Agricultural Inoculants Market Summary

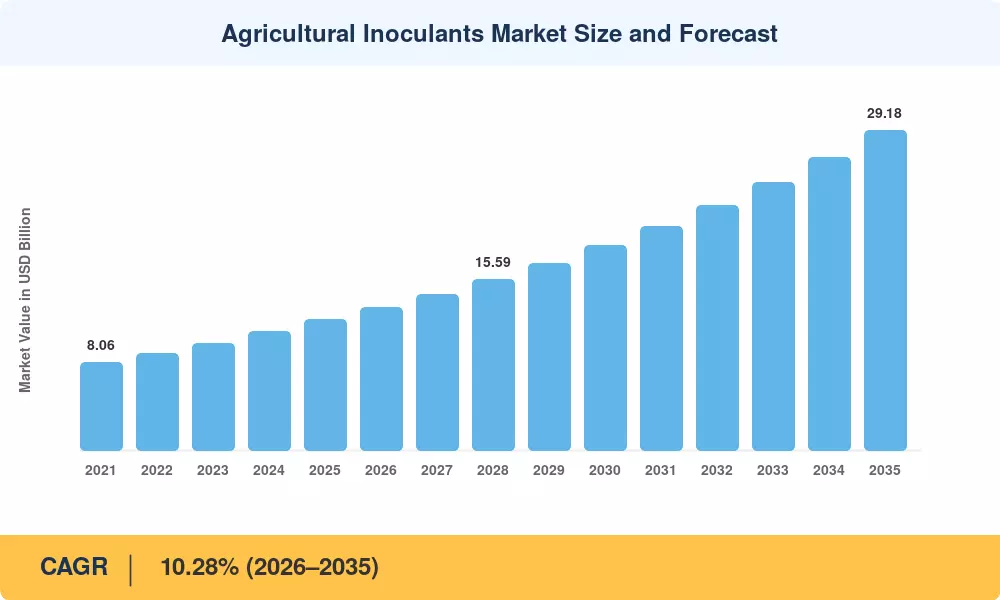

The Agricultural Inoculants Market reached an estimated USD 11.92 billion in 2025 and is projected to grow from USD 13.21 billion in 2026 to USD 29.18 billion by 2035, registering a CAGR of 10.28% during the forecast period. Carbon-credit incentive programs across North America and the EU's revised Common Agricultural Policy are channeling billions toward biological crop inputs, making microbial seed inoculants a core line item in grower input budgets. Venture capital flowing into encapsulation and shelf-life extension platforms — over USD 1.8 billion deployed globally between 2022 and 2025 — has accelerated commercialization timelines for next-generation rhizobium nitrogen-fixing bacteria strains and multi-species consortia [2][3].

A generational shift is underway in crop fertility management. Synthetic fertilizer dependency — which peaked at roughly 200 million metric tons of nutrient consumption globally — is being partially displaced by biofertilizer inoculant products engineered for precision delivery. The EU's Farm to Fork strategy targets a 20% reduction in chemical fertilizer use by 2030, directly elevating demand for mycorrhizal inoculant technology and bacterial nitrogen fixers that can close yield gaps without chemical runoff [4]. Precision agriculture platforms now integrate variable-rate microbial placement with satellite-guided seeding equipment, improving per-hectare ROI by an estimated 12–18% over broadcast methods [5].

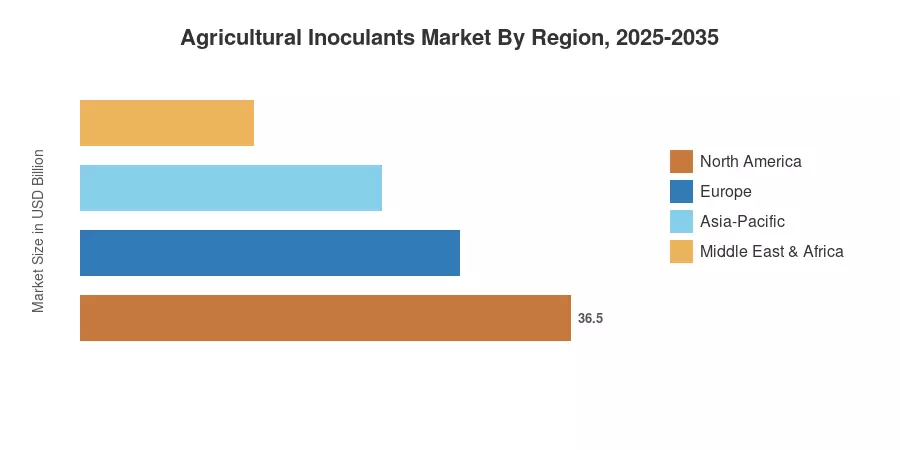

North America commands the largest share of the Agricultural Inoculants Market at approximately 35.1% of 2025 revenue, driven by soybean-dominant cropping systems and established dealer networks for soil microbiome enhancement products. Asia-Pacific is the fastest-growing region with a projected CAGR of 10.72% through 2035, fueled by India's biofertilizer subsidy programs and China's soil health restoration mandates. Europe holds the second-largest share at roughly 27%, anchored by organic farming expansion and tightening pesticide regulation

Key Report Takeaways

• By Function

- Crop nutrition held the dominant position in the Agricultural Inoculants Market with 63.4% share in 2025, reflecting entrenched use of rhizobium nitrogen-fixing bacteria in legume production systems

- Biocontrol agents are projected to advance at a 12.3% CAGR through 2035, propelled by integrated pest management mandates and resistance concerns around synthetic pesticides

• By Microorganism

- Bacterial inoculants generated USD 8.49 billion in 2025 revenue, anchored by decades of field validation for microbial seed inoculants in soybean and pulse crops

- Fungal inoculants — primarily mycorrhizal inoculant technology — are the fastest-growing segment at a 13.9% CAGR, expanding into horticultural and specialty crop applications

• By Mode of Application

- Seed inoculation led with 60.8% share of the Agricultural Inoculants Market in 2025, favored for dosing precision and labor efficiency

- Soil inoculation is projected to grow at a 13.5% CAGR through 2035 as granular and liquid soil-applied formulations gain traction in broadacre cereals

• By Crop Type

- Cereals and grains accounted for 44.6% of demand in 2025

- Fruits and vegetables represent the fastest-growing crop segment with an 11.8% CAGR, driven by premium pricing for residue-free produce

• By Region

- North America captured 35.1% of the 2025 global revenue in the Agricultural Inoculants Market

- Asia-Pacific is projected to post the highest regional CAGR at 10.72% through 2035, with India and China leading adoption of soil microbiome enhancement programs

Market Size and Forecast (2021–2035)

MRFR's forecast model integrates bottom-up revenue tracking from manufacturer shipments, distributor sell-through data, and regulatory filings across 42 countries. Historical figures (2021–2024) reflect actual reported revenues; the base year (2025) uses preliminary estimates; and the forecast horizon (2026–2035) applies the calibrated CAGR of 10.28% with adjustments for anticipated regulatory inflection points.

.webp?v=1785231588)