Automotive Fastener Market Summary

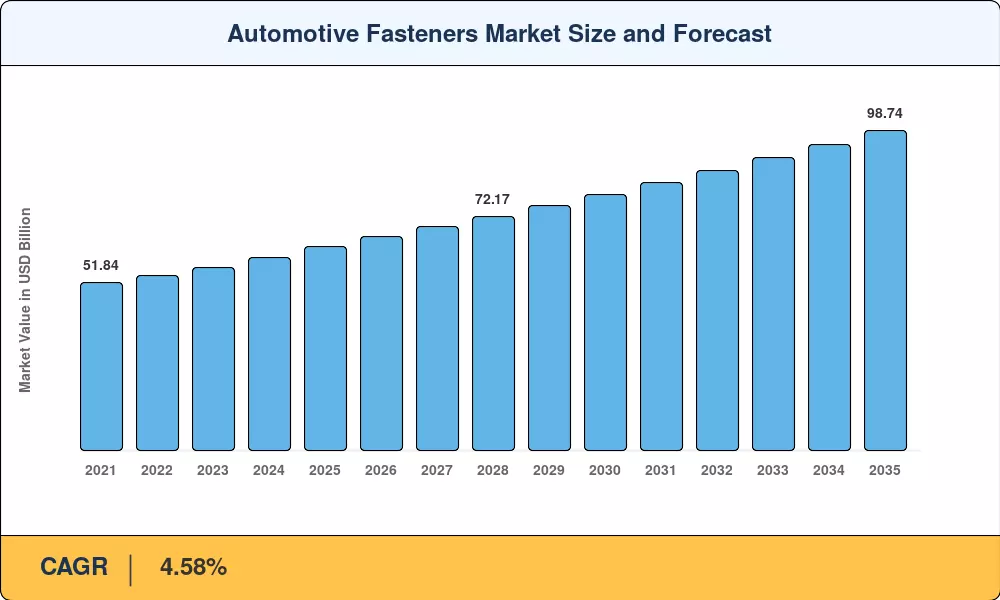

The Automotive Fasteners Market reached an estimated USD 63.10 Billion in 2025 and is projected to grow from USD 65.99 Billion in 2026 to USD 98.74 Billion by 2035, registering a CAGR of 4.58% during the forecast period (2026–2035). This trajectory reflects the sustained pull of global vehicle production recovery — forecast to surpass 95 million units by 2027 — alongside tightening safety-critical joint liability standards in the United States and European Union [1]. Corporate Average Fuel Economy (CAFE) targets and Euro 7 emission norms are forcing OEMs to adopt lighter chassis architectures, directly increasing the engineering complexity and per-vehicle value of fastening systems across passenger cars, commercial vehicles, and two-wheelers.

A significant transformation is reshaping the Automotive Fasteners Market as legacy carbon-steel threaded joints are progressively supplemented by advanced aluminum and titanium alloy variants designed for multi-material body structures. The European Commission's End-of-Life Vehicle Regulation (2024) mandates 30% recycled-content thresholds for metallic components by 2031, catalyzing investment in closed-loop fastener reprocessing lines [2]. Battery-electric vehicle platforms, while eliminating hundreds of powertrain-specific bolts, introduce new thermal-management and battery-enclosure fastening requirements that carry higher unit values.

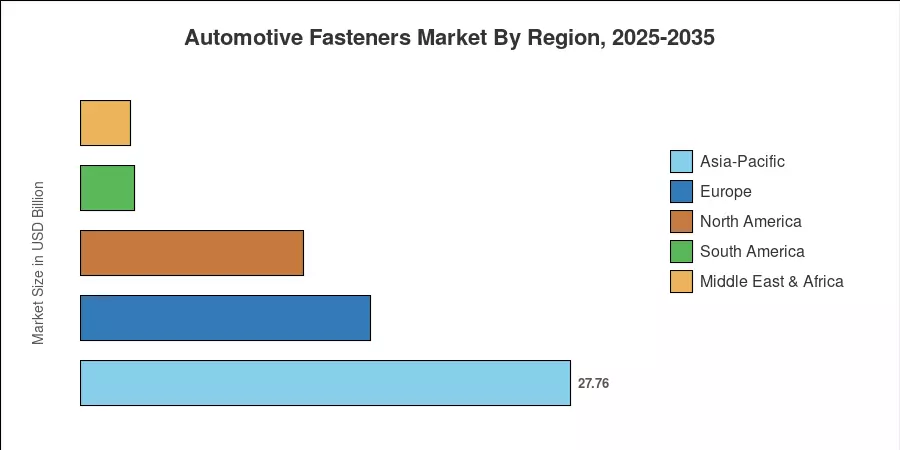

Asia-Pacific commands roughly 44% of global demand, driven by China's dominance in vehicle assembly and India's Production-Linked Incentive scheme for automotive components [3]. Europe holds approximately 26% share, anchored by German premium OEM specifications. North America, accounting for about 20% of the Automotive Fasteners Market, is witnessing procurement consolidation as modular platforms reduce the number of qualified tier-2 suppliers. Over the next decade, fastener digitization — torque-sensing smart bolts, RFID-tagged connectors — will open new value pools across all regions.

Key Report Takeaways

• By Fastener Type

- Threaded fasteners captured approximately 57% of the Automotive Fasteners Market revenue in 2025, reflecting their dominance in powertrain, chassis, and interior assemblies.

- Specialty and safety-critical fastener variants are projected to expand at a 4.55% CAGR as liability requirements intensify

• By Material

- Aluminum fasteners are forecast to record the fastest segment CAGR of 4.69% through 2035, propelled by lightweighting mandates across the EU and North American fleets.

• By Vehicle Type

- Passenger cars represented roughly 72% of the Automotive Fasteners Market in 2025, with compact crossovers driving incremental bolt counts.

• By Propulsion

- Battery-electric vehicle platforms are forecast to grow fastener demand at a 4.66% CAGR to 2035, despite lower unit counts per vehicle.

• By Region

- Asia-Pacific maintained the largest and fastest-growing regional position, with China alone contributing over USD 14 Billion in 2025.

- North America's fastener procurement value is rising as trade-defense duties on imported steel components push OEMs toward domestic suppliers.

Automotive Fasteners Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology integrates bottom-up OEM bill-of-material audits with top-down trade-flow analysis covering 28 fastener product categories across five propulsion architectures and seven application zones. Historical data (2021–2024) draws on customs declarations, industry association shipment records, and annual reports of the top fifteen global suppliers. Forecast projections (2026–2035) apply regression-adjusted demand elasticities tied to IHS Market vehicle-production schedules, lightweighting penetration curves, and electrification adoption rates.