Aircraft Lightning Protection Market Summary

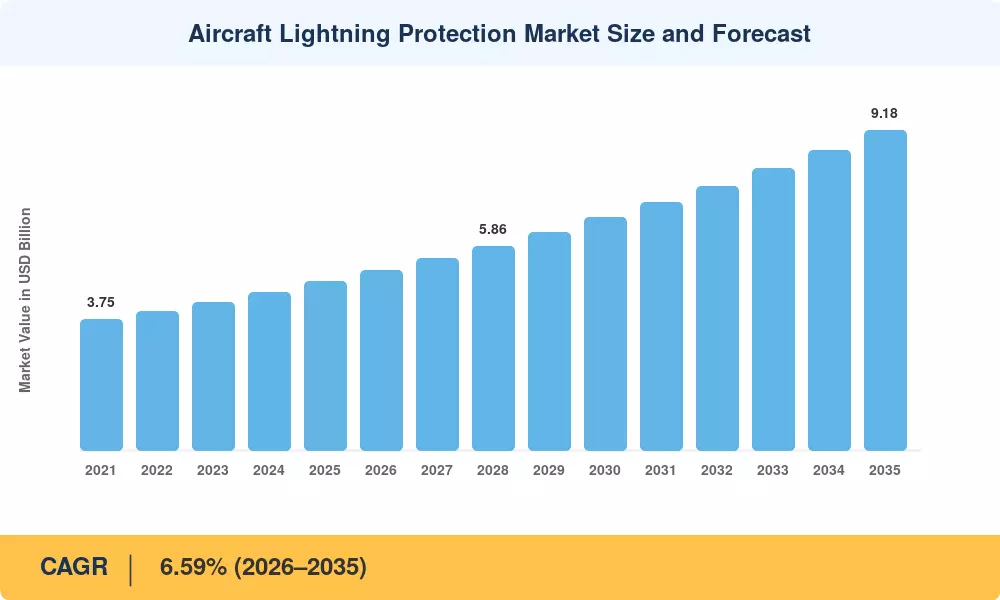

The Aircraft Lightning Protection Market stood at USD 4.84 billion in 2025 and is projected to reach USD 5.18 billion in 2026 before climbing to USD 9.18 billion by 2035, registering a CAGR of 6.59% over the 2026–2035 forecast window. Two policy catalysts anchor this trajectory: the FAA's updated Advisory Circular AC 20-53B mandating enhanced lightning strike certification for composite-intensive airframes, and EASA's 2024 Special Condition SC-VTOL requiring full lightning protection compliance for electric vertical takeoff and landing (eVTOL) platforms. Record commercial aircraft backlogs—exceeding 15,000 units across Boeing and Airbus combined—ensure sustained OEM procurement of qualified composite fuselage lightning shielding materials through the decade.

A generational technology shift is reshaping the Aircraft Lightning Protection Market. Traditional aluminum-skinned fuselages offered inherent conductivity, but the industry's pivot toward carbon-fiber-reinforced polymer (CFRP) airframes eliminates that natural safeguard. Every new composite aircraft delivery now requires conductive foils, interwoven wire meshes, or nanomaterial coatings to channel lightning strike energy safely across aircraft lightning strike zones. Boeing allocated over USD 450 million toward lightning protection R&D for the 777X program alone, signaling the capital intensity of this transition [2]. Static discharge aircraft systems and advanced lightning protection avionics now represent mandatory line items in every next-generation platform's bill of materials.

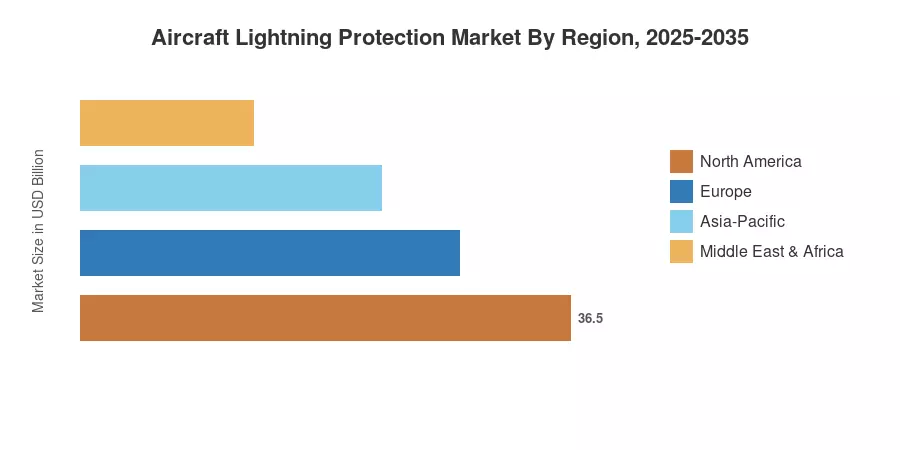

North America commands roughly 35.40% of the Aircraft Lightning Protection Market, anchored by the U.S. defense-industrial base and commercial OEM ecosystem. Asia-Pacific emerges as the fastest-growing region at an 8.22% CAGR, propelled by China's airport expansion program targeting 280 operational facilities by 2026 and India's UDAN regional connectivity scheme [3]. Europe holds the second-largest position with approximately 27% share, driven by Airbus production ramp-ups and stringent EASA certification mandates. The next decade will see aircraft EMI shielding and composite fuselage lightning shielding demand compound as electrification and autonomy reshape fleet architectures worldwide.

Key Report Takeaways

• By Product Type

- Expanded metal foils captured 52.15% of Aircraft Lightning Protection Market revenue in 2025, reflecting their entrenched qualification status across legacy and current-generation platforms

- Plated carbon fiber is advancing at a 7.92% CAGR through 2035, driven by demand for weight-efficient composite fuselage lightning shielding in next-generation narrowbodies

• By Aircraft Type

- Fixed-wing platforms accounted for USD 2.95 billion in the Aircraft Lightning Protection Market in 2025, sustained by commercial backlog fulfillment and military modernization cycles

- eVTOL/urban air mobility is the fastest-expanding segment at a 10.64% CAGR, reflecting regulatory certification progress and air-taxi fleet orders

• By Fit

- Line-fit installations represented 75.90% of the Aircraft Lightning Protection Market in 2025, as OEMs integrate protection systems during initial assembly

- Retrofit demand is growing at 7.41% CAGR as aging fleet operators upgrade static discharge aircraft systems to meet updated airworthiness directives

• By End User

- Defense forces held a dominant share, with naval aviation accounting for the largest procurement volumes for lightning protection avionics

- Civil/commercial customers represent the fastest growth at 9.32% CAGR through 2035

• By Geography

- North America retained 35.40% of 2025 Aircraft Lightning Protection Market revenue

- Asia-Pacific is the fastest-growing region at 8.22% CAGR, led by fleet expansion in China and India

Aircraft Lightning Protection Market Size and Forecast (2021-2035)

MRFR's market sizing integrates bottom-up revenue modeling from 85+ OEM and Tier-1 supplier disclosures, cross-validated against top-down demand estimates derived from global aircraft delivery projections, MRO expenditure databases, and regulatory compliance cost benchmarks [4].