Warehouse management system Market Summary

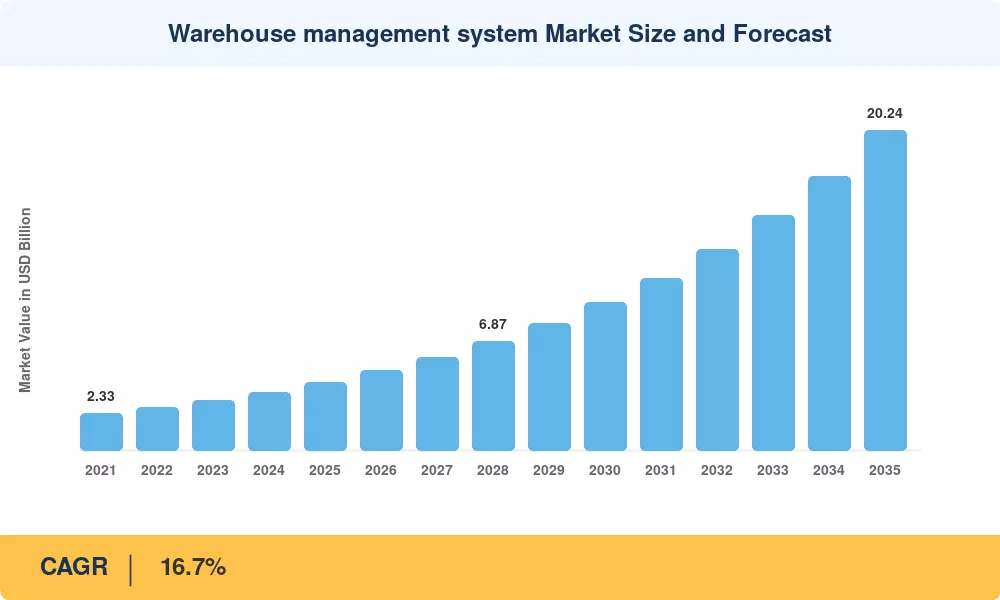

The Warehouse Management System Market reached an estimated USD 4.32 Billion in 2025 and is projected to climb to USD 5.04 Billion in 2026 before expanding to USD 20.24 Billion by 2035, reflecting a 16.7% CAGR across the 2026–2035 forecast window. Two forces underpin this trajectory: the sustained expansion of global e-commerce—cross-border online retail alone grew 26% year-over-year in 2024 [1]—and a structural labor deficit in distribution operations that pushes companies toward software-orchestrated workflows. Government digitization mandates, such as the EU Digital Product Passport regulation slated for phased implementation from 2027, add regulatory urgency to adoption timelines [2].

Legacy spreadsheet-based picking lists and siloed enterprise resource planning modules are giving way to cloud-native, AI-augmented platforms capable of real-time slot optimization and demand-sensing replenishment. Capital investment in the Warehouse Management System Market accelerated sharply after 2022; BloombergNEF tracked over USD 8.7 Billion in logistics-tech venture funding during 2023–2024, a sizable share of which targeted inventory orchestration and warehouse automation software [3]. Predictive analytics engines embedded within modern platforms can lift inventory accuracy by roughly 30%, cutting carrying costs and improving fill rates simultaneously [4].

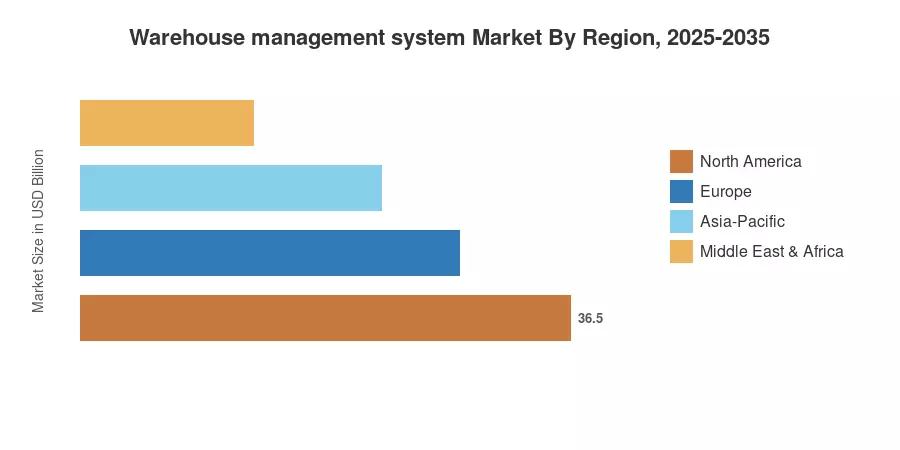

North America commands the largest regional share at 38.1% of the Warehouse Management System Market, driven by mature third-party logistics networks and early cloud adoption. Asia-Pacific is the fastest-growing region with a projected 20.1% CAGR through 2035, fueled by China's smart-logistics corridors and India's expanding organized retail footprint. Europe holds the second-largest share, supported by stringent traceability standards in food, pharmaceutical, and automotive supply chains. As omnichannel fulfillment complexity deepens globally, the Warehouse Management System Market is positioned for a decade of sustained double-digit growth.

Key Report Takeaways

• By Deployment Type

- Cloud-based platforms accounted for 59.1% of the Warehouse Management System Market in 2025, as subscription pricing lowers capital barriers for mid-market operators.

- On-premises deployments continue to serve defense and pharmaceutical verticals where data sovereignty requirements limit cloud migration.

• By Component

- Services captured an 85.6% revenue share in 2025, reflecting the labor-intensive implementation, customization, and managed-services engagements that accompany enterprise roll-outs.

- The software sub-segment is forecast to register an 18.1% CAGR through 2035 as vendors shift to SaaS licensing.

• By Tier Type

- Tier 1 advanced solutions held 38.5% of the Warehouse Management System Market in 2025, chosen by multinational retailers and 3PL conglomerates running multi-site operations.

- Tier 2 intermediate solutions are projected to grow at a 19.4% CAGR, appealing to regional distributors upgrading from spreadsheet-based control.

• By End-User Industry

- Manufacturing represented 32.3% of the Warehouse Management System Market in 2025, driven by just-in-time inventory requirements and parts-kit sequencing.

- Transportation and logistics are set to post a 19.6% CAGR as 3PL operators digitize multi-client operations.

• By Region

- North America led the Warehouse Management System Market with 38.1% revenue share in 2025, anchored by large-scale fulfillment investments from retailers and e-commerce platforms.

- Asia-Pacific is expected to register a 20.1% CAGR through 2035, with China, India, and ASEAN driving demand.

Market Size and Forecast (2021–2035)

Market Research Future's estimates blend proprietary primary surveys of WMS vendors and end-users with secondary validation from logistics-industry databases, company filings, and third-party analyst benchmarks. Historical values (2021–2024) reflect actual reported revenues adjusted for exchange-rate fluctuations; forecast values (2026–2035) apply a calibrated compound growth model tied to the macro drivers discussed in Section 4.