Amphibious Aircraft Market Summary

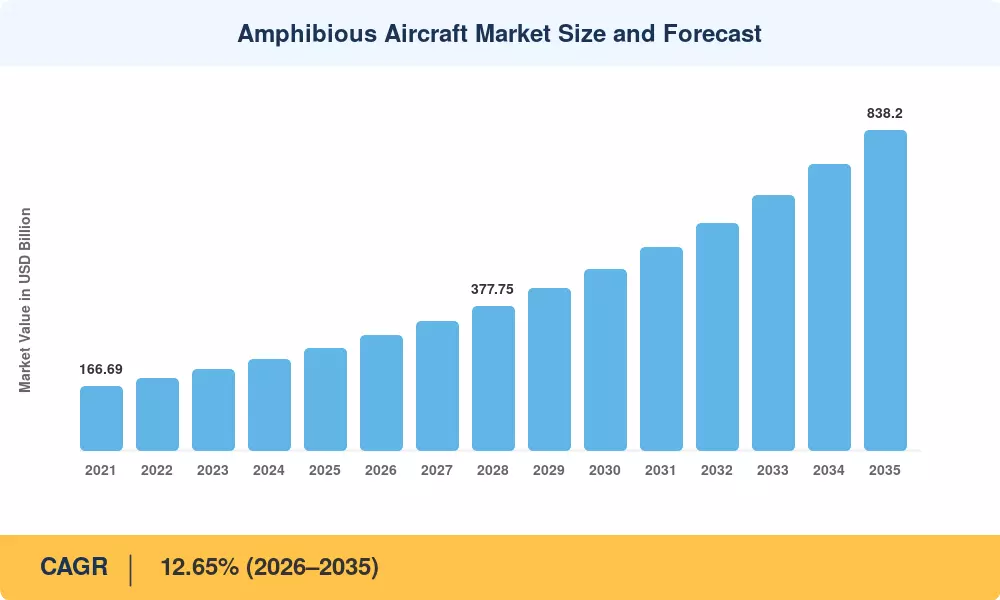

The amphibious aircraft Market reached USD 268.45 Million in 2025 and is positioned to climb to roughly USD 301.20 Million as the 2026 forecast period opens, before extending to USD 838.20 Million by 2035 at a 12.65% CAGR. Two catalysts anchor that trajectory: China's June 2025 production certification of the AG600, which made the country the only mass producer of 60-tonne airframes for firefighting and maritime patrol, and coordinated European agency procurement programs targeting 2028 fleet deliveries. Tight supply and long lead times have pushed operators toward early deposits and multi-year service contracts.

Propulsion is where the amphibious aircraft Market is changing fastest. Legacy piston and older turboprop platforms are giving way to modern turboprop airframes and, increasingly, hybrid/electric powertrains that promise lower operating costs for short inter-island hops. Manufacturers have committed capital toward certification of cleaner powertrains, and several seaplane floatplane amphibious programs now feature electrified demonstrators. Public firefighting budgets exceeding USD 1 billion across European member states underpin near-term airframe demand.

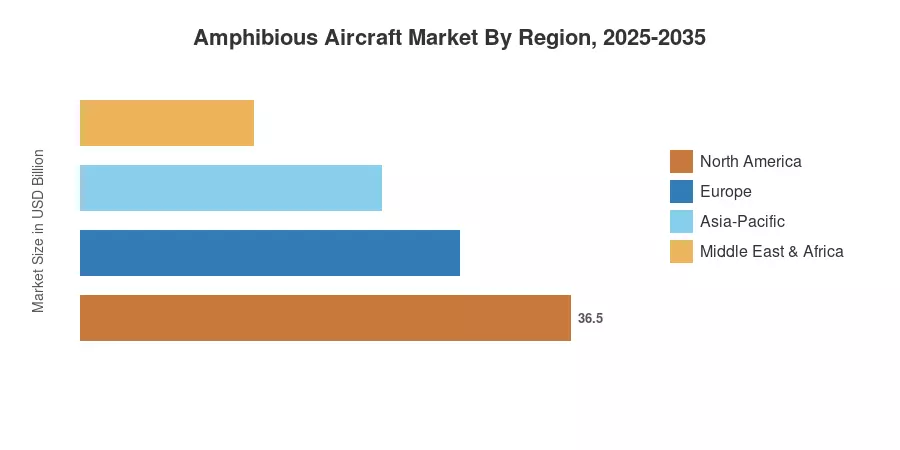

North America holds the dominant position with a 38.6% share of the amphibious aircraft Market, supported by mature utility amphibious aircraft design ecosystems and bush operations. Asia-Pacific is the fastest-growing region at a 13.4% CAGR, driven by inter-island connectivity. Europe ranks second on the strength of firefighting fleet renewal. Momentum should hold as supply normalizes.

Key Report Takeaways

• By Engine Type

- Turboprop platforms led the amphibious aircraft Market with a 42.8% share in 2025, reflecting their balance of payload and reliability for lake water landing aircraft missions

- Hybrid/electric propulsion is the fastest-expanding technology, projected at a 16.4% CAGR through 2035 as electrified seaplane floatplane amphibian demonstrators mature

• By Seating Capacity

- Passenger transport accounted for a 34.6% share of the amphibious aircraft Market in 2025, anchored by amphibious air transport service routes across island geographies

- Firefighting and search-and-rescue are forecast to grow at a 15.1% CAGR through 2035 as public agencies expand aerial response fleets

• By Region

- North America retained USD 103.62 Million of the amphibious aircraft Market in 2025, the largest regional pool

- Asia-Pacific is projected to record a 13.4% CAGR through 2035, the fastest among all regions

Market Size and Forecast (2021–2035)

Market sizing draws on MRFR's bottom-up modeling of fleet deliveries, operator order books, and service-contract revenue, triangulated against published aerospace estimates and regulatory certification records. Historical values reflect actual delivery data; forecast years apply a calibrated 12.65% CAGR.