Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Product Type | Bolts and Screws; Nuts and Collars; Rivets and Blind Fasteners; Pins and Inserts; Specialty / Panel Fasteners | Bolts and Screws | Specialty / Panel Fasteners |

| Material | Aluminum Alloy; Titanium Alloy; Steel and Superalloy; Composite-Compatible Polymer | Titanium Alloy | Composite-Compatible Polymer |

| Application | Commercial Aircraft; Military Aircraft; General Aviation; Unmanned Aerial Vehicles | Commercial Aircraft | Unmanned Aerial Vehicles |

| End-User | Commercial; Military | Commercial | Military |

| Region | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America | Asia-Pacific |

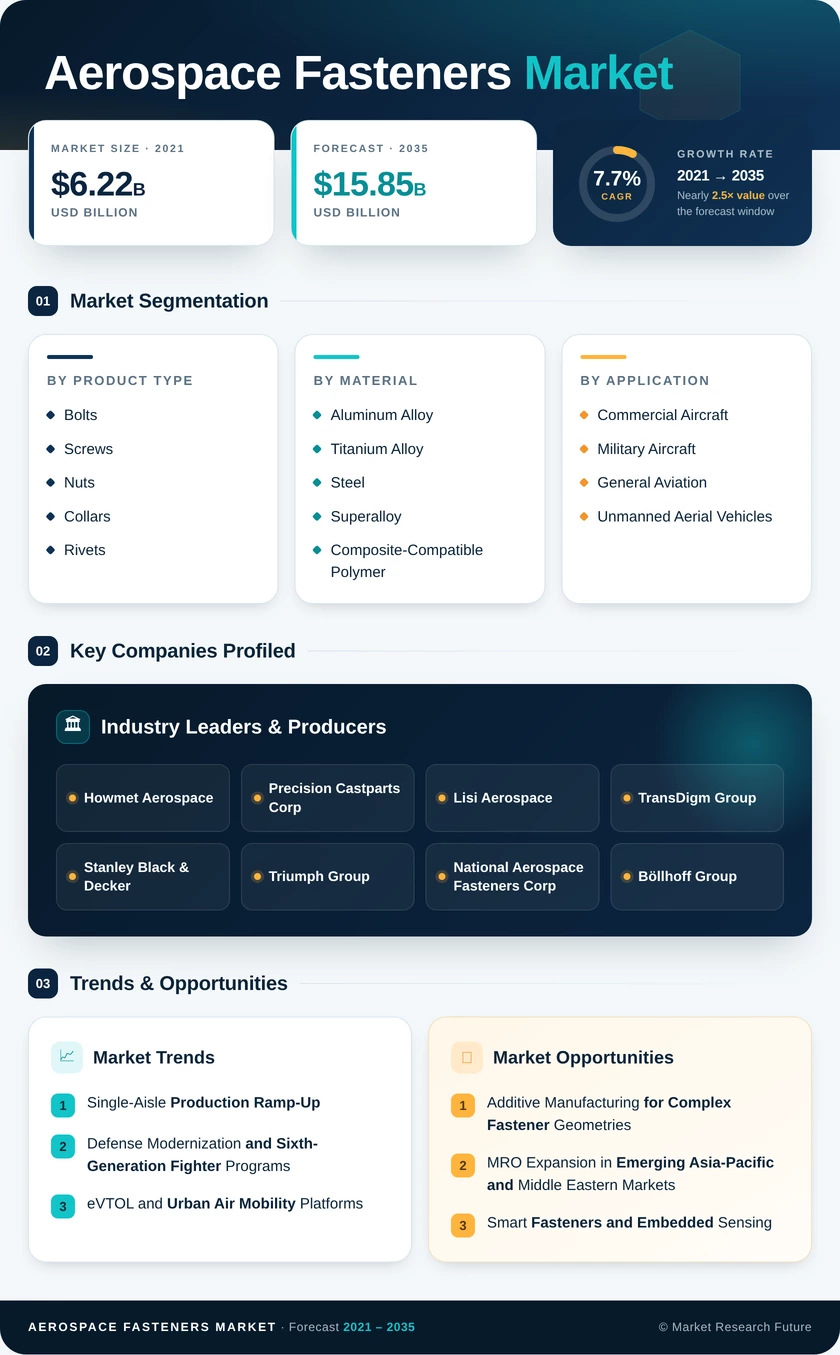

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Bolts and Screws | Largest segment; demand driven by primary structural assembly in fuselage and wing joins |

| Nuts and Collars | Growth linked to engine-pylon and landing-gear locking-assembly requirements |

| Rivets and Blind Fasteners | Automated robotic installation expanding share in fuselage skin-panel attachment |

| Pins and Inserts | Stable niche serving hinge and control-surface pivot applications |

| Specialty / Panel Fasteners | Fastest growing; propelled by cabin-interior programs and eVTOL quick-access designs |

Product-type segmentation reflects the functional hierarchy of aerospace structural assembly. Bolts and screws dominate by value because they carry the highest load requirements, while specialty and panel fasteners are gaining share as new aircraft architectures and accelerated interior-refresh cycles create demand for rapid-access, high-fatigue-cycle hardware.

By Material

| Sub-Segment | Key Trend |

| Aluminum Alloy | Cost-effective choice for secondary and non-corrosion-critical structures |

| Titanium Alloy | Dominant material; galvanic compatibility with CFRP drives sustained leadership |

| Steel and Superalloy | Critical for high-temperature engine and exhaust-system applications |

| Composite-Compatible Polymer | Fastest growing; adoption rising in secondary structures of CFRP-intensive airframes |

Material selection in the aerospace fasteners sector is dictated by the joint environment — temperature, load, and corrosion exposure. Titanium alloy maintains leadership due to its compatibility with composite airframes, while polymer-based solutions are emerging for secondary structures where weight savings and electrical isolation are prioritized.

By Application

| Sub-Segment | Key Trend |

| Commercial Aircraft | Dominant by volume; driven by record narrow-body and widebody backlogs |

| Military Aircraft | Growth fueled by sixth-generation fighter and trainer programs globally |

| General Aviation | Steady demand from business jet and turboprop fleet operations |

| Unmanned Aerial Vehicles | Fastest growing; ISR drones and delivery platforms scaling production volumes |

Application segmentation maps fastener demand to platform production volumes. Commercial aircraft represent the majority of consumption, but unmanned aerial vehicles are the most dynamic growth vector as military and commercial drone fleets expand rapidly across multiple geographies.

By End-User

| Sub-Segment | Key Trend |

| Commercial | Largest segment; includes OEMs, airlines, leasing companies, and Aerospace Fasteners Market providers |

| Military | Fastest growing; defense budget increases and fleet recapitalization programs drive demand |

End-user segmentation distinguishes between civil and defense procurement channels. Commercial end-users dominate by total volume, while military end-users benefit from multi-year defense procurement commitments that provide predictable, long-cycle fastener demand.