Agriculture Drones Market Summary

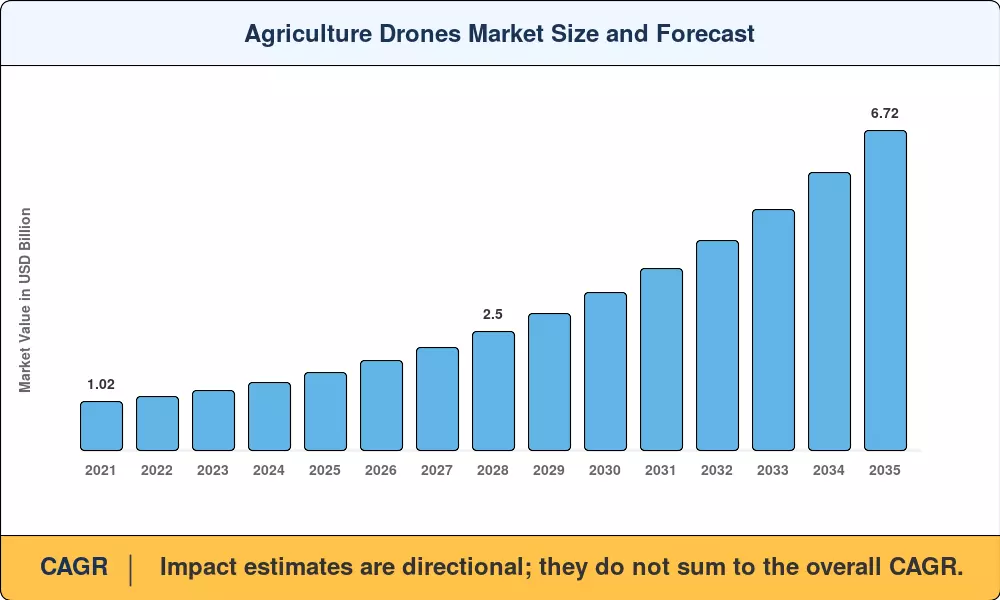

The Agriculture Drones Market reached USD 1.63 billion in 2025 and is projected to grow from USD 1.88 billion in 2026 to USD 6.72 billion by 2035, registering a CAGR of 15.2% during the forecast period (2026–2035). Rising input costs for fertilizers and crop-protection chemicals are pushing growers toward aerial platforms that can cut chemical usage by up to 30% through targeted application. National subsidy programs in the United States, India, and Australia have earmarked hundreds of millions of dollars for drone adoption, confirming government confidence in unmanned aerial vehicles as a tool for closing labor shortages on farms [1][2].

Technology revolution in Agriculture Drones Market is very well underway. Traditional ground-based scouting and manned aerial surveys are being replaced by sensor-equipped rotary-wing and hybrid VTOL planes capable of multispectral imaging, real-time variable-rate spraying and autonomous flight path execution. Edge AI chipsets now conduct field imagery analysis on board in seconds, and the proliferation of rural 5G connectivity guarantees that actionable data is delivered to farm management software in near real time [3]. The USDA plans to give out more than $300 million in grants for precision-agriculture technology between 2023 and 2025, and a large share of that funding will go to drone hardware and analytics integration [1].

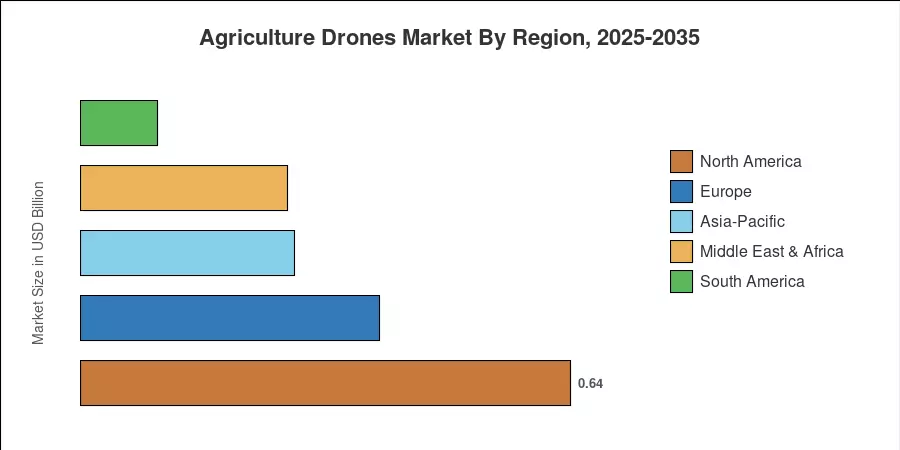

North America represents over 39% of the Agriculture Drones Market, driven by large-scale row crop farming in the U.S. Midwest and legal clarity provided by the FAA Part 107 rules. The Asia-Pacific region is the fastest growing region, and is expected to develop at a CAGR of 17.0% through 2035, driven by India’s Kisan Drone program and China’s rapid fleet expansion through XAG and DJI networks. Europe has the second highest share, at approximately 24% of the total, driven by incentives within the EU Common Agricultural Policy for digital farming. Together these three regions would contribute to the growth of Agriculture Drones Market in the forecast period.

Key Report Takeaways

• By Product

- Rotary-wing drones held approximately 57% of the Agriculture Drones Market share in 2025, reflecting their maneuverability advantage for field-level operations.

- Hybrid VTOL designs are forecast to expand at a 20.5% CAGR through 2035, the fastest-growing product segment in the Agriculture Drones Market.

• By Component

- Hardware accounted for roughly 59% of the Agriculture Drones Market in 2025, covering airframes, sensors, and GPS modules.

- Services are projected to advance at a 19.2% CAGR to 2035, fueled by drone-as-a-service subscription models.

• By Application

- Crop monitoring captured an estimated 44% share of the Agriculture Drones Market in 2025.

- Crop spraying is anticipated to register a CAGR of 20.0% through 2035.

• By Farm Size

- Large-scale commercial farms represented 59% of Agriculture Drones Market revenue in 2025.

- Small and medium farms are poised to grow at a 19.0% CAGR as fleet-sharing cooperatives lower entry barriers.

• By Geography

- North America accounted for 39% of the Agriculture Drones Market in 2025.

- Asia-Pacific is projected to register the highest regional CAGR at 17.0% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) estimated historical figures by cross-referencing import-export statistics, drone-manufacturer shipping details, and farm-technology adoption surveys from the FAO and USDA. Forecast predictions employ bottom-up demand modeling spanning product, component, application, farm-size, and regional segments evaluated against top-down macroeconomic factors including agricultural GDP growth and rural infrastructure investment pipelines [4].

.webp?v=1782308167)