Action Camera Market Summary

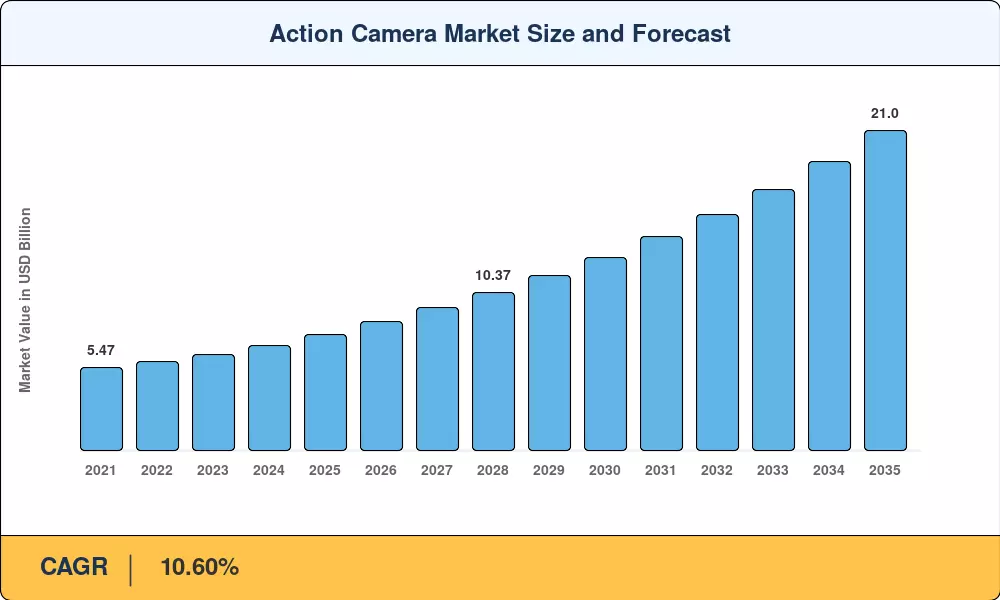

アクションカメラ市場は2025年に75億8,000万米ドルに達し、2026年に84億8,000万米ドルで始まり、年平均成長率10.60%で2035年までに210億米ドルに達する予測軌道の準備が整いました。この拡大を加速しているのは 2 つの力です。プロシューマー グレードの 8K および 360 度キャプチャ テクノロジーの主流価格帯への移行と、屋外レクリエーション インフラストラクチャに新たな資金を注ぎ込んでいる、アジア太平洋および北欧全域にわたる政府支援のアドベンチャー ツーリズム キャンペーンです。[1][2].

アクションカメラ市場では決定的なテクノロジーシフトが進行中です。従来の 1080p 専用デバイスは、Ultra-HD キャプチャ、オンデバイス AI シーン検出、ソーシャル プラットフォームへのワイヤレス ライブ ストリーミングが可能なコンパクトなモジュールに置き換えられています。 GoPro だけでも、2023 年から 2025 年の間に推定 1 億 8,500 万米ドルを研究開発に投資しましたが、DJI のシステムオンチップ コンポーネントの垂直統合により、製品サイクルのタイムラインが 9 か月未満に短縮されました。[3][4]。企業の導入により、対応可能な裾野が広がっています。法執行機関や消防活動における装着型カメラは、消費者セグメントを超えて安定した収益バッファーとなっています。

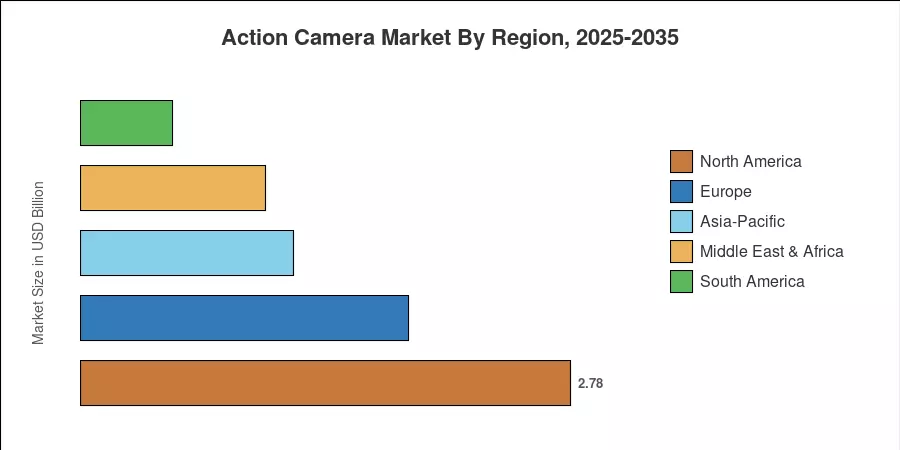

北米は、強力な消費者直販ブランド チャネルと成熟したエクストリーム スポーツ文化に支えられ、2025 年のアクション カメラ市場で 36.70% のシェアを獲得しました。アジア太平洋地域は、中国とインドの可処分所得の増加と拡大によって推進され、2035 年まで 16.00% の CAGR で最も急成長している地域です。国内観光政策。欧州は北欧のアウトドアレクリエーション支出とUEFA主導の放送需要に支えられ、24.50%で2番目に大きなシェアを占めている。次の 10 年は、堅牢なハードウェアとサブスクリプション主導のソフトウェア エコシステムを組み合わせることができるメーカーに報いるでしょう。

レポートの重要なポイント

• 解像度別

- Ultra-HD 4K 以降は、高解像度コンテンツ作成に対する消費者の好みを反映して、2025 年のアクション カメラ市場の推定 49.50% を獲得しました。

- フル HD 1080p デバイスは引き続き価格重視のセグメントにサービスを提供し、新興国でのエントリーレベルの需要が拡大する中、2035 年まで 9.20% の CAGR を維持します。

• 流通チャネル別

- オフライン小売業は、家電チェーン店での体験型の店内デモンストレーションによって、2025 年にアクション カメラ市場全体で 55.20% の収益シェアを獲得し、首位を獲得しました。

- メーカーが消費者直販のフルフィルメントに投資するため、ブランドのウェブストアは 2035 年まで 14.20% の CAGR で最速の成長を遂げると予測されています。

• アプリケーション別

- 2025 年にはスポーツとアドベンチャーの撮影が 64.80% のシェアを占め、アクション カメラ市場のレクリエーション分野の伝統を強化しました。

- 緊急および公共安全サービスは、身体に装着するカメラの義務化により、2035 年まで 15.60% の CAGR で増加しています。

• エンドユーザーによる

- 2025 年のアクション カメラ市場では、消費者が 67.30% のシェアを占めました。

- プロフェッショナルおよびエンタープライズ部門は、2035 年まで 15.20% の CAGR で拡大しています。

• 地域別

- 北米は、2025 年のアクション カメラ市場で 36.70% のシェアを獲得しました。

- アジア太平洋地域は、2035 年まで 16.00% の CAGR で最も急速に上昇している地域です。

アクションカメラ市場規模と予測(2021~2035年)

Market Research Future の推計は、120 名以上の業界関係者との一次インタビュー、企業の提出書類、輸出入貿易データベース、および 38 か国の POS データに対して検証された独自の需要モデルに基づいています。