Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

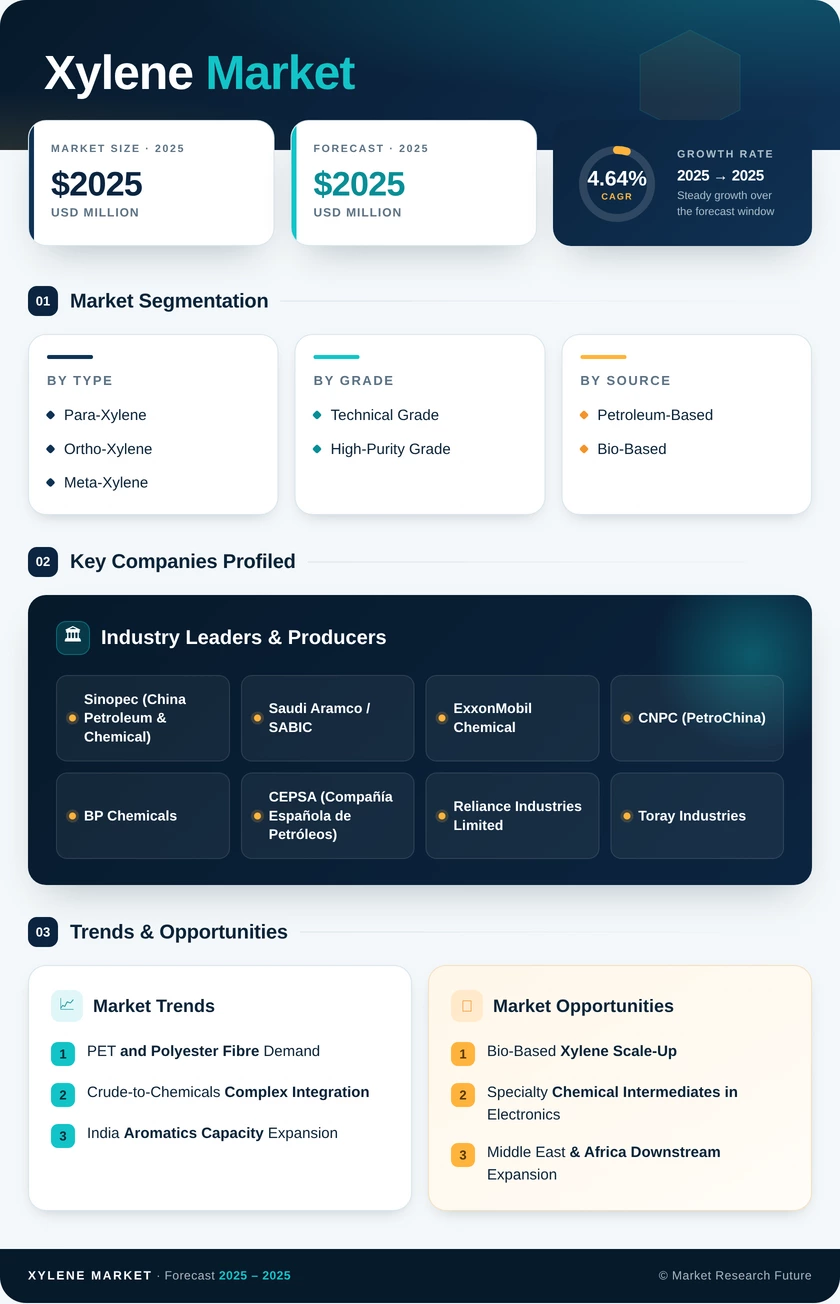

| By Type | Para-Xylene; Ortho-Xylene; Meta-Xylene | Para-Xylene (91.0% share) | Ortho-Xylene (4.52% CAGR) |

| By Grade | Technical Grade; High-Purity Grade | Technical Grade | High-Purity Grade (5.10% CAGR) |

| By Source | Petroleum-Based; Bio-Based | Petroleum-Based (96.0% share) | Bio-Based (~6.10% CAGR) |

| By Application | Solvents; Monomers; Other Applications | Solvents | Monomers (4.80% CAGR) |

| By End-User Industry | Plastics & Polymers; Paints & Coatings; Printing Inks & Adhesives; Xylene Markets & Others | Plastics & Polymers (71.5% share) | Plastics & Polymers (4.66% CAGR) |

| By Region | Asia-Pacific; North America; Europe; South America; Middle East & Africa | Asia-Pacific (53.0% share) | Asia-Pacific (4.90% CAGR) |

Market Segmentation Overview

By Type

| Sub-Segment | Key Trend |

| Para-Xylene | Captive consumption in PET resin and polyester fibre; integrated PX-PTA complexes dominating new capacity |

| Ortho-Xylene | Growth in alkyd resin demand for paint solvent materials; phthalate-free plasticiser substitution driving formulation shifts |

| Meta-Xylene | Niche but growing isophthalic acid demand for specialty packaging and glass fibre composites |

Para-xylene's dominance of the Xylene Market by type is structural rather than cyclical, anchored by the global PET packaging megatrend. Ortho-xylene occupies a resilient niche in coatings intermediates, while meta-xylene benefits from specialty polymer growth in engineered materials applications.

By Grade

| Sub-Segment | Key Trend |

| Technical Grade | Feedstock for paraxylene production units; industrial solvent chemicals bulk applications |

| High-Purity Grade | Rising demand from electronics and pharmaceutical sectors; premium pricing supports margin expansion |

Technical-grade volumes dominate the Xylene Market by sheer scale, but high-purity grade is where margin and growth opportunities intersect. Producers investing in purification infrastructure can access specification-driven markets largely insulated from commodity price cycles.

By Source

| Sub-Segment | Key Trend |

| Petroleum-Based | Catalytic reformate and coal-tar-based streams; integrated refinery chemicals are still cost-advantaged |

| Bio-Based | Scaling via long-term offtake agreements; ISCC PLUS certification enabling brand ESG claims |

The transition from petroleum to bio-based aromatic hydrocarbon solvents will be gradual. Bio-based xylene cannot displace petroleum feedstocks on economics alone within the forecast window, but regulatory carbon pricing and consumer brand commitments create commercially viable niches for certified bio-content supply.

By Application

| Sub-Segment | Key Trend |

| Solvents | Mature in developed markets; strong growth in ASEAN and South Asia paints a solvent materials demand |

| Monomers | PET-driven paraxylene production dominates; fastest-growing sub-category by value |

| Other Applications | Stable pharmaceutical and fuel-blending volumes; low growth outlook |

Solvent applications remain commercially significant and diverse, spanning paint solvent materials, industrial cleaning solvents, and specialty printing inks. The monomer sub-category, however, commands the investment attention of the global Xylene Market given its scale and tie to the high-growth PET packaging industry.

By End-User Industry

| Sub-Segment | Key Trend |

| Plastics & Polymers | Dominant demand pool; PET, polyester fibre, PBT engineering plastics, driving volumes |

| Paints & Coatings | VOC pressure in developed markets is offset by strong emerging market coatings growth |

| Printing Inks & Adhesives | Stable; gradual reformulation to lower-aromatic alternatives in the EU |

| Xylene Markets & Others | Niche; high-purity specifications create margin opportunity |

The plastics and polymers end-user segment defines the trajectory of the global Xylene Market more than any other demand driver. Its growth rate, geographic concentration in Asia-Pacific, and direct linkage to consumer packaging trends make it the primary lens through which investors, producers, and buyers should analyse market dynamics through 2035.