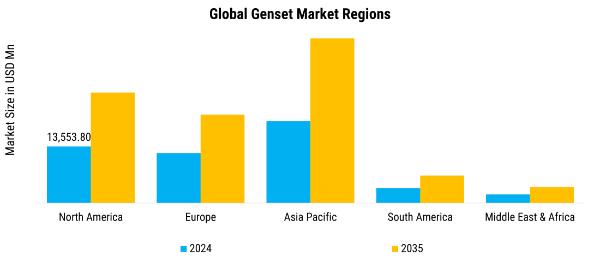

Genset Market Summary

As per Market Research Future analysis, Global Genset Market was valued at USD 50,848.9 million in 2024. The Sonobuoy Industry is projected to grow from USD 53,821.8 million in 2025 to USD 97,651.0 million by 2035, exhibiting a compound annual growth rate (CAGR) of 6.84% during the forecast period (2025 - 2035). The global genset market comprises the production, distribution, and deployment of generator sets designed to provide reliable electrical power across a wide range of applications. A genset typically integrates an internal combustion engine with an alternator to convert mechanical energy into electricity, ensuring continuity of operations in situations where grid power is unavailable or unstable. These systems are used for power purposes, making them essential across residential, commercial, and industrial and utility sectors

Key Market Trends & Highlights

The Global Genset Market is trend is that gensets are no longer just “backup” machines but are embedded into resilience and continuity strategies for critical facilities.

- The expansion of data centers and 5G/edge‑network rollouts is a structurally important trend. Data centers demand near‑zero‑downtime power, making gensets a mandatory component of their backup layers, often backed by lithium‑ion batteries or UPS system.

- Dense urban environments, local noise and zoning rules are pushing the adoption of sound‑attenuated enclosures, low‑sound‑level gensets, and remote‑mount configurations that allow placement away from occupied spaces.

- Diesel remains dominant because of its high energy density, fuel availability, and proven reliability in harsh conditions.

- Perhaps the most strategic trend is the integration of gensets into hybrid power systems and microgrids.

Market Size & Forecast

| 2024 Market Size | 50,848.9 (USD Million) |

| 2035 Market Size | 97,651.0 (USD Million) |

| CAGR (2025 - 2035) | 6.84% |

Major Players

Caterpillar, Cummins, Generac, Atlas Copco, MTU Onsite Energy, KOHLER, Wärtsilä, HIMOINSA, Sterling & Wilson, Mahindra Powerol, Yanmar, and Aksa Power Generation.