Automated Dispensing Machines Market Summary

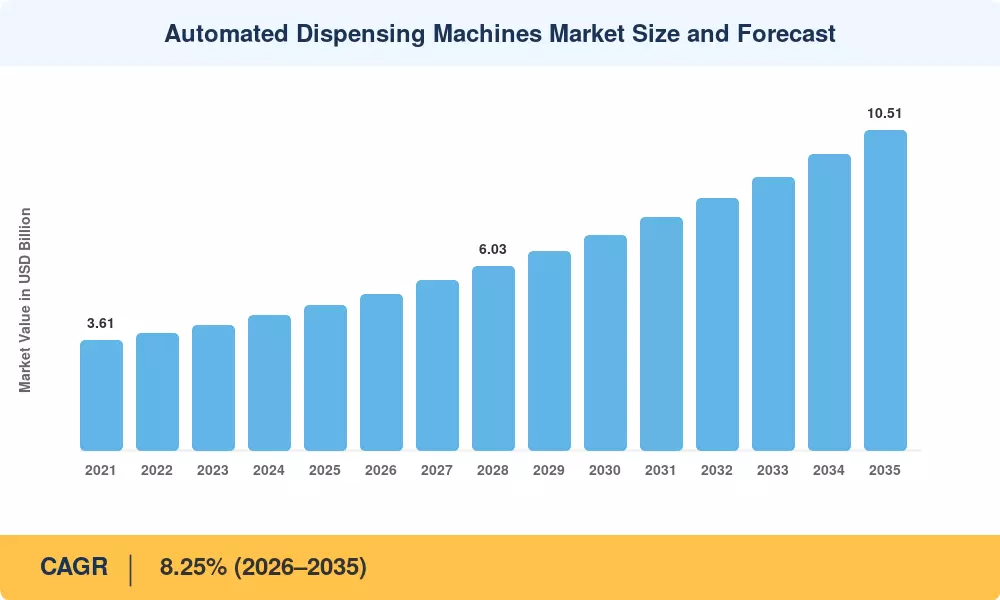

The Automated Dispensing Machines Market size was valued at USD 4.75 Billion in 2025, and the market is projected to grow from USD 5.14 Billion in 2026 to USD 10.51 Billion by 2035, registering a CAGR of 8.25% during the forecast period 2026–2035. Two catalysts anchor this trajectory: the DEA's expanded electronic prescribing mandate for controlled substances, which has pushed U.S. hospitals toward auditable point-of-care dispensing, and FDA Class II clearance pathways that have shortened time-to-market for remote medication management hardware.

Networked, sensor-driven cabinets that record every withdrawal against a patient record in real time are replacing legacy med-cart and manual cabinet procedures. Major U.S. health networks have committed $1.2 billion to pharmacy IT modernization since 2023 [1], a sign of a growing trend toward health systems buying hardware, analytics and cybersecurity as part of a single enterprise contract instead of point solutions.

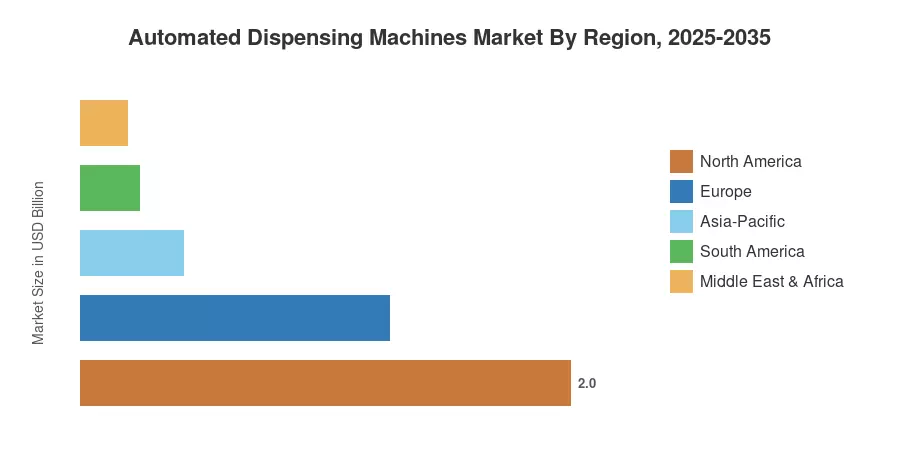

North America is the largest market, estimated to account for 42.2% of revenue in 2025, driven by dense hospital networks and pressure to comply with DEA regulations. Asia-Pacific is the fastest-growing region at a CAGR of 8.8%, with China, India, and South Korea funding modern pharmacy infrastructure. Europe is the runner-up, helped by the EU Falsified Medicines Directive serialization requirements. And the next decade will see vendors competing more on the depth of their software, not just their hardware.

Key Report Takeaways

• By Technology

- Automated dispensing cabinets held an estimated 41.2% share of the Automated Dispensing Machines Market revenue in 2024.

- Decentralized cabinet formats are expanding at roughly 11.5% CAGR through 2035 as bedside dispensing gains traction.

- Centralized robotic dispensing infrastructure generated an estimated USD 2.74 billion in 2025.

• By Sector

- Hospital inpatient pharmacies captured close to 60.1% of the Automated Dispensing Machines Market revenue in 2024.

- Retail and community pharmacy deployments are growing near 9.8% CAGR as chain pharmacies adopt narcotics tracking.

- Unit-dose oral solids accounted for an estimated 46.1% share of dispensed medication volume.

• By Geography

- North America led the Automated Dispensing Machines Market with an estimated 42.2% revenue share in 2024.

- Asia-Pacific is forecast to expand at approximately 8.8% CAGR through 2035.

- Europe contributed an estimated USD 1.26 billion in 2025 revenue.

Market Size and Forecast (2021–2035)

We combine data from hospital procurement, vendor shipment data and disclosures from regulatory filings and triangulate against national pharmacy infrastructure expenditure reports to generate a consistent series for the 2021-2035 period.