Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

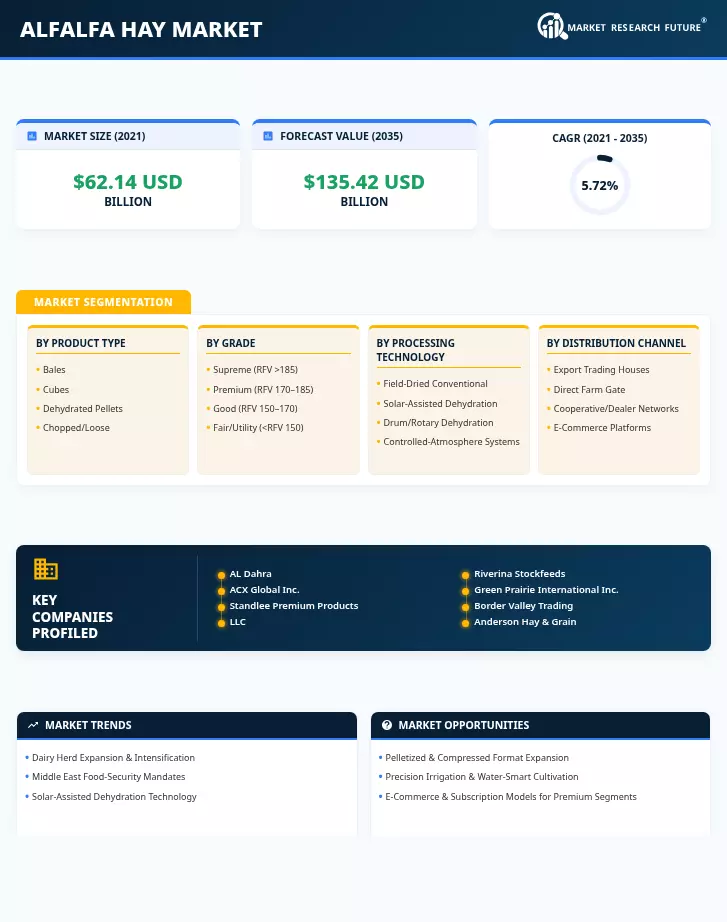

| Product Type | Bales, Cubes, Dehydrated Pellets, Chopped/Loose | Bales | Dehydrated Pellets |

| Grade | Supreme (RFV >185), Premium (RFV 170–185), Good (RFV 150–170), Fair/Utility ( | Premium (RFV 170–185) | Supreme (RFV >185) |

| Processing Alfalfa Hay Market | Field-Dried Conventional, Solar-Assisted Dehydration, Drum/Rotary Dehydration, Controlled-Atmosphere Systems | Field-Dried Conventional | Solar-Assisted Dehydration |

| Distribution Channel | Export Trading Houses, Direct Farm Gate, Cooperative/Dealer Networks, E-Commerce Platforms | Export Trading Houses | E-Commerce Platforms |

| Livestock Application | Dairy Cattle Feed, Beef Cattle Feed, Equine, Small Ruminant, Camel & Other | Dairy Cattle Feed | Equine |

| End-Use Sector | Commercial Farms, Smallholder/Family Farms, Pet-Food & Specialty | Commercial Farms | Pet-Food & Specialty |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Bales | Large-square bales dominate commercial trade; small-square bales serve equine and hobby channels. |

| Cubes | Steady demand from feedlots and equine buyers valuing portion-controlled feeding |

| Dehydrated Pellets | Fastest-growing format driven by export logistics efficiency and e-commerce retail |

| Chopped/Loose | Used primarily in total mixed ration (TMR) blending by commercial dairies |

Bales continue to anchor conventional supply chains, but format innovation is the defining trend in product-type segmentation. Pelletized and cubed formats are capturing share from loose and baled hay as buyers prioritize shipping density, shelf stability, and dust-free handling — particularly in cross-border alfalfa hay export-import routes.

By Grade

| Sub-Segment | Key Trend |

| Supreme (RFV >185) | Premium pricing driven by high-performance dairy and equine nutrition demands |

| Premium (RFV 170–185) | Mainstream standard for dairy cow alfalfa forage programs globally |

| Good (RFV 150–170) | Workhorse grade for beef cattle and general livestock operations |

| Fair/Utility ( | Declining share; used in biomass, erosion control, and budget feed blends |

Grade differentiation is intensifying as analytical testing becomes more accessible and buyers demand tighter nutritional specifications. The shift toward Supreme and Premium grades reflects the broader industry move toward precision nutrition and higher milk-per-ton feed efficiency.

By Processing Alfalfa Hay Market

| Sub-Segment | Key Trend |

| Field-Dried Conventional | Still dominant but losing share to technology-enhanced methods |

| Solar-Assisted Dehydration | Fastest-growing technology; superior nutrient retention at lower energy cost |

| Drum/Rotary Dehydration | Established in European cooperatives, high throughput, gas-dependent |

| Controlled-Atmosphere Systems | Emerging technology for premium-grade preservation and export readiness |

Processing technology is a key differentiator for producers seeking to capture premium pricing. Solar-assisted systems represent the convergence of sustainability and quality, reducing energy costs while preserving the sun-cured alfalfa hay nutrition profiles that high-value buyers demand.

By Distribution Channel

| Sub-Segment | Key Trend |

| Export Trading Houses | Dominant channel for cross-border trade; long-term offtake contracts growing |

| Direct Farm Gate | Regional procurement for nearby dairies and feedlots |

| Cooperative/Dealer Networks | Aggregation model serving mid-size buyers across diverse geographies |

| E-Commerce Platforms | Rapidly growing channel for premium alfalfa hay bale retail, subscription models |

E-commerce is the most disruptive channel trend, bringing lab-tested, traceable products to small-lot buyers who were previously underserved by traditional bulk distribution networks.

By Livestock Application

| Sub-Segment | Key Trend |

| Dairy Cattle Feed | Largest segment: driven by global dairy intensification and TMR adoption |

| Beef Cattle Feed | Stable demand in finishing and backgrounding rations |

| Equine | Fastest-growing application; sport-horse and recreational markets driving premiumization |

| Small Ruminant (Sheep/Goat) | Niche growth in artisanal and Mediterranean dairy operations |

| Camel & Other | Gulf region demand for camel nutrition and zoo/wildlife applications |

Dairy cattle feed remains the volume anchor, while equine and pet-food applications drive margin expansion and premium alfalfa hay bale innovation across the alfalfa hay market.

By End-Use Sector

| Sub-Segment | Key Trend |

| Commercial Farms | Dominant buyer segment: large-scale procurement, cost-optimized sourcing |

| Smallholder/Family Farms | Growing segment in developing markets as organized dairy scales up |

| Pet-Food & Specialty | Fastest-growing sector: rabbit, guinea pig, and specialty animal nutrition |

Commercial farms set the baseline for global demand. Still, the pet-food and specialty sector is introducing new quality standards, packaging formats, and direct-to-consumer business models that are reshaping competitive dynamics across the alfalfa hay market.