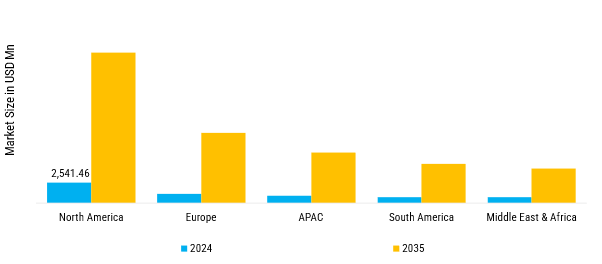

What is the current valuation of the dermal fillers market in 2025?

It is valued at approximately 6.35 USD Billion in 2024.

What is the projected market size for dermal fillers by 2035?

The market is expected to reach around 10.5 USD Billion by 2035.

What is the expected CAGR for the dermal fillers market during the forecast period 2025 - 2035?

It is projected to grow at a CAGR of 4.68% from 2025 to 2035.

Which application segments are driving growth in the dermal fillers market?

Facial contouring and wrinkle reduction are key application segments, with valuations of 2.5 USD Billion and 3.0 USD Billion, respectively, in 2025.

What types of dermal fillers are most popular in the market?

Hyaluronic acid fillers dominate the market, with a projected valuation of 5.5 USD Billion by 2035.

How do demographic factors influence the dermal fillers market?

Demographic factors such as age group and gender are expected to contribute approximately 2.5 USD Billion and 2.0 USD Billion, respectively, to the market by 2035.

What are the primary distribution channels for dermal fillers?

Direct sales and distributors are significant channels, with expected valuations of 4.0 USD Billion and 2.5 USD Billion, respectively, by 2035.

Which companies are leading the dermal fillers market?

Key players include Allergan, Revance Therapeutics, and Galderma, which are pivotal in shaping market dynamics.

What role do end users play in the dermal fillers market?

Cosmetic surgery centers and dermatology clinics are crucial end users, with projected market contributions of 3.0 USD Billion and 2.5 USD Billion, respectively, by 2035.

How does the market for lip enhancement compare to other applications?

Lip enhancement is valued at 1.5 USD Billion in 2025, indicating a growing interest but still trailing behind facial contouring and wrinkle reduction.

作者

Author

Satyendra Maurya

Research Analyst

An accomplished research analyst with high proficiency in market forecasting, data visualization, competitive benchmarking, and others. He holds a pronounced track record in research and consulting projects for sectors such as life sciences, medical devices, and healthcare IT. His capabilities in qualitative and quantitative analysis have resulted in positive client outcomes. Working on niche market trends, opportunities, sales, and forecasted value is part of his skill set.

read more

Co-Author

Rahul Gotadki

Research Manager

He holds an experience of about 9+ years in Market Research and Business Consulting, working under the spectrum of Life Sciences and Healthcare domains. Rahul conceptualizes and implements a scalable business strategy and provides strategic leadership to the clients. His expertise lies in market estimation, competitive intelligence, pipeline analysis, customer assessment, etc.

The secondary research process involved comprehensive analysis of regulatory databases, clinical trial registries, peer-reviewed aesthetic medicine journals, and authoritative health statistical repositories. Key sources included the US Food & Drug Administration (FDA) Centre for Devices and Radiological Health (CDRH) aesthetic device approvals database, European Medicines Agency (EMA) biomedical product registry, Health Canada Medical Devices Active Licence Listing (MDALL), Japan Pharmaceuticals and Medical Devices Agency (PMDA) cosmetic procedure regulations, China National Medical Products Administration (NMPA) aesthetic device classifications, UK Medicines and Healthcare products Regulatory Agency (MHRA), and Therapeutic Goods Administration (TGA) Australia.

Professional medical associations contributing data included the International Society of Aesthetic Plastic Surgery (ISAPS.org) Global Survey, American Society of Plastic Surgeons (ASPS) National Plastic Surgery Statistics, American Society for Dermatologic Surgery (ASDS) Procedure Census, American Academy of Facial Plastic and Reconstructive Surgery (AAFPRS) Annual Survey, British Association of Aesthetic Plastic Surgeons (BAAPS) UK Aesthetic Plastic Surgery Statistics, and German Society for Aesthetic Surgery (DGÄPC).

Academic and epidemiological sources comprised PubMed/MEDLINE indexed journals (Aesthetic Surgery Journal, Dermatologic Surgery, Journal of Cosmetic Dermatology), National Institutes of Health (NIH) RePORTER database, National Center for Biotechnology Information (NCBI) clinical genomic studies, World Health Organization (WHO) Global Health Expenditure Database, OECD.Stat Health Statistics, EU Eurostat Healthcare Database, CDC National Center for Health Statistics ambulatory procedure data, and national health ministry reports from South Korea (KFDA), Brazil (ANVISA), and India (CDSCO). These sources facilitated collection of biodegradable versus non-biodegradable product safety profiles, hyaluronic acid and calcium hydroxylapatite regulatory pathway comparisons, facial line correction procedure volumes, specialty clinic versus hospital utilization patterns, and regional reimbursement dynamics.

Primary Research

In the primary research process, stakeholders from the supply and demand sides were interviewed to acquire qualitative and quantitative insights that were specific to the polyalkylimide segments, PMMA microspheres, and biodegradable additives. From dermatology-focused pharmaceutical manufacturers, medical aesthetic device OEMs, and hyaluronic acid raw material suppliers, supply-side sources included Chief Executive Officers, Vice Presidents of Research & Development, Heads of Regulatory Affairs, and Commercial Directors. Demand-side sources included procurement managers from hospital plastic surgery departments, clinic administrators from specialty dermatology chains, board-certified plastic surgeons, dermatologists, cosmetic aesthetic specialists, and medical spa and medical directors. Primary research has confirmed pipeline timelines for next-generation cross-linked HA formulations, validated product segment differentiation between single-session and multi-session protocols and gathered insights on adoption patterns for facial line correction versus lip enhancement applications, pricing strategies for biodegradable compared to permanent fillers, and reimbursement pathways across hospital versus clinic settings.

Primary Respondent Breakdown:

By Designation: C-level Primaries (40%), Director Level (30%), Others (30%)

By Region: North America (32%), Europe (30%), Asia-Pacific (28%), Rest of World (10%)

Market Size Estimation

Global market valuation was derived through revenue mapping and procedure volume analysis across biodegradable and non-biodegradable categories. The methodology included:

Identification of 50+ key manufacturers across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa specializing in hyaluronic acid, calcium hydroxylapatite, poly-L-lactic acid, PMMA microspheres, and polyalkylimide formulations

Product mapping across facial line correction, lip enhancement, nasolabial fold reduction, facial scar revision, and facelift augmentation segments

Analysis of reported and modeled annual revenues specific to dermal filler portfolios, distinguishing biodegradable product lines (Juvederm, Restylane, Radiesse, Sculptra) from permanent fillers (Bellafill, Aquamid)

Coverage of manufacturers representing 75-80% of global market share in 2024

Extrapolation using bottom-up (procedure volume × Average Selling Price by country, segmented by clinic type and product category) and top-down (manufacturer revenue validation across ISAPS-reported procedure statistics) approaches to derive segment-specific valuations for biodegradable versus non-biodegradable markets

“This is really good guys. Excellent work on a tight deadline. I will continue to use you going forward and recommend you to others. Nice job”

Noah MalgeriCo-Founder

“Thanks. It’s been a pleasure working with you, please use me as reference with any other Intel employees.”

Joseph AguayoSales Operations & Pricing Manager

“Thanks for sending the report it gives us a good global view of the Betaïne market.”

Peter Groot koerkampAccount and Business Manager

“Thank you, this will be very helpful for OQS.”

La Terria DoddProgram Support Specialist

“We found the report very insightful! we found your research firm very helpful. I'm sending this email to secure our future business.”

Younghwan ChoiSenior Retail Manager

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile").

In general the report is well structured. Thanks very much for your efforts.”

Mark IrwinManagement Consultant

“I have been reading the first document or the study, ,the Global HVAC and FP market report 2021 till 2026. Must say, good info! I have not gone in depth at all parts, but got a good indication of the data inside!”

Rob KooikerGroup Product Manager HVAC & Fire Protection GMA

“We got the report in time, we really thank you for your support in this process. I also thank to all of your team as they did a great job.”

Akif MorogluStrategy & Business Development Director

“The Automotive 48V ECU Components Procurement Intelligence Study” was a complex project, but the Market Research Future (MRFR) team handled it with quality, agility, and customer-centricity. They delivered all requested data on time and within the agreed scope. The team, including Shubhendra Anand and Rahul Gotadki, was always readily available to clarify questions and swiftly implement necessary adjustments, driving the project to a successful conclusion within a very demanding timeframe.

I would also like to specifically commend Akshay Agarwal for his responsiveness and support at every stage—from our initial inquiry on May 6th through to final delivery on June 18th. His dedication made the entire process seamless.”

Guilherme Gomes MartinsProduct Management Director