Predictive Maintenance Market Summary

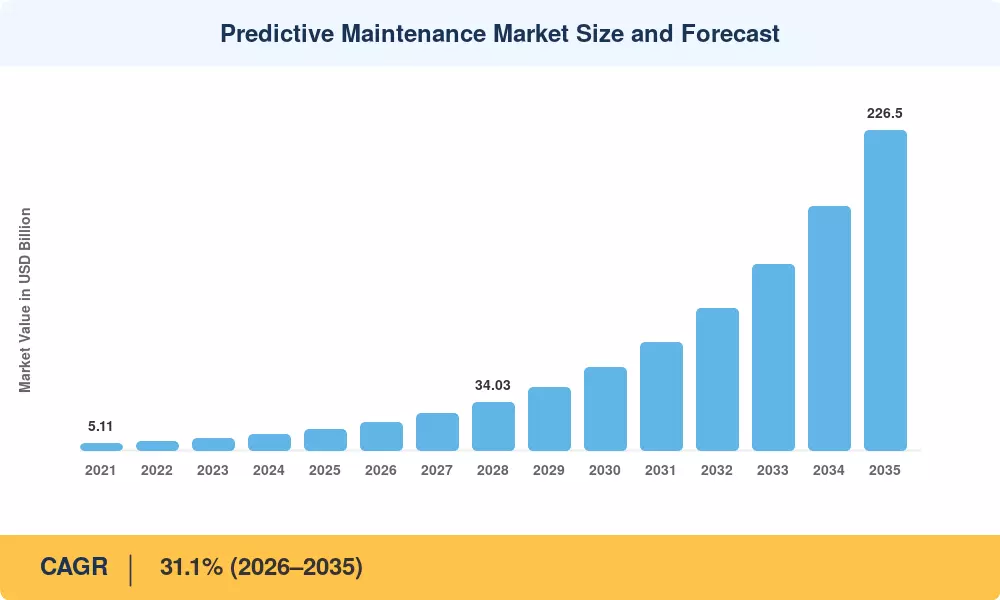

予知保全市場は、2025 年に評価額 151 億米ドルに達し、2026 年の 198 億米ドルから 2035 年までに 2,265 億米ドルに増加すると予測されており、予測期間 (2026 ~ 2035 年) 中に 31.1% の CAGR を記録します。この加速は、企業のデジタル変革の義務と、企業の急速な衰退によるところが大きいです。センサーコスト — 米国エネルギー省の先進製造局によると、産業用 IoT センサーの価格は 2020 年以来約 40% 下落しました。[2]。 EU 機械規則 (2023/1230) や米国の CHIPS および科学法の製造規定などの政府プログラムにより、資産重視の業界は状態監視システムを生産ラインに直接組み込むことを余儀なくされています。

抜本的なテクノロジーの変化により、施設が機器の健全性を管理する方法が書き換えられています。従来の時間ベースの事後保全体制は、かつては石油精製所、発電所、自動車工場で標準的でしたが、振動、熱、音響データをリアルタイムで処理する AI 駆動の機械故障予測プラットフォームに取って代わられています。最近のレポートでは、高度な資産健全性管理プログラムにより、計画外のダウンタイムが 30 ~ 50% 削減され、機械の寿命が 20 ~ 40% 延長されると推定されています。[3]。現在、クラウドネイティブのメンテナンス予測ソフトウェアがデフォルトの導入モデルとして機能していますが、オフショアリグや遠隔鉱山などの帯域幅に制約のある環境ではエッジハイブリッドアーキテクチャが台頭しています。

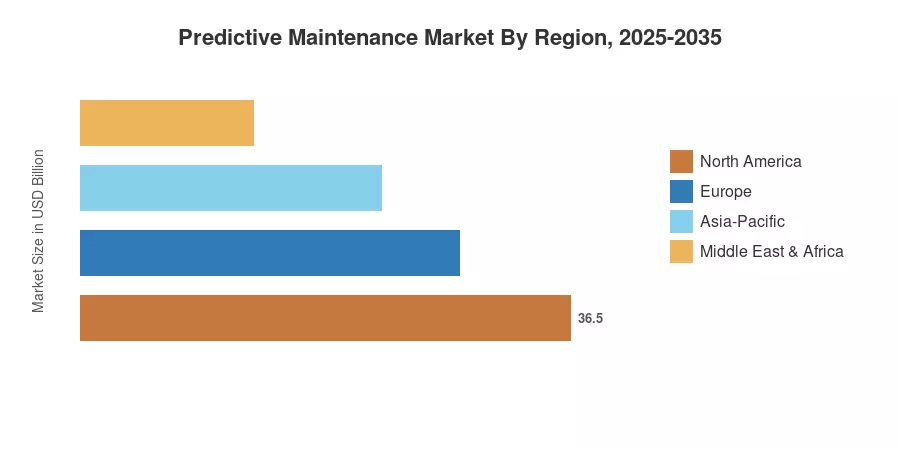

地域的な観点から見ると、航空宇宙、石油・ガス、ディスクリート製造での多用により、北米が予知保全市場で最大のシェアを占め、2025 年の収益の 31.2% を占めています。アジア太平洋地域は、中国のスマートファクトリー推進とインドの生産連動型インセンティブ(PLI)制度によって後押しされ、CAGR 32.7% が予測され、最も急成長している地域として浮上しています。[4]。ヨーロッパは、ドイツのインダストリー 4.0 エコシステムと EU のグリーン ディール産業指令に支えられ、シェア 26.5% で 2 番目に大きな地位を占めています。今後 10 年は、相互運用可能で AI ファーストのプロアクティブな機器サービス ソリューションを大規模に提供するベンダーが報われるでしょう。

レポートの重要なポイント

• コンポーネント別

- ハードウェアは、振動センサーとエッジ ゲートウェイに対する強い需要を反映して、2025 年の予知保全市場シェアの 48.5% を占めました。

- 企業が AI を活用した状態監視システムや分析ダッシュボードに投資するため、ソフトウェアは 2035 年まで 38.4% の CAGR で拡大すると予想されています。

- コンサルティング、統合、管理された運用を含むサービスは、2035 年までに 428 億米ドルに達すると予測されています。

• 導入モード別

- クラウド プラットフォームは 2025 年の予知保全市場規模の 61.5% を占め、エンタープライズ レベルでの資産健全性管理における拡張性の利点を反映しています。

• 企業規模別

- クラウド プラットフォームは 2025 年の予知保全市場規模の 61.5% を占め、エンタープライズ レベルでの資産健全性管理における拡張性の利点を反映しています。

- 大企業は 2025 年に 68.2% の収益シェアを獲得しました。中小企業は、手頃な価格の SaaS ベースのメンテナンス予測ソフトウェアが参入障壁を下げるため、33.2% という最高の予測 CAGR を記録しています。

• 地域別

- 北米は、2025 年に世界収益の 31.2% を占め、予知保全市場をリードしました。

- アジア太平洋地域は、中国、インド、韓国における産業のデジタル化が牽引し、32.7%のCAGRで発展すると予測されています。

市場規模と予測 (2021 ~ 2035 年)

MRFR の推計は、ボトムアップの収益モデリング (ベンダー開示、プロジェクト データベース) と、マクロ経済指標および産業資本支出調査に対するトップダウンの相互検証を組み合わせています。