感情分析市場の概要

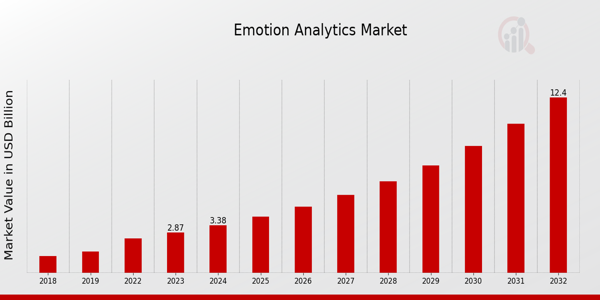

MRFRの分析によると、感情分析市場の規模は2022年に24.4億米ドルと推定されています。感情分析市場業界は、2023年の28.7億米ドルから2032年には124億米ドルに成長すると予想されています。感情分析市場のCAGR(年平均成長率)は、予測期間(2024~2032年)中に約17.64%になると予想されています。

強調される感情分析市場の主要トレンド

感情分析市場は、さまざまな業界で消費者の感情や行動を理解したいという需要の高まりによって推進されています。企業は、顧客体験を向上させ、製品やサービスを改善する上での感情的洞察の重要性をますます認識しています。人工知能と機械学習の進歩により、感情データの分析と解釈が容易になり、企業は戦略をより効果的に調整できるようになりました。さらに、データに基づく意思決定のニーズの高まりにより、組織は感情分析を導入するようになり、エンゲージメントの向上と顧客維持率の向上につながっています。特にヘルスケアと教育の分野では、市場参入の機会が数多く存在します。ヘルスケア分野では、医療従事者が患者の感情状態を理解し、適切な治療方法を調整できるようになるため、感情分析は患者ケアの向上に大きく貢献するでしょう。教育分野も、感情認識デバイスを用いることで、学生の注意力や学習への感情的な準備度合いを測り、学習成果を向上させることができるため、大きな役割を果たせる可能性があります。あらゆる分野で感情知能(EQ)の利点が認識されるようになり、企業は事業範囲を拡大し、市場の様々なターゲット層のニーズに応える発明を生み出す機会を得ています。

最近の傾向では、感情分析を仮想現実(VR)や拡張現実(AR)などの他のテクノロジーと統合する方向へのシフトが見られます。これらの統合により、感情反応に合わせて変化する没入型体験を生み出すことで、顧客とのインタラクションを強化できます。さらに、リモートワークやデジタルコミュニケーションツールの普及により、仮想環境における感情理解の必要性が浮き彫りになり、感情検出ソフトウェアの革新が進んでいます。組織がこれらのテクノロジーを採用し続けるにつれて、感情分析を取り巻く環境は進化を続け、さまざまなセクターに新たな可能性とアプリケーションが生まれます。

図 1: 感情分析市場規模、2024~2032 年 (10 億米ドル)

出典: 一次調査、二次調査、MRFR データベース、アナリストレビュー

感情分析市場の推進要因

顧客体験管理の重要性の高まり

感情分析市場業界は、さまざまなセクターにおける顧客体験管理の重要性の高まりによって大きく推進されています。企業や組織は、エンゲージメント、サービス品質、そしてブランドロイヤルティを向上させるために、顧客の感情を理解することの価値をこれまで以上に認識しています。消費者の期待が進化するにつれ、企業はソーシャルメディア、フィードバックフォーム、あるいは直接のコミュニケーションなど、あらゆるやり取りから感情を測定できる高度な分析ツールの導入を迫られています。こうした顧客インサイトの向上への需要から、組織はサービス、製品、そしてコミュニケーション戦略をより適切にカスタマイズするために、感情分析を業務に統合するようになっています。感情分析によって、企業は感情的な反応を捉え、分析することで、顧客満足度やブランドイメージに関する貴重な洞察を得ることができます。これは、差別化が不可欠な競争の激しい市場において極めて重要です。企業は顧客とのやり取りに高い基準を設定し続けているため、現在の顧客感情を理解するだけでなく将来の行動を予測するのにも役立つ戦略的資産として感情分析に注目しています。組織がこれらの洞察を業務改善や顧客維持戦略に活用するにつれて、この傾向は加速し、感情分析市場の大幅な成長につながると予想されます。

AI と機械学習技術の進歩

人工知能 (AI) と機械学習技術の進歩は、感情分析市場業界の成長を促進する上で重要な役割を果たしています。これらの技術革新により、組織は膨大な量の非構造化データを効率的に分析することが容易になりました。企業は、オーディオ、ビデオ、テキストデータを処理できるため、以前は得られなかった感情的な洞察を抽出できます。 AI と機械学習アルゴリズムにより、感情の検出と分析がより高速になり、より正確で、より信頼できるものになります。これらのテクノロジーは進化を続け、感情分析ツールに不可欠なものとなり、企業のリアルタイム フィードバックと強化された意思決定を可能にしています。

予測分析の需要の高まり

意思決定プロセスにおける予測分析の需要も、感情分析市場業界の成長を促進しています。組織がデータ主導の戦略を目指すにつれて、履歴データに基づいて感情の傾向と顧客の行動を予測する能力は非常に重要になります。予測分析は、企業が顧客のニーズと嗜好に積極的に対応し、よりパーソナライズされたエクスペリエンスを生み出すのに役立ちます。この傾向は、感情的な反応を理解することが結果に大きな影響を与える可能性があるマーケティング、ヘルスケア、金融などの分野でますます認識されています。

感情分析市場セグメントの洞察

感情分析市場のアプリケーションの洞察

感情分析市場には、さまざまな分析手法を通じて人間の感情や行動を理解するために不可欠な幅広いアプリケーションが含まれます。 2023年には、市場全体の価値は28億7,000万米ドルに達し、2032年までに大幅に成長すると予測されています。アプリケーションセグメントは、組織がデータを活用して顧客体験を向上させ、意思決定を改善するための多様な方法を示しています。音声分析は、2023年に9億米ドルと評価され、企業が顧客とのやり取りにおける感情的な反応を測定するのに役立つ重要な分野であり、顧客サービスと全体的な満足度を向上させるための不可欠なツールとなっています。このサブカテゴリが進化するにつれて、2032年までに価値が39億2,000万米ドルに増加すると予想されており、感情検出における重要性が高まっていることを示しています。一方、顔表情認識は、2023年に10億米ドルの評価額を持ち、2032年までに44億米ドルに達すると予想されています。このアプリケーションは、視覚的な手がかりを通じて感情状態をリアルタイムで分析できるため、ますます重要になってきており、小売やエンターテイメントなどの分野には欠かせないものとなっています。テキスト分析は、2023年に7億5000万米ドルと評価され、様々なチャネルからのテキストデータを処理することで、感情のニュアンスをより深く理解することができます。2032年までに33億米ドルにまで成長すると予想されており、ソーシャルメディアの感情分析や顧客フィードバック評価において重要な役割を果たすことが期待されています。心理グラフィック分析は、2023年には2億2000万米ドルと評価されていますが、その重要性の高まりを反映しており、2032年までに7億8000万米ドルに成長すると予測されています。このアプリケーションは、消費者の動機、態度、嗜好に関するより深い洞察を提供し、ターゲットを絞ったマーケティング戦略の可能性を秘めています。感情分析市場のセグメンテーションは、これらのアプリケーションが企業における感情的知性に対する高まる需要にどのように対応しているかを明らかにし、情報に基づいた意思決定を通じて顧客エンゲージメントとブランドロイヤルティを強化する機会を浮き彫りにしています。市場が拡大し続けるにつれて、これらのアプリケーションへの重点は、このダイナミックな業界における成長の潜在的な道を最大限に広げながら課題に対処する技術と方法論の進歩につながる可能性があります。

出典:一次調査、二次調査、MRFRデータベース、アナリストレビュー

感情分析市場の展開タイプの洞察

感情分析市場は勢いを増しており、2023年には28億7000万米ドルの予測価値があり、2024年には大幅な成長が見込まれています。今後数年間の市場成長を見据え、この市場区分は、オンプレミスやクラウドベースのソリューションといったアプローチを含む導入タイプの重要性を浮き彫りにしています。オンプレミス導入は、組織がデータとシステムをより強力に制御できるようにし、厳格なセキュリティ要件を持つ業界に対応します。一方、クラウドベースの導入は、柔軟性、費用対効果、アクセスの容易さからますます人気が高まっており、企業は事業を効率的に拡張できます。この市場では、両方の導入タイプの長所を組み合わせて多様な組織のニーズを満たすハイブリッドソリューションへの強いトレンドが見られます。テクノロジーの進化に伴い、様々な業界で感情分析ツールの需要が高まり、感情分析市場の収益がさらに増加すると予想されます。市場の成長は、ビジネス戦略における感情知性の重要度の高まりによって推進されており、企業が顧客の感情をより深く理解し、全体的なエンゲージメントを強化しようとする中で、業界に大きな機会が生まれています。

感情分析市場の最終用途に関する洞察

感情分析市場は、いくつかの重要な最終用途に区分されており、それぞれが市場の成長に独自に貢献しています。 2023年時点で、市場全体の価値は28億7000万米ドルと推定されており、様々な分野における安定した需要を反映しています。小売業界では、感情分析によって感情を分析することで顧客体験が向上し、顧客ロイヤルティと売上向上につながっています。ヘルスケア業界では、患者とのインタラクションやメンタルヘルス評価の改善といった感情分析の恩恵を受けており、治療現場において不可欠なツールとなっています。同様に、自動車業界では、ドライバーと乗客の安全確保のために感情分析を活用し、一人ひとりに合わせた体験を提供しています。メディアエンターテインメント業界では、感情分析を活用してコンテンツ配信とエンゲージメントを向上させ、視聴者とのより深いつながりを実現しています。教育業界もまた、感情分析によって学生のエンゲージメントや学習成果に関する洞察が得られ、より優れた教育戦略が促進されるなど、変化の兆しを見せています。こうした多様なセグメンテーションは、感情分析が様々な分野に幅広く適用可能であり、その重要性が高まっていることを浮き彫りにしており、感情分析市場の成長ポテンシャルを反映しています。

感情分析市場におけるテクノロジーインサイト

感情分析市場は、2023年に28億7000万米ドルと評価され、大幅な成長が見込まれています。この市場を牽引する主な要因として、医療、小売、エンターテインメントなど、様々な分野における感情データを分析するための高度な技術に対する需要の高まりが挙げられます。テクノロジー分野では、機械学習やディープラーニングといった手法が、大量の感情データを効率的に処理し、予測能力とリアルタイム分析を強化する能力から、極めて重要な役割を果たしています。自然言語処理もまた重要であり、機械がテキストを通じて伝えられる人間の感情を理解し解釈することを可能にし、顧客とのやり取りや満足度を向上させます。市場の進化に伴い、これらの技術の統合が市場の成長をさらに加速させ、企業は感情的な洞察を活用して戦略的な意思決定を行い、顧客ロイヤルティを育むことができるようになります。消費者行動の変化や技術の進歩は引き続き機会をもたらす一方で、データプライバシーや倫理的配慮といった課題が市場の動向に影響を及ぼす可能性があります。全体的なセグメントは、業界の多様なニーズに応える継続的なイノベーションと進化する方法論を特徴としており、感情分析市場の軌道を形作っています。

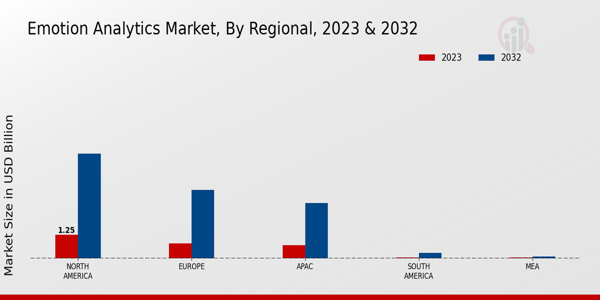

感情分析市場の地域別洞察

感情分析市場の地域セグメントは堅調な成長軌道を反映しており、北米が2023年に12億5,000万米ドルの評価額を達成してリードし、2032年には55億米ドルに成長すると予測されており、市場での過半数の地位を示しています。ヨーロッパは0.8億米ドルの評価額で続き、36億米ドルに達すると予測されており、市場動向の形成における重要な役割を浮き彫りにしています。 2023年に7億米ドルと評価され、29億米ドルに達すると予測されているアジア太平洋地域は、急速な技術進歩と感情主導型ソリューションの需要増加に牽引され、大きな可能性を示しています。南米と中東アフリカは、2023年にそれぞれ7億米ドルと5億米ドルと評価されている小規模市場ですが、成長の機会があり、2032年までに3億米ドルと1億米ドルに達すると予測されています。この地域区分は、感情分析市場の収益ダイナミクスに関する貴重な洞察を明らかにし、北米が優勢である一方で、変化する消費者行動と産業需要を反映して、APACなどの新興市場が将来の成長を促進する上でますます重要になっていることを示しています。

出典:一次調査、二次調査、MRFRデータベース、アナリストレビュー

感情分析市場の主要プレーヤーと競合分析

感情分析市場は、企業が顧客体験の向上とブランドロイヤルティの向上のために消費者の感情を理解することの価値を認識するにつれて、大きな注目を集めています。この分野では、顔認識、音声感情分析、心理生理学的測定など、さまざまな技術的手段を通じて感情を収集・分析します。この分野で事業を展開する企業は、多様なタッチポイントから得られる感情データを解釈できる高度な分析ソリューションを提供するために競争しています。顧客中心の戦略と改善されたエンゲージメントツールのニーズの高まりは、この市場におけるイノベーションを促進しています。競争が激化する中、企業は実用的な結果をもたらす最先端の技術と洞察を取り入れることで、自社のサービスを差別化しようと努めています。Emotientは、堅牢な表情認識技術で評価され、感情分析市場の主要プレーヤーとして台頭しています。同社の強みは、リアルタイムの感情検知能力にあり、これは、即時の感情的反応に基づいてサービスをカスタマイズしたい企業にとって非常に役立ちます。Emotientは、顔の表情から感情を高精度に分析できる強力なプラットフォームを構築することで、リーダーとしての地位を確立し、小売、ヘルスケア、エンターテインメントなど、さまざまな分野に適用可能です。また、分析機能を継続的に強化するディープラーニングアルゴリズムも活用し、感情認識技術の最前線に君臨し続けています。イノベーションと卓越性への強いこだわりが、Emotientの強力な市場プレゼンスにつながり、貴重なパートナーシップを築き、事業拡大を推進することに繋がっています。Beyond Verbalは、感情分析市場で事業を展開するもう一つの有力企業であり、人間の感情を解読するための音声分析を専門としています。同社は、音声のイントネーションとパターンを分析して感情状態を評価する独自の技術を開発し、従来のデータ指標では見落とされがちな洞察を提供しています。 Verbalの強みは、言葉のニュアンスから意味のある感情を抽出する能力にあります。これは、通信、カスタマーサービス、さらにはメンタルヘルスアプリケーションなどの分野で特に役立ちます。同社は、より深い感情的洞察を通じて、対人コミュニケーションの強化とユーザーエクスペリエンスの向上に注力しています。 Beyond Verbalは、アルゴリズムを継続的に改良し、製品ラインナップを拡充することで競争優位性を維持し、音声ベースの感情分析が企業と顧客のインタラクションを変革する可能性を示しています。

感情分析市場の主要企業

感情分析市場の業界動向

感情分析市場は、AIと機械学習技術の進歩に牽引され、近年、関心とイノベーションが急増しています。 AffectivaやEmotientといった企業は、顧客サービスからメンタルヘルスモニタリングに至るまで、様々なアプリケーションへの感情認識の統合に注力し、その能力を拡大しています。Beyond Verbalは音声感情分析のパイオニアとして、Nuance Communicationsは顧客とのインタラクションに関するより深い洞察を提供するためにプラットフォームを強化しています。MicrosoftとIBMは感情分析の機能を活用し、クラウドサービスの向上に努めており、重要なコラボレーションが進められています。

これらの企業の成長は明らかであり、評価額の上昇は、業界全体で感情分析ツールの需要が高まっていることを反映しています。公表されている合併や買収は確認されていますが、これらの企業における最近の具体的な活動は限られています。しかしながら、OracleやClarifaiといった企業からの投資増加は、この分野への関心の高まりを示しています。企業が感情知能(EQ)の重要性を認識するにつれ、市場は急速に拡大し、消費者行動をより繊細に理解し、プラットフォームをまたいでユーザーエクスペリエンスを向上させることに貢献すると見込まれています。

感情分析市場のセグメンテーションに関する洞察

感情分析市場は2024年に33.76億USDの価値がありました。

市場は2035年までに201.6億USDに達すると予測されています。

2025年から2035年までの感情分析市場の予想CAGRは17.64%です。

顔の表情認識とテキスト分析は、2035年までに48億USDに達すると予測されています。

主な展開タイプはオンプレミスで、2023年までに80.8億USDに達すると予想されており、クラウドベースは2035年までに120.8億USDに達すると予測されています。

ヘルスケアは2035年までに48億USDに成長すると予想されており、相当な需要を示しています。

機械学習は2035年までに80.64億USDの評価額で支配すると予測されています。

主要なプレーヤーには、IBM、Microsoft、Google、Amazon、NVIDIAなどが含まれます。

音声分析、顔の表情認識、心理的分析はすべて堅調な成長が見込まれており、評価額は数十億米ドルに達する見込みです。

自然言語処理は2035年までに39.76億USDに達すると予測されており、市場におけるその重要性を強調しています。

著者

Ankit Gupta is a seasoned market intelligence and strategic research professional with over six plus years of experience in the ICT and Semiconductor industries. With academic roots in Telecom, Marketing, and Electronics, he blends technical insight with business strategy. Ankit has led 200+ projects, including work for Fortune 500 clients like Microsoft and Rio Tinto, covering market sizing, tech forecasting, and go-to-market strategies. Known for bridging engineering and enterprise decision-making, his insights support growth, innovation, and investment planning across diverse technology markets.

read more