Water Quality Sensor Market Summary

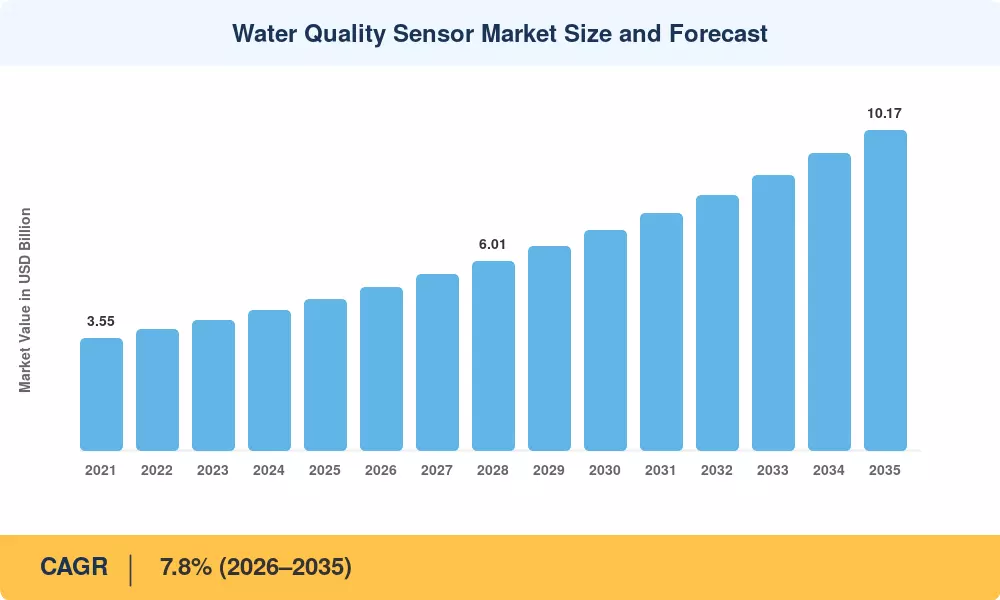

The Water Quality Sensor Market reached an estimated USD 4.80 billion in 2025 and is projected to grow from USD 5.17 billion in 2026 to USD 10.17 billion by 2035, registering a CAGR of 7.8% during the forecast period. Two catalysts are accelerating this trajectory: the U.S. EPA's revised Lead and Copper Rule Improvements (LCRI), which mandate enhanced monitoring at over 66,000 community water systems [2], and the European Union's recast Drinking Water Directive (2020/2184), requiring member states to deploy real-time IoT water quality monitoring networks across all large suppliers by 2026 [3]. Together, these policy mandates are converting what was once a periodic sampling exercise into continuous, sensor-driven surveillance.

Legacy grab-sample workflows — where technicians collect water in bottles and ship them to centralized labs — are rapidly giving way to online water quality analyzer installations that deliver turbidity pH dissolved oxygen sensor readings every few seconds. The World Bank's USD 2.7 billion commitment to water infrastructure in South Asia and Sub-Saharan Africa between 2023 and 2027 specifically earmarks a portion for multiparameter water quality sensor probe deployment at distribution end-points [4]. Portable handheld water quality sensor devices are also gaining traction in decentralized monitoring where piped infrastructure remains incomplete.

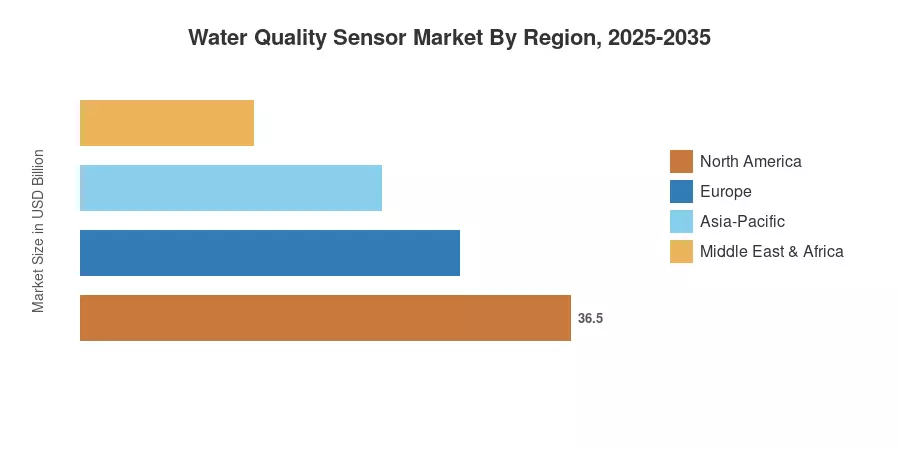

North America commands the largest share of the Water Quality Sensor Market at approximately 34%, driven by stringent Safe Drinking Water Act (SDWA) compliance. Asia-Pacific is the fastest-growing region with a projected CAGR of 9.6%, fueled by China's "14th Five-Year Plan" water pollution controls and India's Jal Jeevan Mission. Europe holds the second-largest share near 28%, anchored by the EU Water Framework Directive. These regional dynamics suggest the Water Quality Sensor Market will remain structurally diversified through 2035.

Key Report Takeaways

• By Technology

- Optical sensing technology — encompassing turbidity pH dissolved oxygen sensor systems — holds the leading revenue share of approximately 38% in the Water Quality Sensor Market, driven by low maintenance and multi-analyte capability

- Electrochemical sensors are forecast to register the fastest CAGR of 8.9%, reflecting rising demand for nitrate phosphate water quality sensor probes in agricultural run-off monitoring

- Digital multiparameter water quality sensor probe platforms represent a USD 1.22 billion segment in 2025, as utilities consolidate single-parameter devices into unified digital architectures

• By Application

- Municipal drinking water treatment constitutes approximately 31% of end-use demand for the Water Quality Sensor Market, given regulatory mandates for continuous compliance monitoring

- Industrial process water applications are projected to grow at a CAGR of 8.4%, propelled by semiconductor fabrication and pharmaceutical ultrapure water requirements

• By Region

- North America accounted for USD 1.63 billion in 2025, with the U.S. contributing over 82% of regional revenue

- Asia-Pacific is poised to add the highest incremental value through 2035, supported by government-backed IoT water quality monitoring programs across China, India, and Southeast Asia

Water Quality Sensor Market Size and Forecast (2021–2035)

MRFR's sizing methodology triangulates bottom-up revenue estimates from sensor OEMs, utility capex disclosures, and top-down macro indicators including treated water volume growth and regulatory compliance timelines. Historical figures (2021–2024) reflect actual shipment and revenue data; 2025 is a calibrated base-year estimate; 2026–2035 values apply a 7.8% CAGR with minor annual variations reflecting policy milestones.