3D Metrology Market Summary

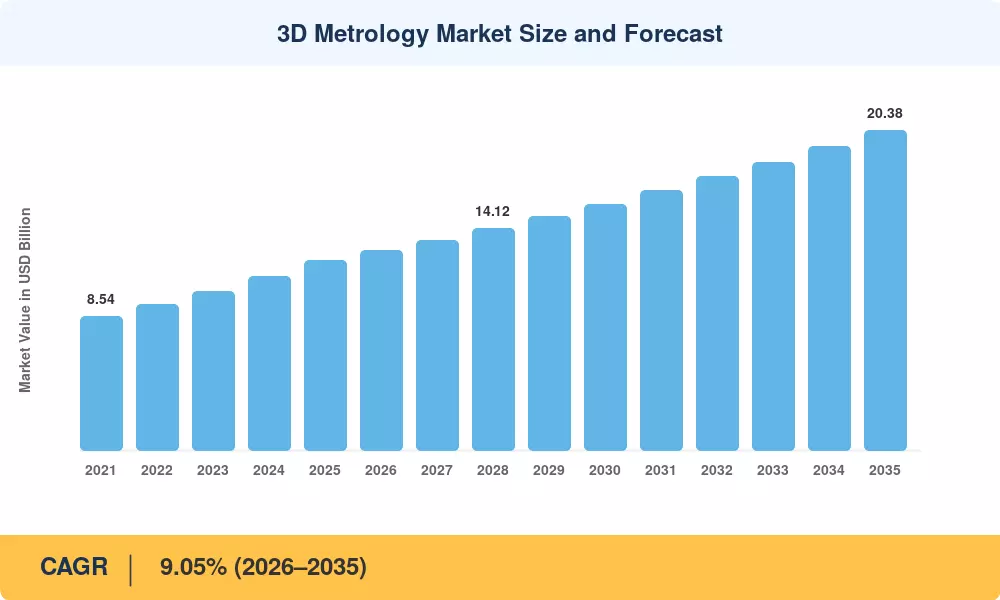

The 3D Metrology Market reached an estimated USD 12.07 billion in 2025 and is projected to grow from USD 12.79 billion in 2026 to USD 20.38 billion by 2035, registering a CAGR of 5.98% during the forecast period. This expansion is anchored in tightening dimensional tolerances across automotive, aerospace, and medical device production lines, where regulators now demand full traceability of every critical feature. Government-backed smart manufacturing initiatives — including China's "Made in China 2025" extension programs and the U.S. CHIPS and Science Act allocations for advanced metrology infrastructure — are accelerating capital expenditure on precision 3D measurement systems [1][2].

A technology transformation is reshaping the competitive landscape of the 3D Metrology Market. Legacy contact-based coordinate measuring machines are steadily giving way to non-contact optical 3D scanning metrology platforms that deliver faster throughput and richer point-cloud datasets. Inline inspection cells equipped with laser trackers and structured-light sensors now replace end-of-line sampling stations, cutting cycle times by 30–40% in high-volume plants [3]. Investment in CMM 3D inspection tools with integrated AI-driven defect classification exceeded USD 1.8 billion globally in 2024, signaling strong confidence in automated quality workflows [4].

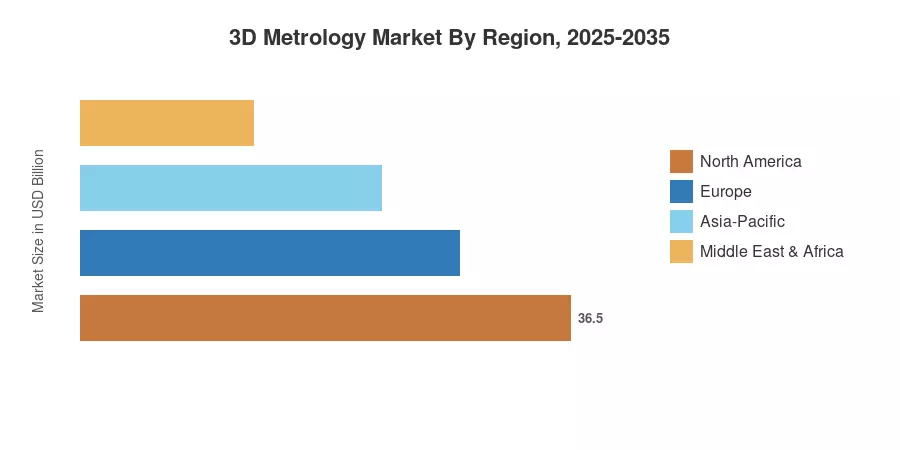

Asia-Pacific commands roughly 55.2% of the global 3D Metrology Market revenue, driven by China's massive electronics and EV assembly capacity and South Korea's semiconductor fabrication buildout. Europe holds the second-largest share at approximately 22.5%, buoyed by Germany's Industrie 4.0 mandates and France's aerospace cluster investments. North America is the third-largest region but leads in adoption of 3D surface profiling tools for medical implant verification, while the Middle East & Africa represents the fastest absolute growth pocket outside Asia-Pacific, owing to infrastructure megaprojects in Saudi Arabia and the UAE[6].

Key Report Takeaways

• By Component

- Hardware accounted for a 70.1% share of the 3D Metrology Market in 2025, reflecting heavy capital investment in CMM 3D inspection tools and laser tracker systems

- Services are forecast to expand at a 9.05% CAGR through 2035, fueled by calibration, training, and managed-inspection contracts

• By Hardware Type

- Coordinate measuring machines generated USD 4.88 billion in 2025, maintaining their role as the backbone of three-dimensional measurement systems in production environments

- Laser scanners are projected to grow at a 6.72% CAGR as manufacturers prioritize non-contact optical 3D scanning metrology for delicate components

• By Application

- Quality control & inspection captured 47.6% of the 3D Metrology Market in 2025, confirming precision 3D measurement as the primary use case

• By End-User Industry

- Automotive held a 31.5% revenue share in 2025, while medical & dental is the fastest-growing vertical at a 7.18% CAGR

• By Region

- Asia-Pacific contributed 55.2% of the global 3D Metrology Market sales in 2025, with a 6.02% CAGR projected for 2026–2035

- North America represented USD 2.65 billion in 2025, driven by aerospace and defense inspection mandates

Market Size and Forecast (2021–2035)

MRFR's market sizing integrates bottom-up revenue modeling from equipment OEM shipment data, software license revenues, and service contract values, cross-validated against top-down macroeconomic indicators including manufacturing value-added output and industrial automation capital expenditure trends.

.webp?v=1783604733)