Web Analytics Market Summary

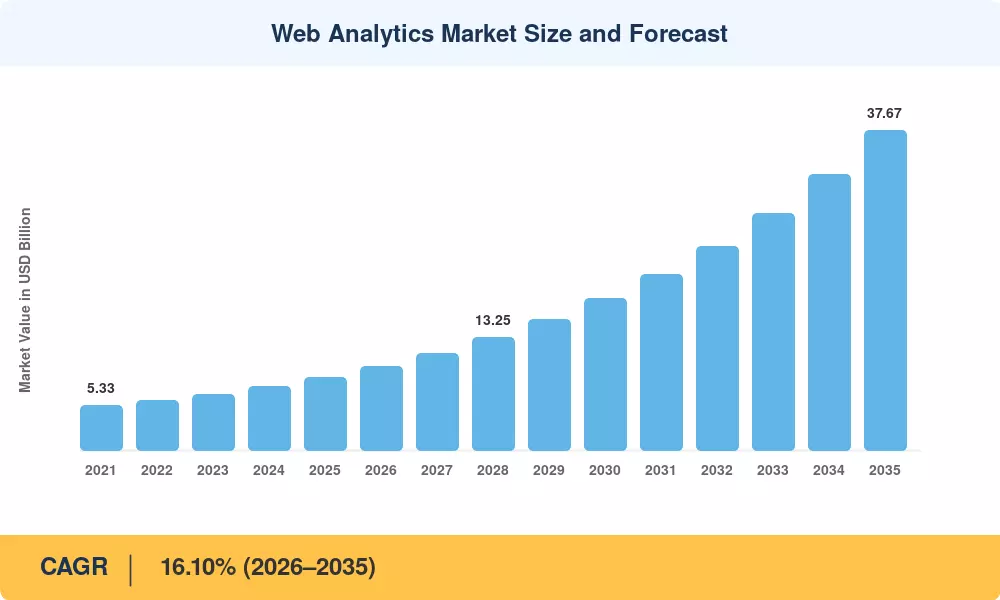

The Web Analytics Market reached a valuation of USD 8.54 billion in 2025 and is projected to grow from USD 9.83 billion in 2026 to USD 37.67 billion by 2035, registering a CAGR of 16.10% across the forecast period. Two forces underpin this trajectory: the global acceleration of digital commerce — which crossed USD 6.3 trillion in 2024 [1] — and a regulatory environment that now penalizes organizations operating without compliant measurement infrastructure. The EU's Digital Markets Act and successive U.S. state privacy laws have turned analytics from a discretionary marketing tool into a compliance necessity, pushing procurement budgets upward across every industry vertical.

A fundamental technology shift is reshaping the Web Analytics Market as legacy tag-based, client-side measurement gives way to server-side data collection, AI-driven journey intelligence, and privacy-preserving attribution models. Organizations invested an estimated USD 19 billion in marketing technology consolidation during 2024 alone [2], with analytics platforms sitting at the center of these stack overhauls. First-party data strategies, prompted by the decline of third-party cookies, have elevated analytics vendors that combine secure cloud infrastructure with real-time predictive capabilities.

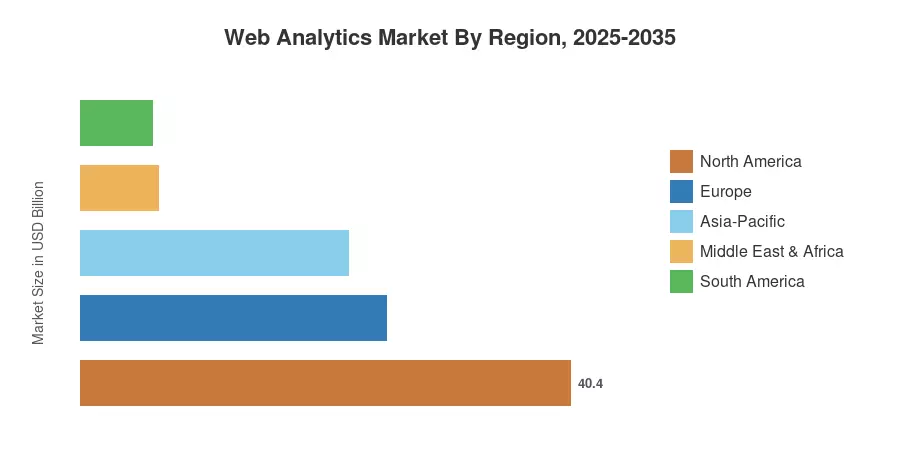

North America commands approximately 40.4% of the Web Analytics Market, anchored by enterprise-scale adoption among Fortune 500 retailers and financial services firms. Asia-Pacific stands as the fastest-growing region, projected to expand at a 16.80% CAGR through 2035, driven by digital payment proliferation in India and Southeast Asia. Europe holds the second-largest share at roughly 25.2%, shaped by GDPR-driven demand for privacy-centric analytics architectures. As digital touchpoints multiply across sectors from healthcare to government services, the Web Analytics Market is poised for sustained double-digit expansion through the next decade.

Key Report Takeaways

• By Application

- Online Marketing and Marketing Automation accounted for 43.5% of Web Analytics Market revenue in 2025, reflecting the deep integration of analytics into campaign orchestration workflows.

- Customer Journey Mapping is projected to register a CAGR of 17.07% through 2035, as enterprises shift from page-level metrics to full-funnel attribution models.

• By Offering

- Solutions held a 68.3% share of the Web Analytics Market in 2025, while Services are expected to grow at a 17.17% CAGR as implementation and managed analytics engagements expand.

• By Deployment

- Cloud-Based deployment controlled 72.2% of the Web Analytics Market share in 2025.

• By Region

- North America led the Web Analytics Market with a 40.4% share in 2025, driven by mature enterprise SaaS ecosystems.

- Asia-Pacific is forecast to register the highest CAGR of 16.80% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates combine primary interviews with analytics vendors, system integrators, and enterprise buyers alongside secondary analysis of financial filings, industry association data, and regulatory impact assessments. Historical figures (2021–2024) are triangulated against publicly reported vendor revenues; forecast figures (2026–2035) apply proprietary growth modeling calibrated to macroeconomic indicators, privacy regulation timelines, and technology adoption curves.