Predictive Maintenance Market Summary

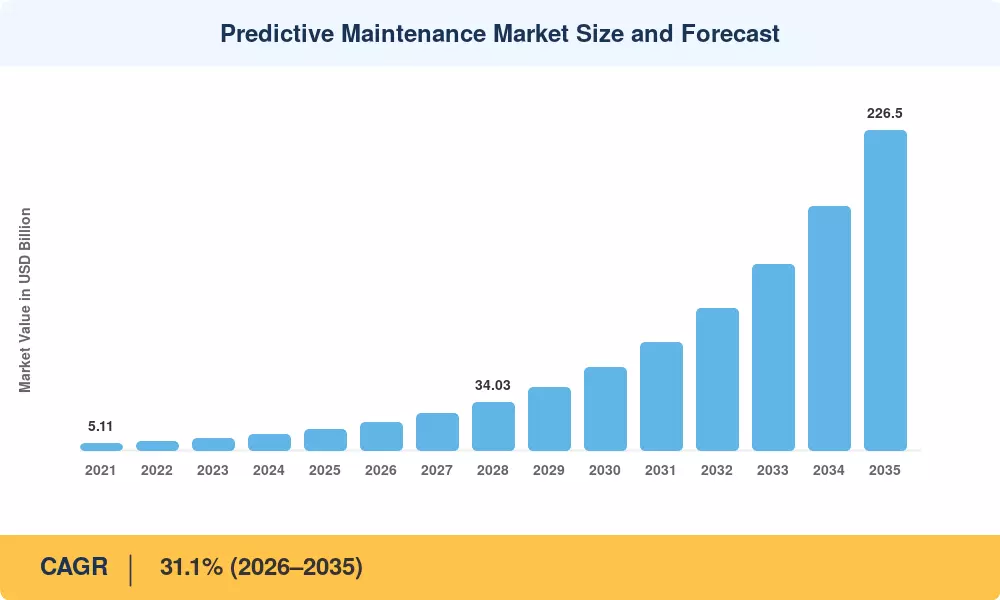

The Predictive Maintenance Market reached a valuation of USD 15.10 Billion in 2025 and is projected to climb from USD 19.80 Billion in 2026 to USD 226.50 Billion by 2035, registering a CAGR of 31.1% during the forecast window (2026–2035). This acceleration owes much to enterprise digital-transformation mandates and the rapid erosion of sensor costs — industrial IoT sensor prices have dropped roughly 40% since 2020, according to the U.S. Department of Energy's Advanced Manufacturing Office [2]. Government programs such as the EU Machinery Regulation (2023/1230) and the U.S. CHIPS and Science Act's manufacturing provisions are compelling asset-heavy industries to embed condition monitoring systems directly into production lines.

A sweeping technology shift is rewriting how facilities manage equipment health. Legacy time-based and reactive maintenance regimes — once the norm across oil refineries, power plants, and automotive factories — are giving way to AI-driven machine failure prediction platforms that process vibration, thermal, and acoustic data in real time. A recent report estimates that advanced asset health management programs can cut unplanned downtime by 30–50% and extend machinery life by 20–40% [3]. Cloud-native maintenance forecasting software now serves as the default deployment model, though edge-hybrid architectures are rising in bandwidth-constrained environments such as offshore rigs and remote mines.

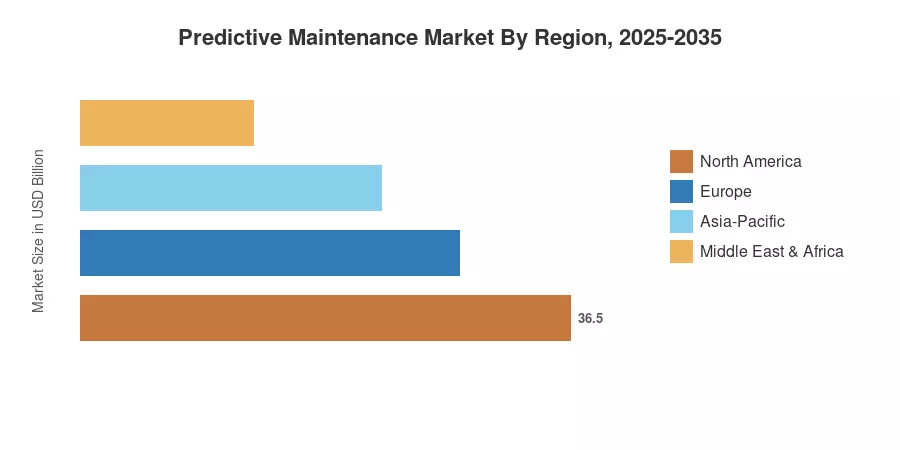

From a regional standpoint, North America commands the largest share of the Predictive Maintenance Market at 31.2% of 2025 revenue, driven by heavy adoption in aerospace, oil and gas, and discrete manufacturing. Asia-Pacific emerges as the fastest-growing region with a projected CAGR of 32.7%, fueled by China's smart-factory push and India's Production Linked Incentive (PLI) schemes [4]. Europe holds the second-largest position at 26.5% share, anchored by Germany's Industrie 4.0 ecosystem and the EU's Green Deal industrial mandates. The decade ahead will reward vendors who deliver interoperable, AI-first, proactive equipment servicing solutions at scale.

Key Report Takeaways

• By Component

- Hardware accounted for 48.5% of the Predictive Maintenance Market share in 2025, reflecting strong demand for vibration sensors and edge gateways.

- Software is set to expand at a 38.4% CAGR through 2035, as enterprises invest in AI-powered condition monitoring systems and analytics dashboards.

- Services — including consulting, integration, and managed operations — are projected to reach USD 42.80 billion by 2035.

• By Deployment Mode

- Cloud platforms represented 61.5% of the Predictive Maintenance Market size in 2025, reflecting scalability advantages for asset health management at the enterprise level.

• By Enterprise Size

- Cloud platforms represented 61.5% of the Predictive Maintenance Market size in 2025, reflecting scalability advantages for asset health management at enterprise level.

- Large enterprises held 68.2% revenue share in 2025; SMEs register the highest forecast CAGR at 33.2% as affordable SaaS-based maintenance forecasting software lowers entry barriers.

• By Region

- North America led the Predictive Maintenance Market with 31.2% of global revenue in 2025.

- Asia-Pacific is projected to progress at a 32.7% CAGR, driven by industrial digitization in China, India, and South Korea.

Market Size and Forecast (2021–2035)

MRFR's estimates blend bottom-up revenue modeling (vendor disclosures, project databases) with top-down cross-validation against macroeconomic indicators and industrial capital-expenditure surveys.