Author

Snehal Singh

香水市場調査報告書 製品タイプ別(香水、オードトワレ、オードコロン、ボディスプレー、フレグランスオイル)、用途別(パーソナルケア、家庭用、商業用、工業用)、香りのノート別(フローラル、フルーティ、ウッディ、オリエンタル、シトラス)、流通チャネル別(オンライン小売、スーパーマーケット、デパート、専門店)、地域別(北米、ヨーロッパ、南米、アジア太平洋、中東およびアフリカ)- 2035年までの予測。

MRFRの分析によると、2024年の世界香水市場規模は144.1億米ドルと推定されています。香水業界は、2025年に150.2億米ドルから2035年には227.8億米ドルに成長すると予測されており、2025年から2035年の予測期間中に年平均成長率(CAGR)は4.25を示しています。

グローバルフレグランスマーケットは、持続可能性とeコマースの成長に向けてダイナミックなシフトを経験しています。

| 2024 Market Size | 14.41 (USD十億) |

| 2035 Market Size | 2278億ドル |

| CAGR (2025 - 2035) | 4.25% |

ロレアル(フランス)、エスティ ローダー(アメリカ)、プロクター・アンド・ギャンブル(アメリカ)、コティ(アメリカ)、レブロン(アメリカ)、資生堂(日本)、シャネル(フランス)、ユニリーバ(イギリス)、エイボン(イギリス)

Our Impact

Enabled $4.3B Revenue Impact for Fortune 500 and Leading Multinationals

Partnering with 2000+ Global Organizations Each Year

30K+ Citations by Top-Tier Firms in the Industry

グローバルフレグランス市場は、消費者の嗜好の変化と持続可能性への強調によって、現在ダイナミックな進化を遂げています。個人が環境への影響をより意識するようになるにつれて、フレグランスの配合において自然およびオーガニック成分への明らかな傾向が見られます。このシフトは、クリーンな製品への欲求を反映するだけでなく、エコフレンドリーな実践を支持する広範な社会運動とも一致しています。さらに、Eコマースの台頭は、消費者がフレグランスにアクセスする方法を変革し、より多様性と利便性を提供しています。オンラインプラットフォームは、ブランドがより広いオーディエンスにリーチできるようにし、個々の嗜好に応じたよりパーソナライズされたショッピング体験を促進しています。

持続可能性への強調は、グローバルフレグランス市場内でますます顕著になっています。消費者は、自然およびオーガニック成分を使用した製品に惹かれ、環境責任への広範なコミットメントを反映しています。この傾向は、ブランドがエコフレンドリーな調達および製造方法を採用しようとする可能性を示唆しています。

Eコマースプラットフォームの拡大は、フレグランスの流通の風景を大きく変えています。消費者は、さまざまなブランドや香りを自宅の快適さから探索できるようになり、より多様な製品にアクセスできるようになっています。この傾向は、オンラインショッピングが消費者の行動や嗜好を形成する上で重要な役割を果たし続けることを示唆しています。

グローバルフレグランス市場内で、ニッチおよびアーティザナルフレグランスブランドへの関心が高まっています。これらの小規模企業は、独自の香りのプロファイルや職人技に焦点を当て、香りの選択において個性を求める消費者にアピールしています。この傾向は、主流の製品からよりパーソナライズされた独自の製品へのシフトを示唆しているかもしれません。

技術の進歩は、グローバル香料産業の進化において重要な役割を果たしています。香りの調合や供給システムの革新により、ブランドはより複雑で魅力的な香水を作成できるようになっています。例えば、人工知能や機械学習の進展が消費者の好みを分析し、トレンドを予測するために活用されており、これによりより成功した製品の発売につながる可能性があります。さらに、生産プロセスにおける持続可能な技術の使用がますます普及しており、エコフレンドリーな製品に対する消費者の需要に合致しています。技術が進化し続ける中で、香水開発の創造性と効率性が向上し、グローバル香料産業の市場動向に影響を与えることが予想されます。

環境問題に対する消費者の意識の高まりは、グローバル香水産業を持続可能な慣行へと導いているようです。ブランドは、環境に配慮した原材料の調達に焦点を当てており、これは環境意識の高い消費者にアピールするだけでなく、持続可能性を支持する規制のトレンドとも一致しています。天然香料の市場は大幅に成長することが予測されており、今後数年間で年平均成長率が10%を超えるとの見積もりがあります。この持続可能性へのシフトは、生産プロセスの革新をもたらし、廃棄物やカーボンフットプリントを削減する可能性があります。消費者が製品の調達において透明性を求める中、持続可能性を優先する企業はグローバル香水産業において競争優位を得る可能性が高いです。

セレブリティフレグランスの普及は、グローバルフレグランス業界に影響を与え続けています。著名人による endorsements やコラボレーションは、ブランドの可視性や消費者の関心を高めることが多いです。データによると、セレブリティフレグランスはかなりの売上を生み出すことができ、一部のラインは初年度に1億米ドルを超える収益を達成しています。この現象は、消費者がセレブリティの endorsements に関連する憧れのライフスタイルに惹かれていることを示唆しています。しかし、市場はセレブリティフレグランスの飽和により消費者の疲労感に直面する可能性もあります。それにもかかわらず、セレブリティブランドの魅力は、グローバルフレグランス業界における強力な推進力として残り、購買決定やブランドロイヤルティに影響を与えています。

急速に拡大する電子商取引プラットフォームは、グローバル香水業界の小売業の風景を再形成しています。オンライン販売チャネルはますます人気を集めており、香水セクターの電子商取引売上が2026年までに総売上の30%以上を占める可能性があることを示すデータがあります。この傾向は、オンラインショッピングの便利さと、より幅広い製品にアクセスできる能力によって推進されています。さらに、ソーシャルメディアマーケティングやインフルエンサーとのコラボレーションがブランドの可視性と消費者のエンゲージメントを高めています。その結果、従来の実店舗は、この進化する市場で競争力を維持するために戦略を適応させる必要があるかもしれません。電子商取引の台頭は、グローバル香水業界における消費者の購買行動に引き続き影響を与える可能性が高いです。

ニッチおよびアーティザナルな香水ブランドの出現は、グローバル香水産業に大きな影響を与えています。これらのブランドは、独自の香りのプロファイルと高品質の成分を強調することが多く、個別化された独占的な体験を求める消費者にアピールしています。市場データによると、ニッチ香水セグメントは年間約12%の成長率を示しており、消費者の好みがより独特な製品にシフトしていることを示しています。この傾向は、香水を通じた個性や自己表現への欲求に起因している可能性があります。消費者がこれらの専門的な製品にますます惹かれる中、既存のブランドはこの成長する市場セグメントを捉えるために革新し、ポートフォリオを多様化する必要があるかもしれません。ニッチブランドの台頭は、グローバル香水産業内の競争ダイナミクスを再定義する可能性が高いです。

グローバルフレグランス市場において、製品タイプの分布は、香水が最大のセグメントであり、かなりの市場シェアを占めていることを示しています。その魅力は、贅沢さと個人の表現に深く根ざしており、質に投資する意欲のある強力な消費者基盤を形成しています。それに対して、ボディスプレーは急成長しているセグメントとしてのニッチを確立しており、主に手頃な価格と便利さを求める若年層の消費者にアピールしています。このダイナミクスは、異なるデモグラフィックにおける多様な嗜好を示しています。消費者がより目の肥えた存在になるにつれて、フレグランス市場内の成長トレンドは、汎用性と日常使用製品への嗜好の変化によって影響を受けています。ボディスプレーは、その軽やかな香りと使いやすさから支持を集めており、カジュアルな場面に適しています。一方、香水セグメントは、個人のアイデンティティを高めることを目的としたフォーミュレーションやブランディング戦略の革新によって引き続き繁栄しています。

香水(支配的)対オーデコロン(新興)

香水は、濃縮されたフォーミュレーションと長持ちする香りを提供する能力で知られ、グローバルフレグランスマーケットの主要なプレーヤーと見なされています。このセグメントは、特に香りの選択において贅沢さと洗練さを重視する消費者にアピールします。それに対して、オードトワレは、日常使いのためにより軽やかでリフレッシングな香りを求める人々の間で人気が高まっています。香料オイルの濃度が低いことが特徴で、より控えめな香りを提供し、暖かい季節に好まれることが多いです。多様でカジュアルな香りへの親和性の高まりは、オードトワレをますます魅力的な選択肢として位置づけており、特にダイナミックなライフスタイルに合った選択肢を求めるミレニアル世代やZ世代の消費者の間で人気が高まっています。

グローバルフレグランス市場は、さまざまな最終用途セグメントにわたって多様な分布を示しており、パーソナルケア製品が最大のシェアを占めています。このセグメントには、化粧品、スキンケア、ヘアケア、その他のパーソナルグルーミングアイテムに使用される香水が含まれます。それに続いて、家庭用セグメントが重要なプレーヤーとして浮上しており、消費者が魅力的な香りで生活空間を向上させることをますます求める中で急成長を遂げています。香水の選択肢が広がる中、これらの2つのセグメントは市場におけるさまざまな消費者の好みを捉える位置にあります。

個人ケア:主流対家庭:新興

グローバルフレグランス市場において、パーソナルケアセグメントは依然として支配的であり、多様なデモグラフィックにわたる美容およびグルーミング製品に対する需要の高まりによって推進されています。このセグメントは、強力なマーケティング戦略と香りのフォーミュレーションにおける絶え間ない革新の恩恵を受けており、消費者に多様な選択肢を提供しています。一方、家庭用セグメントは、キャンドル、ディフューザー、エアフレッシュナーなどの家庭環境での香りの使用が増加しているため、新興市場として位置付けられています。アロマセラピーや家庭の雰囲気を向上させることの利点に対する認識の高まりが、このセグメントの成長を促進しています。そのため、ブランドは家庭環境に特化したユニークな香りの開発に投資しており、市場の競争が激化し急速に拡大している要素となっています。

グローバルフレグランス市場において、セグメントの分布はフローラルノートが最大の要素であり、世界中の消費者の心と感覚を魅了しています。バラからジャスミンまでの幅広い香りを含むフローラルフレグランスは、プレミアムおよびマスマーケットの両カテゴリーで強固な地位を確立し、さまざまなデモグラフィックにわたって売上を支配しています。それに対して、サンダルウッドやシダーのような豊かで土の香りを特徴とするウッディノートは急速に人気を集めており、より深く、より地に足のついた嗅覚体験を求める多様なオーディエンスにアピールしています。これらの香りの成長は、消費者の嗜好の変化や自然で土の香りへの新たなトレンドに影響されています。香りを通じた個人の表現への消費者の傾向が高まる中で、ウッディノートの復活が見られ、選択肢としてだけでなくライフスタイルの声明として位置づけられています。さらに、フローラルとウッディの両方のノートを含むユニセックスフレグランスの人気が、これらのセグメントにおける市場の拡大をさらに促進し、香りの販売の未来に対して有望な軌道を示しています。

フローラル(優勢)対ウッディ(新興)

フローラル香料セグメントは、その伝統的な魅力と多様性により、さまざまな年齢層や文化的背景に響くため、世界の香水市場で依然として支配的です。フローラルの香りは、女性らしさ、ロマンチックさ、エレガンスを象徴することが多く、消費者にとって常に人気があります。主要ブランドは、これらの特性を活用して、消費者とのつながりを強化する魅力的なマーケティングキャンペーンを展開しています。一方で、新興のウッディセグメントは、現代の感情に合わせて進化しており、強さ、安定感、洗練を象徴しています。持続可能性のトレンドが高まる中、ウッディの香りはますます自然由来の成分から調達され、エコ意識の高い消費者に合致しています。このシフトは、ウッディの香りの市場での地位を強化するだけでなく、その物語を深め、伝統と現代性の融合に寄与し、成長する市場にとって魅力的な選択肢となっています。

グローバルフレグランス市場において、オンライン小売チャネルは、利便性と多様性を求める消費者の好みにより、最大のシェアを占めています。オンラインプラットフォームは、さまざまな顧客の好みに応じた幅広いフレグランスオプションを提供しています。一方で、スーパーマーケットもこのセグメント内で重要なニッチを確立しており、食料品の買い物をしながら迅速かつアクセスしやすい選択肢を求める買い物客にアピールしています。彼らの市場シェアはかなりのものですが、現在、オンライン小売と比較して成長速度は遅くなっています。

スーパーマーケット(支配的)対専門店(新興)

スーパーマーケットは、広範なリーチと確立された小売ネットワークを活用して、消費者に人気の香水ブランドへの容易なアクセスを提供する支配的な流通チャネルとして浮上しています。彼らは幅広い人口統計に対応し、手頃な価格と便利さを提供することを目指しており、これが市場での存在感を大いに高めています。それに対して、専門店は新たなチャネルとして台頭しており、特定の顧客ニーズに応えるニッチな香水製品に焦点を当てています。これらの店舗は、パーソナライズされたサービスとユニークな製品提供を通じてショッピング体験を向上させ、顧客の忠誠心を育んでいます。消費者がユニークでパーソナライズされた香水体験にシフトする中、専門店は急速に支持を集めており、香水愛好者の需要に応えています。

香水市場に関する詳細な洞察を得る 無料サンプルを請求する

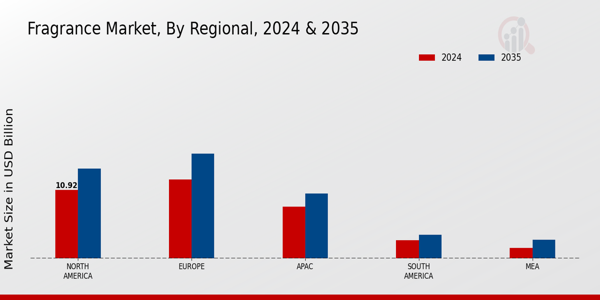

グローバルフレグランス市場は、多様な地域のダイナミクスによって特徴づけられ、全体的な成長において重要な役割を果たしています。2024年には、北米が109.2億米ドルの市場価値を占め、パーソナルケア製品への強い需要と文化的トレンドの影響によって推進されています。ヨーロッパは、香水業界における歴史的な重要性と革新的な製品の発売により、125.8億米ドルの評価を反映し、続いています。

2024年に82.6億米ドルと評価されるAPAC地域は、都市化の進展と可処分所得の増加により急速に台頭しており、市場における重要なプレーヤーとなっています。南米は29.5億米ドルの市場価値を持ち、進化する香り文化を強調しています。一方、MEA地域は16.8億米ドルと評価され、消費者の嗜好の変化と中間層の増加によって成長の可能性を示しています。各地域は、文化的および個人的な重要性のために香りを受け入れる多様な消費者によって、グローバルフレグランス市場の収益に独自に貢献しており、市場の成長は多面的で競争的です。

出典:一次調査、二次調査、Market Research Futureデータベースおよびアナリストレビュー

グローバルフレグランス市場は、確立されたブランドと新興プレーヤーの間で激しい競争が繰り広げられる、動的で広範なセクターです。この市場は、消費者の嗜好の変化、進化するトレンド、プレミアムおよびニッチなフレグランスへの傾向の高まりによって影響を受けています。可処分所得や都市化などの経済的要因も、市場のダイナミクスを形成する上で重要な役割を果たしています。企業は、フレグランスの処方における革新、広範なマーケティング戦略、有名デザイナーやセレブとのコラボレーションを通じて、厳しい競争に取り組んでいます。

この競争の激しい環境は、ブランドロイヤルティと消費者エンゲージメントの重要性を浮き彫りにし、企業は常に提供を向上させ、さまざまな地域市場で強力な存在感を確立するよう努めています。消費者がユニークな嗅覚体験を求める中、グローバルフレグランス市場は成長を続け、プレーヤーが自らを差別化するための魅力的な機会を提供しています。アボンは、さまざまな人口統計を対象としたフレグランス製品の広範なポートフォリオを活用し、グローバルフレグランス市場での強力な存在感が認識されています。このブランドは、ダイレクトセリングモデルとパーソナライズされた顧客とのインタラクションを通じて、忠実な顧客基盤を育成しています。

アボンの強みは、さまざまな嗜好や場面に応じた幅広いフレグランスを提供できる能力にあり、これにより広範なオーディエンスにアピールしています。企業は、品質を損なうことなく手頃な価格を強調し、多くの消費者にアクセス可能であることを確保しています。さらに、アボンの持続可能性へのコミットメントと原材料の責任ある調達は、香りの世界での評判をさらに高め、環境に配慮した顧客とのつながりを強化しています。

全体として、アボンは革新と顧客中心の実践に焦点を当てることで、グローバルフレグランス市場に戦略的に位置付けています。資生堂は、グローバルフレグランス市場の著名なプレーヤーであり、豊かな伝統と品質・洗練の評判を誇っています。同社の製品ポートフォリオには、伝統と現代的な感性を融合させたフラッグシップフレグランスが含まれており、グローバルなオーディエンスにアピールしています。資生堂の強みは、強力な研究開発能力にあり、進化する消費者の嗜好に共鳴する革新的な香りの導入を可能にしています。

同社は、さまざまな戦略的合併や買収を通じて重要な市場プレゼンスを確立し、リーチを拡大し、提供を強化しています。さらに、資生堂は高級ブランドとのコラボレーションを積極的に行い、独占的なフレグランスを創出することで、目の肥えた顧客を惹きつけています。高品質な原材料と豪華なパッケージに焦点を当てることで、資生堂は競争の激しいフレグランス市場で際立っています。同ブランドは、グローバルなマーケティング活動に投資を続けており、グローバルフレグランス市場の最前線に留まり、さまざまな地域の消費者との強い関係を育んでいます。

グローバルフレグランス市場は、2024年から2035年にかけて年平均成長率4.25%で成長すると予測されており、プレミアム製品と持続可能な調達に対する消費者の需要の高まりがその要因です。

新しい機会は以下にあります:

2035年までに、市場は進化する消費者の好みと革新的な戦略を反映して、堅調な成長を遂げると予想されています。

| 市場規模 2024 | 14.41億米ドル |

| 市場規模 2025 | 15.02億米ドル |

| 市場規模 2035 | 22.78億米ドル |

| 年平均成長率 (CAGR) | 4.25% (2024 - 2035) |

| レポートの範囲 | 収益予測、競争環境、成長要因、トレンド |

| 基準年 | 2024 |

| 市場予測期間 | 2025 - 2035 |

| 過去データ | 2019 - 2024 |

| 市場予測単位 | 億米ドル |

| 主要企業のプロファイル | 市場分析進行中 |

| カバーされるセグメント | 市場セグメンテーション分析進行中 |

| 主要市場機会 | グローバルフレグランスにおける持続可能で自然な成分の需要の高まりは、重要な機会を提供します。 |

| 主要市場ダイナミクス | 持続可能で自然な成分への消費者の嗜好の変化が、フレグランス業界の革新を促進しています。 |

| カバーされる国 | 北米、ヨーロッパ、APAC、南米、中東・アフリカ |

The secondary research process involved comprehensive analysis of regulatory databases, trade publications, industry association reports, and authoritative cosmetics and fragrance organizations. Key sources included the International Fragrance Association (IFRA), International Fragrance Foundation (IFF), Cosmetics Europe – The Personal Care Association, US Food & Drug Administration (FDA) Cosmetics Division, European Chemicals Agency (ECHA) REACH Database, National Institute of Standards and Technology (NIST), Cosmetics & Toiletries (C&T) Magazine, Perfumer & Flavorist Magazine, International Federation of Societies of Cosmetic Chemists (IFSCC), HCPA (Household & Commercial Products Association), Bureau of Indian Standards (BIS) for Cosmetic Safety, China’s National Medical Products Administration (NMPA), International Trade Chemistry Association (ITCA), NCBI/PubMed for dermatological safety studies, UN Comtrade Database for import/export statistics, Eurostat Trade Data, US International Trade Commission (USITC) fragrance trade reports, and national statistics offices for retail sales data from key markets. These sources were used to collect formulation standards, regulatory compliance data, raw material pricing trends, consumer preference studies, and competitive landscape analysis for premium fragrances, mass-market scents, fragrance oils, and associated personal care applications.

During the primary research process, both supply-side and demand-side stakeholders were interviewed to get qualitative and quantitative information. Supply-side sources included CEOs, Presidents of Global Fragrance Creation, Vice Presidents of Brand Development, Chief Perfumers, and heads of regulatory affairs from fine fragrance houses, flavor and fragrance manufacturers, and personal care product formulators. Demand-side sources included Chief Merchandising Officers from department stores and specialty beauty retailers, procurement directors from mass-market chains, dermatologists who specialize in allergic reactions to fragrance compounds, and marketing heads from luxury fashion houses that have perfume licenses. Primary research confirmed market segmentation across product tiers, confirmed new fragrance launch pipelines, and gathered information on consumer purchasing behavior, digital sampling strategies, raw material sourcing sustainability, and olfactory trend adoption patterns.

Primary Respondent Breakdown:

By Designation: C-level Primaries (42%), Director Level (25%), Others (33%)

By Region: North America (32%), Europe (30%), Asia-Pacific (35%), Rest of World (3%)

Global market valuation was derived through revenue mapping and consumption volume analysis across value chains. The methodology included:

Identification of 45+ key manufacturers across fine fragrance houses (Givaudan, Firmenich, IFF, Symrise), beauty conglomerates (L'Oréal, Estée Lauder, Coty, Puig), and personal care formulators spanning North America, Europe, Asia-Pacific, Latin America, and Middle East

Product mapping across perfume, eau de toilette, eau de cologne, body spray, and fragrance oil categories

Analysis of reported and modeled annual revenues specific to fragrance portfolios and licensed brand operations

Coverage of manufacturers and fragrance houses representing 72-78% of global market share in 2024

Extrapolation using bottom-up (consumer unit volume × ASP by country/region, adjusted for duty-free and grey market flows) and top-down (manufacturer revenue validation, ingredient supplier shipment data) approaches to derive segment-specific valuations for luxury, prestige, and mass-market tiers across distribution channels

Triangulation & Validation

Data triangulation was achieved by cross-referencing primary interview insights with secondary data from trade associations, validating shipment volumes against retail scan data, and reconciling manufacturer-reported revenues with import/export statistics. Market forecasts were stress-tested against historical GDP-per-capita correlations, beauty expenditure elasticity coefficients, and regional tourism recovery patterns affecting travel retail fragrance sales.

このレポートの無料サンプルを受け取るには、以下のフォームにご記入ください

“This is really good guys. Excellent work on a tight deadline. I will continue to use you going forward and recommend you to others. Nice job”

“Thanks. It’s been a pleasure working with you, please use me as reference with any other Intel employees.”

“Thanks for sending the report it gives us a good global view of the Betaïne market.”

“Thank you, this will be very helpful for OQS.”

“We found the report very insightful! we found your research firm very helpful. I'm sending this email to secure our future business.”

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

“I have been reading the first document or the study, ,the Global HVAC and FP market report 2021 till 2026. Must say, good info! I have not gone in depth at all parts, but got a good indication of the data inside!”

“We got the report in time, we really thank you for your support in this process. I also thank to all of your team as they did a great job.”

“The Automotive 48V ECU Components Procurement Intelligence Study” was a complex project, but the Market Research Future (MRFR) team handled it with quality, agility, and customer-centricity. They delivered all requested data on time and within the agreed scope. The team, including Shubhendra Anand and Rahul Gotadki, was always readily available to clarify questions and swiftly implement necessary adjustments, driving the project to a successful conclusion within a very demanding timeframe.

I would also like to specifically commend Akshay Agarwal for his responsiveness and support at every stage—from our initial inquiry on May 6th through to final delivery on June 18th. His dedication made the entire process seamless.”