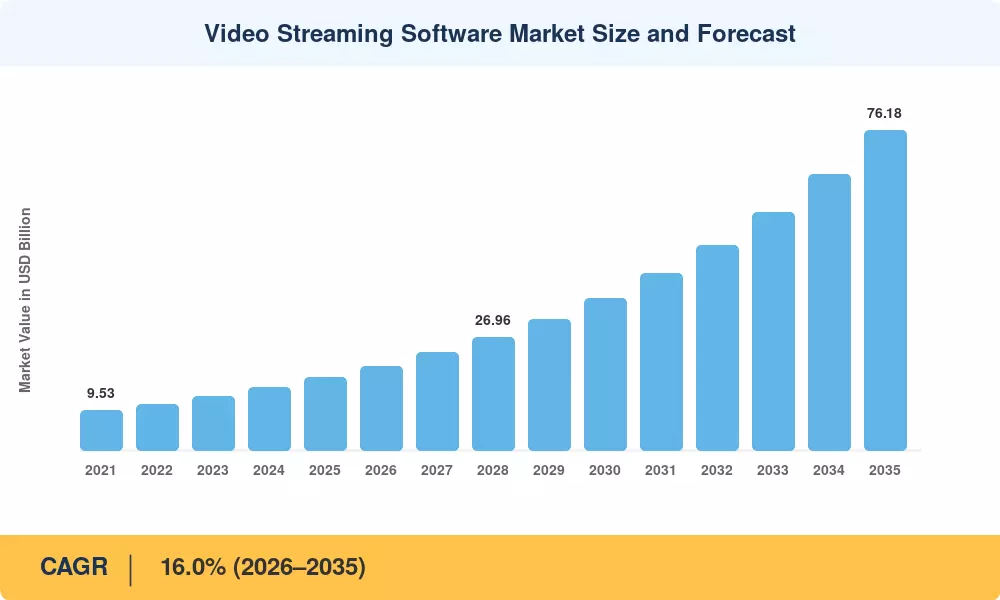

The Video Streaming Software Market reached USD 17.27 billion in 2025 and is projected to grow from USD 20.03 billion in 2026 to USD 76.18 billion by 2035, registering a CAGR of 16.0% during the forecast period. Two catalysts are propelling this expansion: the rapid enterprise shift toward cloud-native video infrastructure and tightening regulatory mandates that require organizations to archive, encrypt, and audit recorded media. The EU's Digital Services Act enforcement timeline, for instance, has pushed broadcasters and platform operators to invest in modular streaming stacks capable of real-time content moderation — a requirement that rigid legacy appliances cannot satisfy [1].

Across industries, monolithic hardware encoders and on-premise media servers are being replaced by programmable, API-first platforms that unify transcoding, content management and viewer analytics into a single SaaS layer. The migration cycle still has a long way to go, and a 2024 poll indicated that 61% of organizations had allocated new cash for browser-based video tools, up from 38% in 2022 [2]. Hospitals, universities and financial services firms no longer see video as a discretionary add-on to communications, but as mission-critical infrastructure.

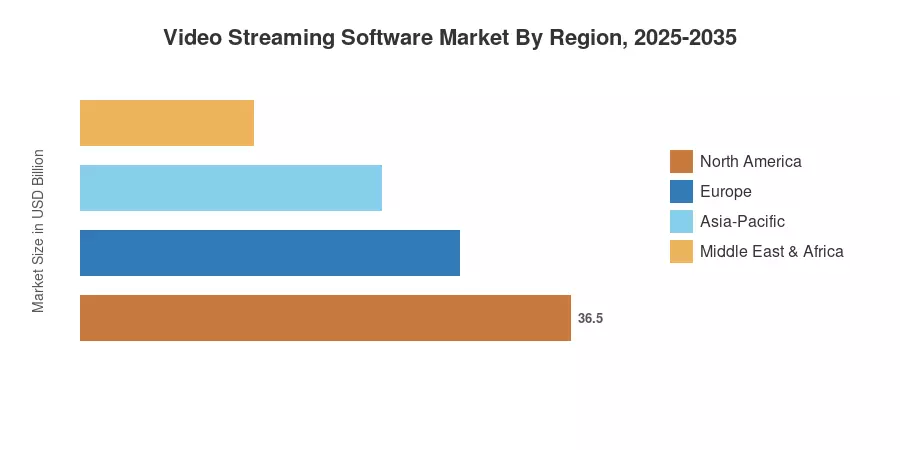

North America dominated the video streaming software market with a revenue share of 40.2% in 2025. This dominance is due to the investment from hyperscalers and a robust advertising-technology ecosystem. Asia-Pacific is the fastest-expanding market with a CAGR of 20.8% expected to be driven by smartphone penetration, affordable mobile data, and government digitization efforts in India, Indonesia, and Vietnam. The second greatest proportion was Europe, helped by GDPR-related data handling rules that are a boon for managed cloud video providers. The Video Streaming Software Market is expected to grow at a steady double-digit rate through 2035 as 5G deployments pick up pace and edge-compute nodes become widely available.

Key Report Takeaways

• By Component

- Solutions accounted for 84.2% of the Video Streaming Software Market share in 2025, reflecting enterprise preference for integrated platform purchases over piecemeal service contracts.

- The services segment is advancing at a 19.5% CAGR through 2035, led by managed encoding, professional integration, and 24/7 support engagements.

• By Streaming Type

- Video-on-demand delivery held 69.0% of the Video Streaming Software Market in minutes delivered during 2025.

- Live streaming is forecast to grow at a 21.8% CAGR, fueled by sports, gaming, and real-time commerce use cases.

• By Vertical

- Media and entertainment commanded 49.5% revenue share in 2025, while healthcare is projected to expand at a 21.5% CAGR — the fastest among tracked verticals.

• By Geography

- North America led with 40.2% of global revenue in 2025.

- Asia-Pacific is on track for a roughly 20.8% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimations combine primary interviews with 240+ industry stakeholders, vendor financial filings and verifiable third-party statistics from. Historical data (2021-2024) are actual revenue filings; projected predictions (2026-2035) are based on a bottom-up segment build-up evaluated against macro demand models. All figures are in USD Billion at the constant 2025 exchange rate.