発電機市場 概要

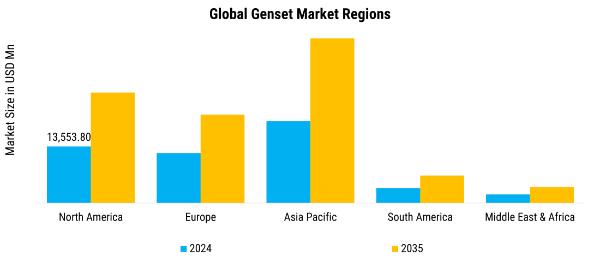

Market Research Futureの分析によると、世界の発電機市場は2024年に508億4,890万米ドルと評価されています。ソノブイ産業は2025年の538億2,180万米ドルから2035年までに976億5,100万米ドルに成長すると予測されており、予測期間中(2025年〜)6.84%の年間平均成長率(CAGR)を示しています。 2035年)。 世界の発電機市場は、幅広い用途にわたって信頼性の高い電力を供給するように設計された発電機セットの生産、流通、展開で構成されています。発電機は通常、内燃エンジンとオルタネーターを統合して機械エネルギーを電気に変換し、系統電力が利用できない、または不安定な状況でも動作の継続性を確保します。これらのシステムは電力目的で使用され、住宅、商業、産業および公益事業部門にわたって不可欠なものとなっています。

主要な市場動向とハイライト

世界の発電機市場の傾向として、発電機はもはや単なる「バックアップ」マシンではなく、重要な施設の回復力と継続性戦略に組み込まれています。

- データセンターの拡大と 5G/エッジネットワークの展開は、構造的に重要な傾向です。データセンターはダウンタイムがほぼゼロの電力を要求するため、発電機はバックアップ層の必須コンポーネントとなっており、多くの場合、リチウムイオン電池や UPS システムによって支えられています。

- 密集した都市環境、局所的な騒音、ゾーニング規則により、防音エンクロージャ、低騒音レベルの発電機、占有スペースから離れた場所に設置できるリモートマウント構成の採用が推進されています。

- ディーゼルは、エネルギー密度が高く、燃料の入手可能性が高く、過酷な条件下でも実証済みの信頼性があるため、引き続き主流となっています。

- おそらく最も戦略的なトレンドは、発電機をハイブリッド電力システムとマイクログリッドに統合することです。

市場規模と予測

| 2024年の市場規模 | 50,848.9 (USD Million) |

| 2035年の市場規模 | 97,651.0 (USD Million) |

| CAGR (2025 - 2035) | 6.84% |

| 2024 年に最大の地域市場シェアを獲得 | アジア太平洋地域 |

主要なプレーヤー

Caterpillar、Cummins、Generac、アトラスコプコ、MTU オンサイト エナジー、KOHLER、バルチラ、HIMOINSA、スターリング&ウィルソン、マヒンドラ・パワール、ヤンマー、アクサ・パワー・ジェネレーション。