Alfalfa Hay Market Summary

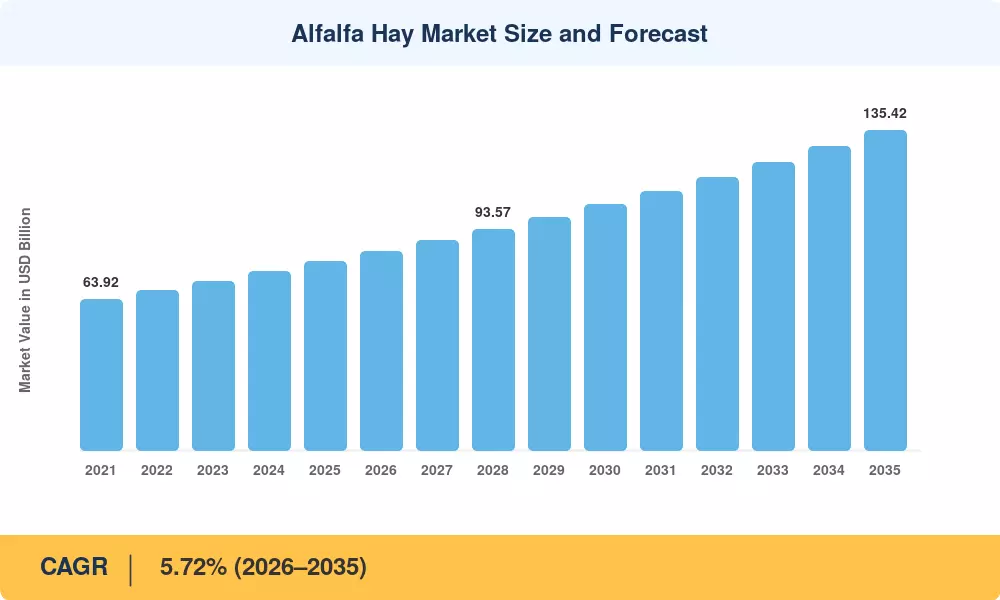

The global alfalfa hay market stood at USD 79.86 billion in 2025 and is projected to reach USD 135.42 billion by 2035, expanding at a CAGR of 5.72% over the 2026–2035 forecast window. Two powerful catalysts are propelling this trajectory: dairy intensification programs across Asia-Pacific nations, where governments are subsidizing domestic milk production to cut import dependency, and food-security mandates in the Middle East that have driven a 28% rise in premium alfalfa hay bale imports since 2022. Saudi Arabia's National Water Strategy alone has redirected over USD 1.2 billion in forage procurement toward imported sun-cured alfalfa hay nutrition products, as domestic cultivation faces strict groundwater withdrawal caps [2].

A silent transformation is happening in the processing landscape. Traditional field drying, still the standard practice for about 44% of global production, is gradually being replaced by solar-assisted dehydration and controlled-atmosphere systems, which can minimize spoiling losses by up to 35% [3]. Pelletized and compressed forms are now the fastest growing product category in the alfalfa hay market, since logistics improvements cut shipping costs by about 20% per metric ton relative to standard bales [4]. Investment in hay processing facilities totaled more than USD 800 million worldwide for 2023-2025.

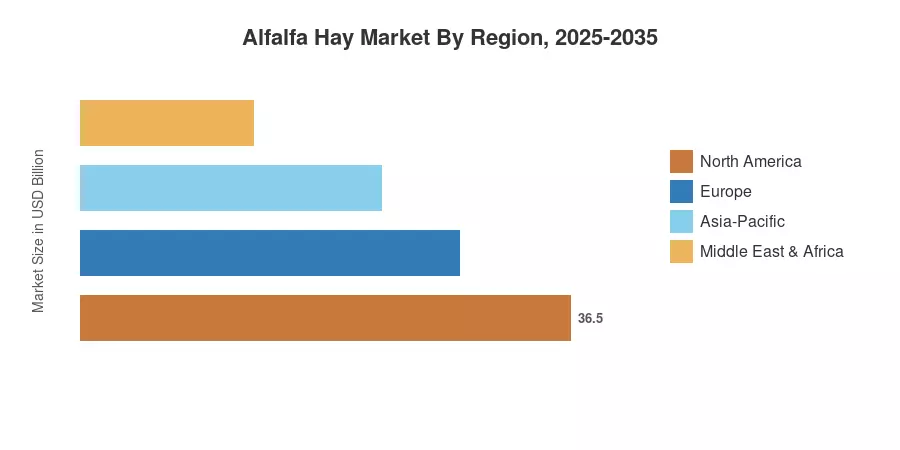

North America holds the greatest share in the alfalfa hay market with over 38.6% revenue share in 2025, driven by the production belt in the Western U.S. Asia-Pacific is the fastest expanding region with a forecast CAGR of 7.34% till 2035 due to the expansion of China’s dairy industry and increasing demand for dairy cow alfalfa feed in India Europe’s share is the second greatest, at about 22%, boosted by intensive cattle operations in Spain, France and Italy. The next decade promises considerable structural alterations in this market with changing production geography due to water shortages and accelerating alfalfa hay export and import flows.

Key Report Takeaways

• By Product Type

- Bales accounted for 45.3% of alfalfa hay market revenue in 2025, reflecting their dominance across conventional dairy cow alfalfa forage supply chains

- Dehydrated pellets are projected to expand at a 9.1% CAGR through 2035, driven by logistics cost advantages and premium alfalfa hay bale demand from equine and pet-food buyers

• By Livestock Application

- Dairy cattle feed represented USD 42.85 billion in 2025 value, underscoring the centrality of dairy cow alfalfa forage in global feed programs

- The pet-food and specialty segment is growing at a 9.7% CAGR through 2035, reflecting rising demand for traceable, dust-free premium alfalfa hay bale products

• By Geography

- North America led the alfalfa hay market with 38.6% revenue share in 2025

- Asia-Pacific is projected to grow at a 7.34% CAGR through 2035, the fastest among all regions

- Middle East & Africa alfalfa hay export-import activity surged, with Saudi Arabia and UAE accounting for over 60% of regional procurement value

Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology combining USDA production data, FAO trade statistics, customs-level alfalfa hay export-import records, and proprietary Market Research Future (MRFR) surveys of major producers and trading houses across 32 countries. Historical values reflect actual trade-weighted pricing; forecast figures apply Market Research Future (MRFR)'s calibrated CAGR model with adjustments for drought cycles, water-policy shifts, and dairy herd expansion projections.