Emotion Analytics Market Summary

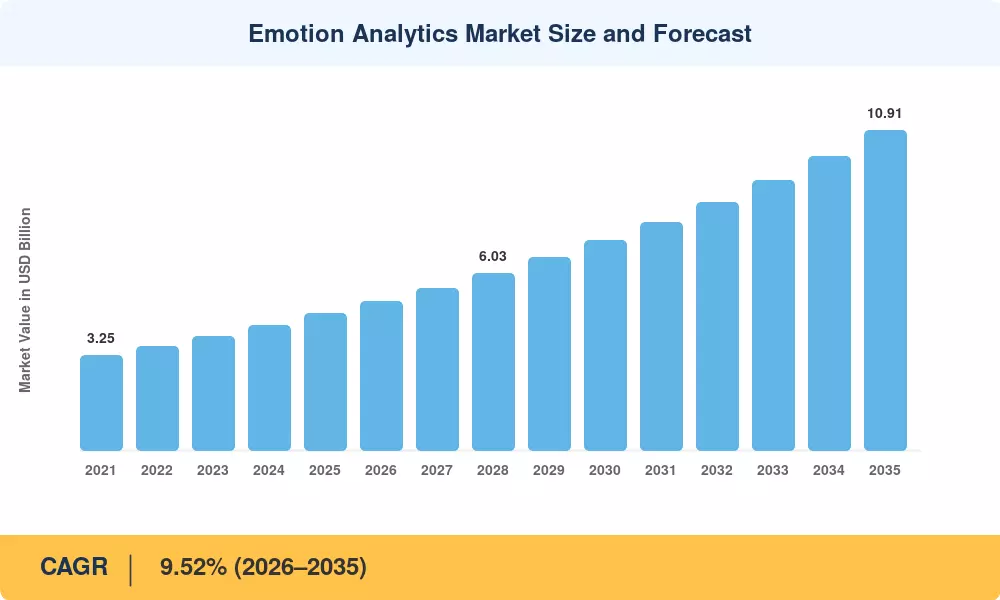

The Emotion Analytics Market reached an estimated USD 4.68 billion in 2025 and is projected to grow from USD 5.37 billion in 2026 to USD 10.91 billion by 2035, registering a CAGR of 9.52% during the forecast period. Two catalysts are reshaping enterprise spending: the EU AI Act's transparency mandates for biometric classification systems and a wave of contact-center modernization investments exceeding USD 18 billion globally, both of which place AI-powered sentiment detection platforms at the center of compliance and productivity agendas.

A fundamental technology shift is underway. Legacy keyword-based sentiment tagging — once the backbone of voice-of-customer programs — is giving way to multimodal inference engines that fuse facial expression recognition software outputs with voice prosody, biosignals, and contextual text analysis. This convergence has been accelerated by transformer-based architectures and on-device neural processing units, with Qualcomm and Apple collectively committing over USD 4 billion in edge-AI silicon R&D during 2024 alone[5]. Customer emotion analysis for retail is emerging as a high-value deployment vertical, with pilot programs at major U.S. and European retailers demonstrating 12–17% lifts in conversion rates when real-time emotion AI for call centers is paired with adaptive scripting [4].

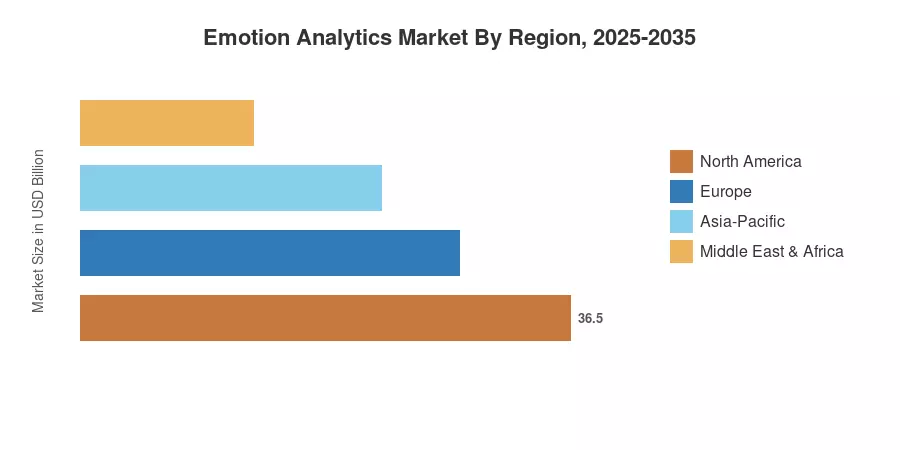

North America commands the largest share of the Emotion Analytics Market at approximately 39% of 2025 revenue, anchored by mature SaaS ecosystems and early regulatory frameworks for biometric data. Asia-Pacific stands as the fastest-growing region with a projected CAGR of 12.38%, driven by government-backed smart-city programs across China, India, and South Korea. Europe holds the second-largest position, where GDPR-aligned privacy-preserving architectures give regional vendors a competitive edge in voice tone emotion recognition systems procurement The next decade will test whether vendors can scale real-time emotion AI for call centers without triggering the consent fatigue that slowed earlier biometric rollouts.

Key Report Takeaways

• By Deployment

- Cloud-based emotion analytics solutions accounted for 58.2% of the Emotion Analytics Market in 2025, reflecting SaaS-first procurement across mid-market enterprises

- Edge and on-device inference is projected to achieve a 10.78% CAGR through 2035, fueled by latency-critical automotive and healthcare deployments

• By Component

- Software platforms held USD 2.16 billion in revenue during 2025 within the Emotion Analytics Market, as facial expression recognition software bundles expanded into omnichannel suites

- Hardware modules — including dedicated emotion-processing chipsets — will post the fastest component CAGR at 10.05% through 2035

• By Modality

- Facial emotion recognition commanded 41.5% of the Emotion Analytics Market revenue in 2025,

- Though biosignal-driven multimodal systems are gaining share at a 11.68% CAGR

• By Application

- Customer service and contact centers captured USD 2.75 billion in 2025, with real-time emotion AI for call centers reducing average handle time by up to 22%

- Healthcare and well-being use cases are forecast to expand at a 9.69% CAGR, driven by telepsychiatry reimbursement reforms

• By Region

- North America led with 39.1% share in 2025

- While Asia-Pacific is expected to log a 12.38% CAGR through 2035

MRFR's market sizing combines bottom-up revenue modeling from over 120 vendor disclosures with top-down validation against enterprise IT spending benchmarks published by Gartner, IDC, and regional trade bodies. Historical figures (2021–2024) are based on confirmed financial disclosures; 2025 is the base-year estimate; and 2026–2035 values apply the calibrated 9.52% CAGR with adjustments for anticipated adoption inflections in 2028 and 2032.