Voice Prosthesis Devices Market Summary

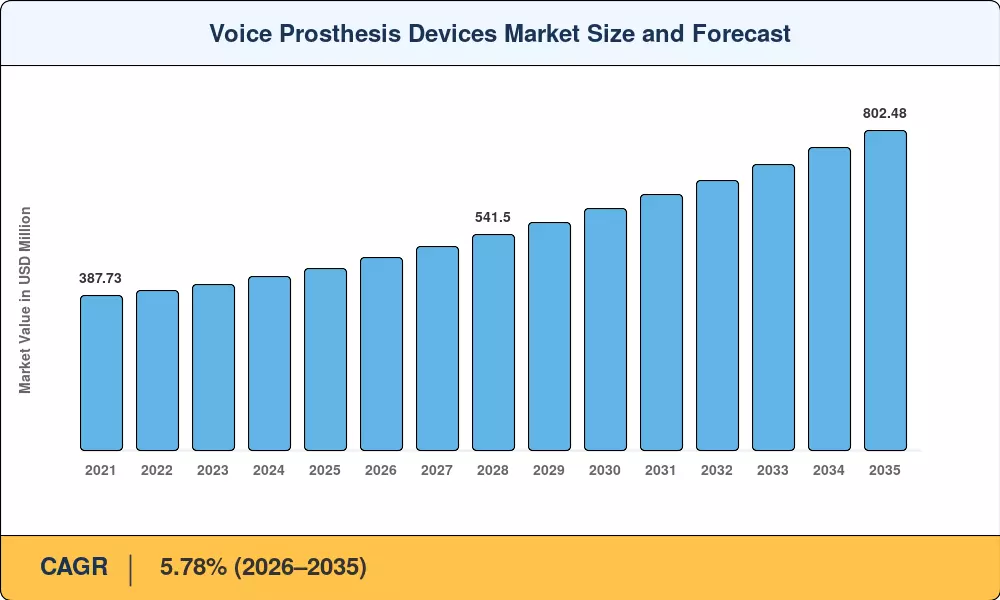

The Global Voice Prosthesis Devices Market size was valued at USD 457.50 Million in 2025, and the market is projected to grow from USD 483.94 Million in 2026 to USD 802.48 Million by 2035, registering a CAGR of 5.78% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the FDA's 2026 alignment of its quality-system regulation with ISO 13485, which compresses multi-region device registration timelines, and expanding reimbursement frameworks across Germany, Japan, and Australia that now cover prosthetic valve replacements on an annualized basis rather than per-episode [1][3]. These structural policy shifts convert what was once a fragmented, out-of-pocket spending category into a recurring, system-funded revenue stream for the Voice Prosthesis Devices Market.

On the technical side, the old school silicone valves with a life span of 60–90 days are being replaced with biofilm-resistant fluoropolymer composites and antimicrobial-coated devices with a life span of 120–180 days. Horizon Europe, the research and innovation programme of the European Commission, funded research into next-generation tracheoesophageal prosthesis with EUR 14 million between 2023 and 2025. Private investments in 3D-printed patient-specific devices in 2024 reached over USD 38 million worldwide [2][5]. This transition lowers the lifetime expenses per patient and prepares the Voice Prosthesis Devices Market for deployment in medium income healthcare systems.

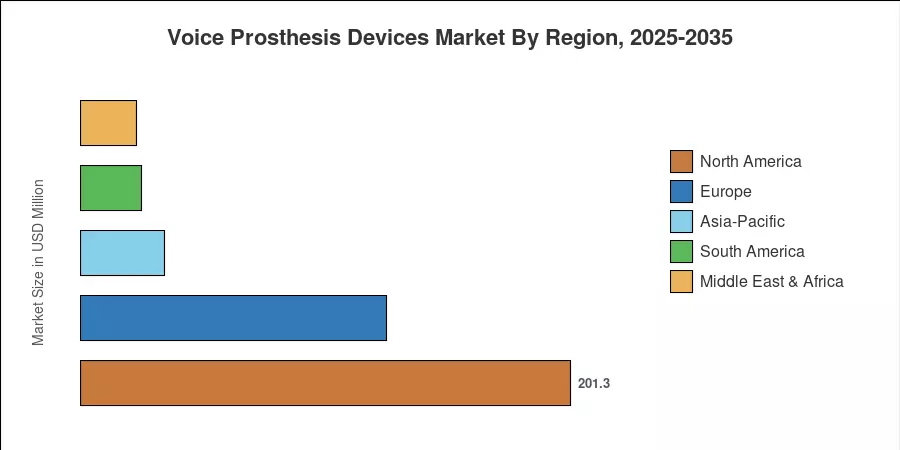

Owing to large laryngectomy procedure volumes and matured insurance coverage, North America held a revenue share of 44.0% in the Voice Prosthesis Devices Market in 2025. The Asia-Pacific region is the fastest expanding with a CAGR of 7.58% through 2035, because of the domestic manufacturing in India and China that reduces the cost of device units by 30–40% than imported ones [4]. Europe’s share is the second biggest at 27.5%, supported by universal healthcare coverage in Scandinavia and Western Europe. The Voice Prosthesis Devices Market is expected to surpass the USD 800 Million mark by the end of this decade as the outpatient ENT settings increase replacement volumes.

Key Report Takeaways

• By Device Type

- Indwelling systems captured 78.0% of the Voice Prosthesis Devices Market share in 2025, reflecting clinician preference for longer-dwelling devices that reduce office visits.

- Non-indwelling systems are advancing at a 6.34% CAGR through 2035, favored in home-care and resource-constrained settings.

• By Valve Type

- Provox Series held a 66.0% revenue share in 2025, benefiting from decades of clinical evidence and speech-language pathologist familiarity.

- Blom-Singer Dual Valve platforms are growing at a 6.72% CAGR, gaining traction in North American ambulatory surgery centers.

• By End User

- Hospitals accounted for 62.0% of the Voice Prosthesis Devices Market in 2025.

- Specialty clinics are expanding at a 7.11% CAGR as ENT procedures migrate to outpatient settings.

• By Regional

- North America led with 44.0% of the Voice Prosthesis Devices Market revenue in 2025.

- Asia-Pacific is projected to grow at a 7.58% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future calibrated historical estimates using device import/export registries, Medicare/Medicaid claims databases, and manufacturer disclosures. Forecast projections apply a compound annual growth model adjusted for regulatory milestone timing, demographic aging curves, and reimbursement expansion schedules across 32 countries [1].

.webp?v=1782120130)