Aircraft Seals Market Summary

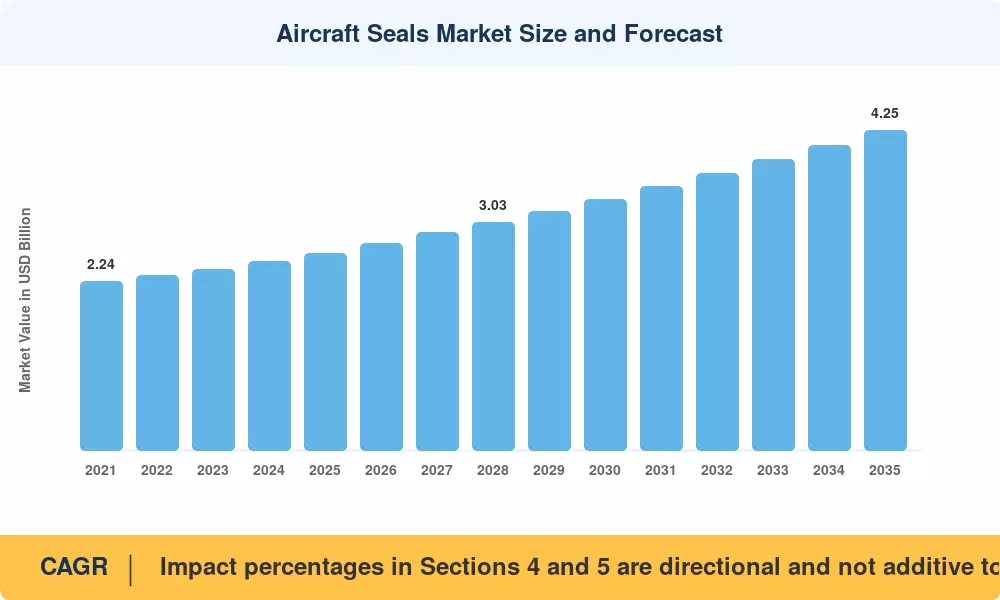

The global Aircraft Seals Market was valued at USD 2.62 billion in 2025 and is projected to grow from USD 2.75 billion in 2026 to USD 4.25 billion by 2035, registering a CAGR of 4.95% during the forecast period. Record commercial-aircraft backlogs are sustaining replacement and OEM demand — Boeing alone forecasts roughly 44,000 new jet deliveries through 2043, while Airbus accelerated its A320neo production cadence to 75 units per month by late 2025 [1][2]. These backlogs translate directly into multi-year procurement pipelines for sealing components across engines, airframes, and flight-control systems.

Material science is changing the heart of the Aircraft Seals Market. Legacy fluoropolymer compounds are being challenged from two directions: more stringent fire-safe and zero-leakage mandates under revised FAA TSO-C77b and EASA CS-25.856 specifications, and proposed PFAS restrictions across the European Union that could disqualify thousands of qualified part numbers by the late 2020s [3][4]. Supplier lead times for new-program installations are being reduced 30–40% using fluorosilicone blends, sophisticated PTFE composites and additive-manufactured seal designs [5]. A new, yet valuable, level of R&D expenditure is cryogenic-grade seals for hydrogen propulsion test rigs.

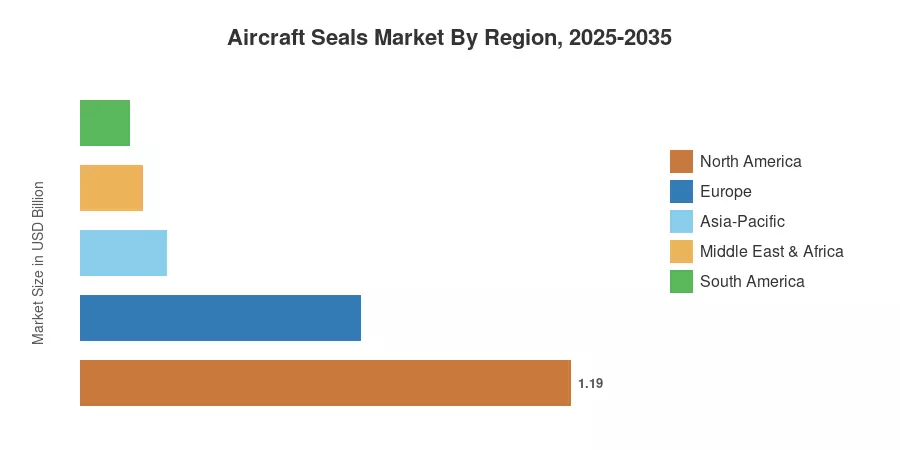

North America accounts for 45.3% of the Aircraft Seals Market, supported by defense procurement and the installed base of Pratt & Whitney / GE Aerospace engines. Asia-Pacific is the fastest-growing region at a projected CAGR of 7.85%, supported by narrowbody fleet expansion in China and India. Europe holds the second-largest share at approximately 25.8%, supported by ramp-ups in Airbus production and aftermarket programs for Rolls-Royce. The convergence of Advanced Air Mobility certification timelines and next-generation engine architectures will sustain demand trajectories through 2035.

Key Report Takeaways

• By Seal Type

- Dynamic seals accounted for 70.5% of the Aircraft Seals Market in 2024, reflecting their critical role in rotating and reciprocating engine assemblies.

- Inflatable seal configurations are forecast to expand at a 6.55% CAGR through 2035, driven by cabin-door pressurization and cargo-bay applications.

• By Application

- Engine systems held a 49.2% share of the Aircraft Seals Market in 2024, as turbine-section seals require frequent replacement at 5,000–8,000 flight-hour intervals.

- Environmental control and fuel-system applications are projected to grow at a combined 7.25% CAGR, buoyed by bleed-air redesign programs.

• By Material

- PTFE and composite grades captured 38.8% of the Aircraft Seals Market in 2024, reflecting their compatibility with wide-temperature envelopes.

- Fluorosilicone is poised for the fastest material-level CAGR at 7.52%, as OEMs pursue PFAS-free substitution roadmaps.

• By Aircraft Type

- Fixed-wing platforms commanded 73.2% share of the Aircraft Seals Market in 2024, spanning single-aisle through widebody fleets.

- Unmanned aerial vehicles are advancing at a 9.15% CAGR, propelled by defense ISR and commercial inspection use cases.

• By Geography

- North America dominated with a 45.3% share of the Aircraft Seals Market in 2024, supported by US DoD sustainment budgets exceeding USD 150 billion annually.

- Asia-Pacific is set to post a 7.85% CAGR through 2035, as Chinese and Indian carriers absorb 8,000+ new aircraft.

Market Size and Forecast (2021–2035)

MRFR’s sizing methodology combines primary interviews with Tier-1 seal manufacturers, procurement disclosures from airframe OEMs, and verified aftermarket demand models. Historical numbers (2021-2024) are taken from corporate filings and customs trade data; future values (2026-2035) are based on a calibrated 4.95% CAGR, using fleet delivery dates and MRO cycle assumptions.

.webp?v=1785231590)