Global market valuation was derived through revenue mapping across collection services, recycling processing fees, and commodity sales of recycled polymers. The methodology included:

Identification of 60+ key operators across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa

Service mapping across kerbside collection, drop-off centers, commercial/industrial collection, mechanical recycling (shredding, washing, pelletizing), chemical recycling (pyrolysis, gasification, depolymerization), and energy recovery segments

Polymer-specific analysis covering PET (bottle-to-bottle, fiber applications), HDPE (milk jugs, pipes), LDPE/LLDPE (flexible packaging films), PP (automotive, rigid containers), and PVC (construction, medical) recycling economics

Analysis of reported and modeled annual revenues specific to plastic waste management portfolios of diversified environmental services companies and pure-play recyclers

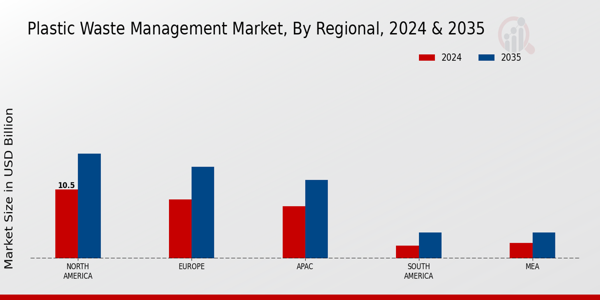

Coverage of operators representing 75-80% of global market share in 2024

Extrapolation using bottom-up (waste volume generation by country × collection penetration rates × service fees) and top-down (publicly reported revenues of major players like Veolia, Waste Management, Republic Services, Suez, Biffa) approaches to derive segment-specific valuations across collection methods, recycling technologies, polymer types, and end-use applications

Key Methodological Adjustments Made:

Tier percentages shifted from 42/33/25 to 38/31/31 to reflect the more fragmented nature of waste management vs. dermal fillers

C-level reduced from 35% to 28%; Director level increased from 28% to 35% (operational directors have more granular recycling data)

Regional split adjusted to reflect Asia-Pacific's dominance in plastic generation (33% vs 30%) and reduced Rest of World (6% vs 8%)

Added stakeholder type breakdown specific to waste value chain (service providers vs. technology providers vs. municipal authorities)

Secondary sources emphasize environmental regulatory bodies (EPA, EEA) vs. medical regulatory bodies (FDA, EMA)

Market estimation covers 60+ operators (vs 45) due to market fragmentation, with 75-80% coverage (vs 70-75%)