Xylene Market Summary

The global Xylene Market was valued at approximately USD 48,210 Million in 2025 and is projected to reach USD 75,840 Million by 2035, expanding at a CAGR of 4.64% over the forecast period 2026–2035. Two catalysts anchor this trajectory: the accelerating global buildout of polyethylene terephthalate (PET) packaging capacity and tightening brand-owner commitments to lower-carbon packaging that drive long-term offtake volumes for paraxylene production. China's 14th Five-Year Plan, which allocated over USD 30 billion toward integrated crude-to-chemicals complexes, has meaningfully widened upstream capacity and reinforced the cost base supporting aromatics yields.

The technological transformation reshaping the Xylene Market centres on the transition from stand-alone naphtha reformers to highly integrated refinery-to-chemicals configurations. Legacy catalytic reforming units in Japan and South Korea now operate below 60% utilisation as Gulf-based and Chinese integrated complexes achieve aromatics yields approaching 40% of feed. Saudi Aramco's Crude-to-Chemicals programme, a USD 100 billion-plus investment platform, and SABIC's integration strategy exemplify the shift that is displacing older European cracker economics. Bio-based xylene routes—while still niche—secured meaningful long-term offtake commitments from major beverage and apparel brands during 2023–2024, signalling that hydrocarbon processing chemicals face structural competition at the margins. [1][4]

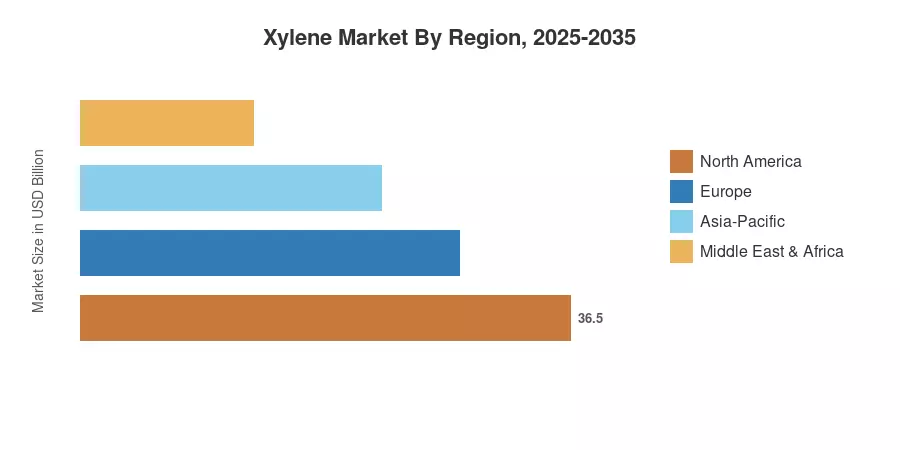

Asia-Pacific commanded roughly 53% of the Xylene Market in 2025 and is expected to maintain the fastest regional CAGR at approximately 4.90% through 2035, driven by China's downstream polymer complex expansions and India's rising demand for industrial solvent chemicals. North America ranked second with around 19% share, underpinned by U.S. Gulf Coast paraxylene capacity expansions and resilient domestic polyester demand. Europe, constrained by VOC regulations and energy costs, contributes an estimated 14% share but remains an innovation hub for bio-based and circular chemical intermediates. The next decade will test how quickly emerging bio-routes can scale against the structural cost advantage of integrated Middle Eastern and Chinese refiners. [2][5]

Key Report Takeaways

• By Type

- Para-xylene holds approximately 91% of the Xylene Market in 2025, reflecting its dominant role in paraxylene production for PET resin and polyester fibre

- Ortho-xylene is forecast to grow at a 4.52% CAGR through 2035, driven by rising phthalic anhydride demand in alkyd resins and paint solvent materials

- Meta-xylene, while the smallest isomer segment, is gaining traction in isophthalic acid production for specialty polyesters

• By Source

- The Xylene Market shows petroleum-based streams accounting for roughly 96% share in 2025

- Bio-based alternatives are projected to expand at a CAGR above 6.1% through 2035

• By Grade

- High-purity grade is the fastest-growing grade segment in the Xylene Market, advancing at approximately 5.1% CAGR as semiconductor and pharmaceutical solvent specifications tighten

• By Region

- Asia-Pacific leads with approximately 53% share of the Xylene Market and posts the highest regional CAGR at 4.90%

- North America and Europe combined represent about 33% of the Xylene Market volume, with diverging outlooks shaped by energy transition policies

Market Size and Forecast (2021–2035)

MRFR's estimates are built on a bottom-up volume model that cross-references reported production data from refinery operators, IEA aromatics supply statistics, and demand-side pull from PET resin, polyester, and industrial solvent channels. Historical values for 2021–2024 are anchored to actual trade and production records; 2025 is the base year; 2026–2035 figures apply the calibrated CAGR forward.