Water Taxi Market Summary

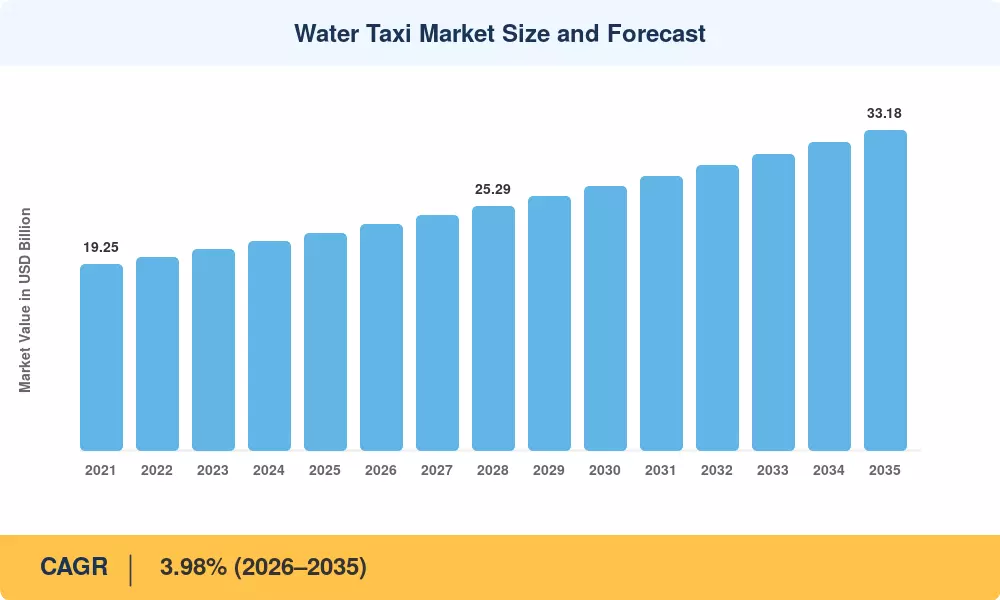

The Water Taxi Market reached an estimated USD 22.51 billion in 2025 and is projected to grow from USD 23.41 billion in 2026 to USD 33.18 billion by 2035, registering a CAGR of 3.98% during the forecast period (2026–2035). Municipal transit authorities across three continents are channeling capital into waterborne commuter service networks as congested urban corridors push policymakers toward multimodal solutions. The U.S. Federal Transit Administration's 2024 allocation of USD 412 million for ferry water taxi commuter service infrastructure, paired with the EU's Sustainable and Smart Mobility Strategy targeting a 90% emissions cut by 2050, anchors much of the near-term investment pipeline [2][3].

A technology pivot is well underway. Legacy diesel fleets that once dominated harbor and coastal routes are giving way to electric water taxi urban ferry platforms and solar-powered water taxi green propulsion systems capable of slashing direct fuel costs by roughly a fifth. Norway's Norled launched a fully battery-electric ferry water taxi commuter service on the Stavanger route in 2023, validating lithium-ion propulsion for vessels under 30 meters and prompting at least fourteen operators in Western Europe to file electrification permits within twelve months [4]. Autonomous water taxi harbor navigation trials, backed by USD 78 million in venture funding during 2024 alone, signal a second wave of disruption that will reshape crew economics across the forecast window [5].

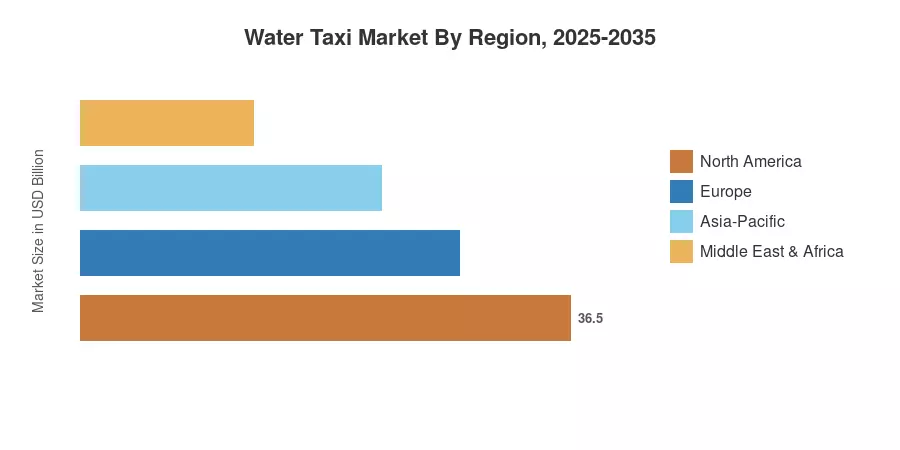

North America commands approximately 42% of the Water Taxi Market, driven by dense coastal metro corridors from New York to Vancouver. Asia-Pacific stands as the fastest-growing region with a projected CAGR of 4.09%, fueled by water taxi tourism charter expansion in Southeast Asian archipelago economies and rapid urbanization in coastal Indian cities. Europe holds the second-largest share at roughly 27%, underpinned by Scandinavian electrification mandates and Mediterranean tourism demand. By 2035, the Water Taxi Market is poised to become a mainstream urban transit layer rather than a niche tourism offering

Key Report Takeaways

• By Product Type

- Ferries captured roughly 50% of the Water Taxi Market in 2024, reflecting entrenched commuter networks across North American and Northern European corridors

- Yachts are forecast to expand at the fastest pace through 2035, driven by luxury water taxi tourism charter demand in the Caribbean and Maldives

- Sail boats maintain a niche presence, with a 2024 valuation near USD 1.58 billion as eco-tourism operators favor wind-assisted rigid inflatable boat RIB taxi alternatives

• By Propulsion Type

- Diesel propulsion accounted for a CAGR of 3.21% in the Water Taxi Market during the historical period, though fleet replacement cycles favor cleaner alternatives

- Electric water taxi urban ferry systems are projected to grow at the highest rate through 2035, backed by municipal emission-reduction targets

• By Region

- North America generated approximately USD 9.45 billion in Water Taxi Market revenue in 2024

- Asia-Pacific is expected to register a 4.09% CAGR, the fastest among all regions, during 2026–2035

Water Taxi Market Size and Forecast (2021–2035)

MRFR’s size methodology triangulates top-down government transit expenditure data, operator level income disclosures and vessel production figures from classification organizations such as Lloyd’s Register and DNV. Historical data (2021-2024) comes from audited financial statements and port authority traffic data. Forecast data (2026-2035) is developed using a calibrated compound growth model, cross-validated with IMO fleet predictions[6].

.

.webp?v=1784802863)