Agricultural Fumigants Market Summary

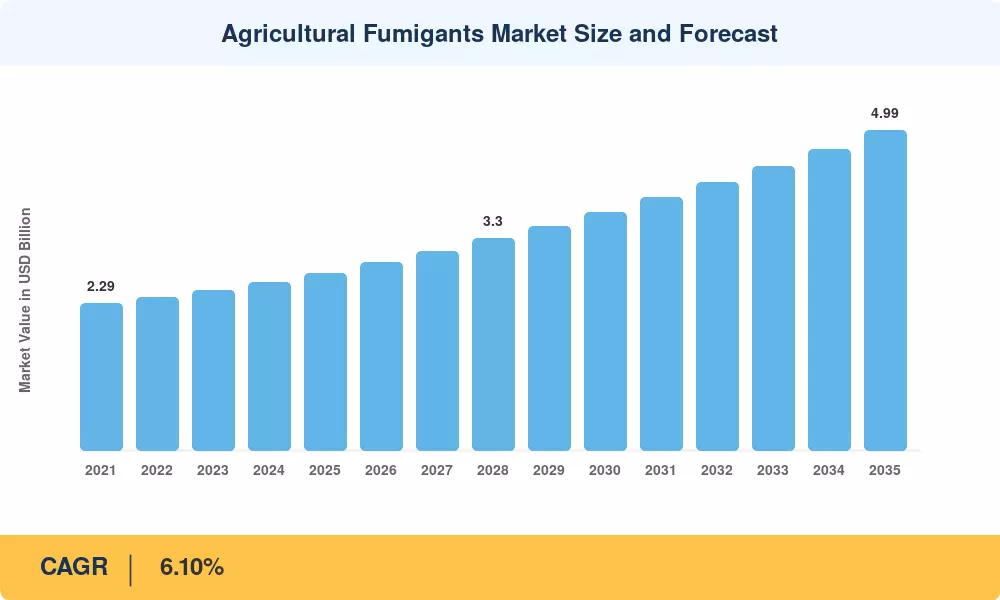

The Agricultural Fumigants Market was valued at USD 2.76 Billion in 2025 and is projected to grow from USD 2.93 Billion in 2026 to USD 4.99 Billion by 2035, registering a CAGR of 6.10% during the forecast period (2026–2035). Rising pest pressure across cereal, fruit, and vegetable supply chains — combined with tightening food-safety mandates from the Codex Alimentarius Commission and the US EPA's reregistration review schedule — is channeling fresh investment into chemical and non-chemical fumigation programs globally. The FAO estimates that pest- and disease-driven post-harvest losses still account for 14% of total food production, equivalent to roughly USD 220 billion annually, keeping the economic case for fumigant adoption firmly intact [2].

The market for agricultural fumigants is seeing a generational shift in technology. Growers and warehouse owners are moving toward precision-metered delivery systems, GPS-guided soil injection rigs, and integrated pest-management platforms that incorporate biological controls and fumigation due to the increasing regulatory phase-downs of legacy broad-spectrum compounds. A portion of the EUR 10 billion allocated by the EU's Farm to Fork Strategy until 2030 for sustainable crop-protection research specifically focuses on next-generation fumigant formulations and closed-loop application equipment [3].

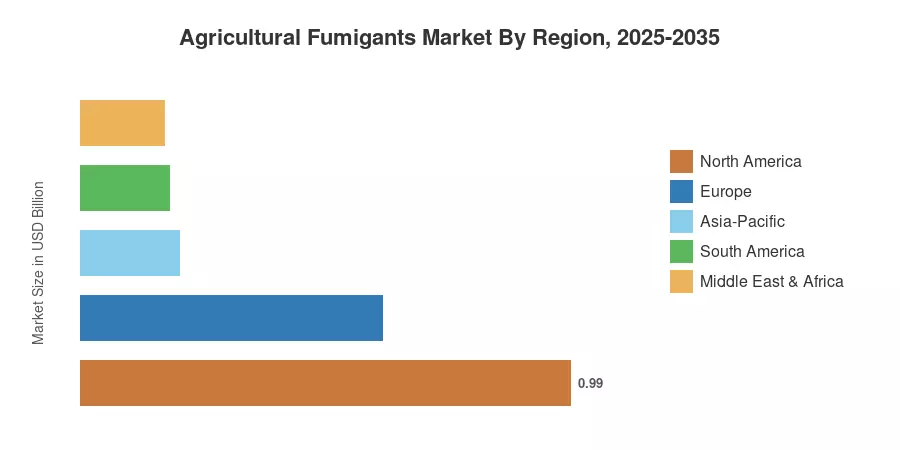

With high-value specialty crop production in California, Florida, and the Pacific Northwest, North America holds the greatest portion of the agricultural fumigants market, accounting for over 36% of global revenue. The fastest-growing region is Asia-Pacific, which is expected to increase at a CAGR of 7.3% through 2035 due to China's and India's expanding needs for grain storage. Due to strict maximum-residue-limit (MRL) rules that ironically boost demand for certified fumigant products, Europe has the second-largest market, at about 22%.

Key Report Takeaways

• By Type

- Phosphine leads the Agricultural Fumigants Market by type, accounting for approximately 28% of global revenue in 2025, owing to its cost-effectiveness and broad regulatory approval for stored-grain treatment.

- 1,3-Dichloropropene is the fastest-growing type segment, expanding at a CAGR of 7.1% through 2035 as growers in warm climates adopt it for pre-plant soil treatment.

- Metam Sodium generated an estimated USD 0.47 Billion in 2025 revenue, driven by demand across North American and European vegetable and strawberry cultivation.

• By Method of Application

- Soil-based fumigation holds a dominant share of approximately 58% in the Agricultural Fumigants Market, reflecting the critical role of pre-plant pest control in high-value horticulture.

- Warehouse fumigation is growing at a CAGR of 5.8%, as expanding grain reserve programs in Asia and Africa increase demand for post-harvest treatments.

• By Region

- North America remains the largest regional contributor to the Agricultural Fumigants Market, generating approximately USD 0.99 billion in 2025.

- Asia-Pacific is projected to register the fastest CAGR at 7.3% through 2035, driven by India's cereal storage modernization and China's integrated pest-management mandates.

- South America is an emerging growth pocket, with Brazil's expanding soybean and coffee export infrastructure pushing regional demand upward at 6.5% CAGR.

Agricultural Fumigants Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining bottom-up revenue analysis of leading fumigant producers, top-down consumption modeling calibrated against FAO crop-production statistics, and primary interviews with agrochemical distributors and regulatory officials across 25 countries. All historical figures reflect actual reported revenues and trade volumes; forecast values apply the calibrated 6.10% CAGR alongside region-specific adjustment factors for regulatory timelines and crop-mix shifts.

.webp?v=1783929758)