Airborne ISR Market Summary

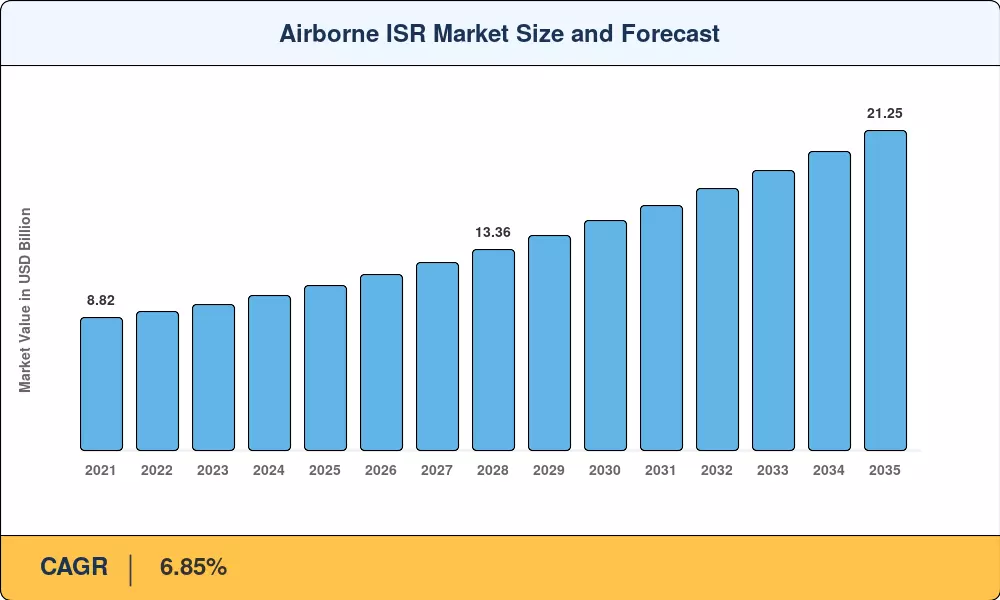

The Airborne ISR Market reached an estimated USD 10.95 billion in 2025 and is projected to grow from USD 11.70 billion in 2026 to USD 21.25 billion by 2035, registering a CAGR of 6.85% during the forecast period (2026–2035). This expansion is being driven by escalating geopolitical tensions across the Indo-Pacific, Eastern Europe, and the Middle East, combined with the U.S. Department of Defense's Replicator initiative targeting mass-scale deployment of attritable uncrewed platforms [1]. NATO allies collectively increased ISR-related procurement budgets by over 18% in FY2024 alone, signaling sustained demand through the decade [2].

A pronounced technology shift is reshaping how militaries collect and exploit aerial intelligence. Legacy manned platforms built around proprietary sensor buses are giving way to open-architecture configurations compliant with SOSA (Sensor Open Systems Architecture) and CMOSS (C5ISR/EW Modular Open Suite of Standards), reducing upgrade timelines from years to months [3]. The Pentagon's FY2025 budget allocated USD 2.4 billion specifically toward next-generation airborne reconnaissance payloads and AI-driven processing-exploitation-dissemination (PED) pipelines [4]. These investments are compressing sensor-to-shooter timelines below five minutes for the first time at scale.

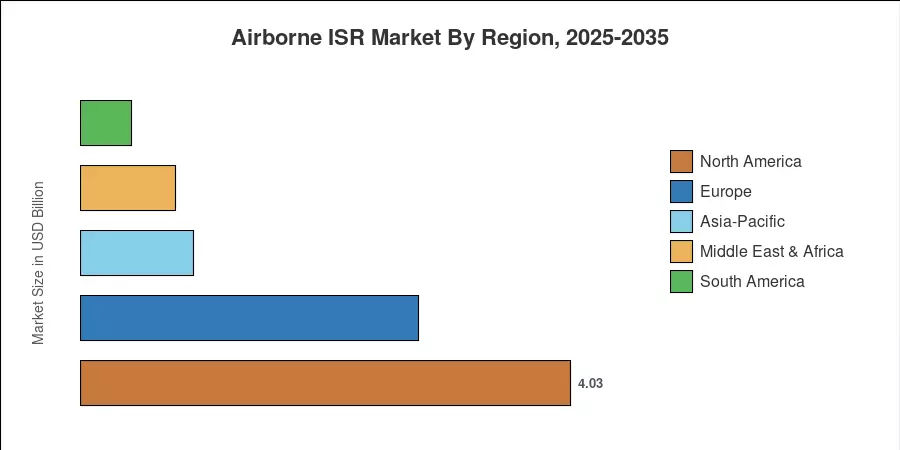

North America commands the largest share of the Airborne ISR Market at approximately 36.8% of global revenue, anchored by U.S. Air Force and Army programs such as ABMS and TITAN [5]. Asia-Pacific stands as the fastest-growing region with an anticipated CAGR of 8.50%, fueled by modernization drives in India, Japan, and South Korea. Europe holds the second-largest regional position, where rising defense expenditure among EU member states is accelerating procurement cycles for both manned and unmanned ISR assets through 2035.

Key Report Takeaways

• By Platform Type

- Manned aircraft platforms accounted for 76.0% of the Airborne ISR Market in 2025, reflecting continued reliance on modified fixed-wing airframes for long-endurance missions.

- Unmanned systems are projected to expand at a CAGR of 11.20% through 2035, driven by cost-per-flight-hour advantages and reduced crew risk.

• By Solution

- Hardware-centric systems (sensors, gimbals, datalinks) commanded approximately 76.2% of the Airborne ISR Market share in 2025.

- Software and analytics platforms are forecast to grow at a 9.18% CAGR between 2026 and 2035, reflecting the shift toward recurring-revenue PED models.

• By Application

- Warfare missions represented 38.5% of revenue in 2025, remaining the largest application category.

- Environmental monitoring applications are expected to register the fastest growth among application segments through 2035.

• By End User

- Defense organizations contributed 61.0% of the Airborne ISR Market revenue in 2025.

- The commercial and civil segment is projected to record the highest CAGR over the forecast period, led by disaster-response and infrastructure-inspection use cases.

• By Region

- North America led the Airborne ISR Market with a 36.8% share in 2025, anchored by U.S. DoD program spending.

- Asia-Pacific is expected to achieve the highest regional CAGR of 8.50% between 2026 and 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining top-down defense-budget analysis, bottom-up platform-level procurement tracking, and are validated through primary interviews with program managers and OEM executives across 15 countries.