Automatic Content Recognition Market Summary

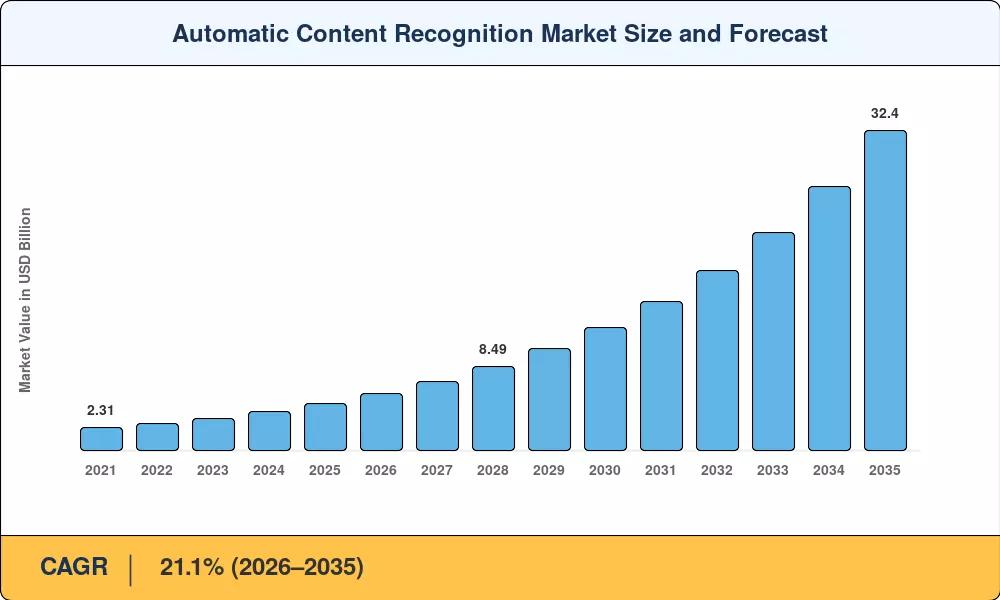

The Automatic Content Recognition Market reached USD 4.76 Billion in 2025, propelled by a decisive shift toward addressable television advertising and edge-AI chipsets capable of running fingerprinting workloads directly on consumer devices. From a 2026 starting value of USD 5.79 billion, the Automatic Content Recognition Market is projected to climb to USD 32.40 billion by 2035, registering a CAGR of 21.1% across the forecast window. Two catalysts stand out: the EU Digital Services Act's transparency mandates for content tracking, and major OEM commitments — exemplified by smart TV shipments crossing 290 million units globally in 2024 — that embed ACR silicon at the board level [1][2].

The competitive landscape is changing due to a shift in technology. Hybrid architectures that combine cloud-based matching engines with on-device audio-video signature extraction are replacing outdated server-side watermarking stacks. In an effort to commercialize second-screen interaction and real-time ad substitution, broadcasters and streaming services spent more than USD 1.2 billion in combined R&D on these next-generation platforms in 2024 [3]. The end product is a data ecosystem that simultaneously records viewing activity across HDMI-passthrough, OTT, and linear inputs.

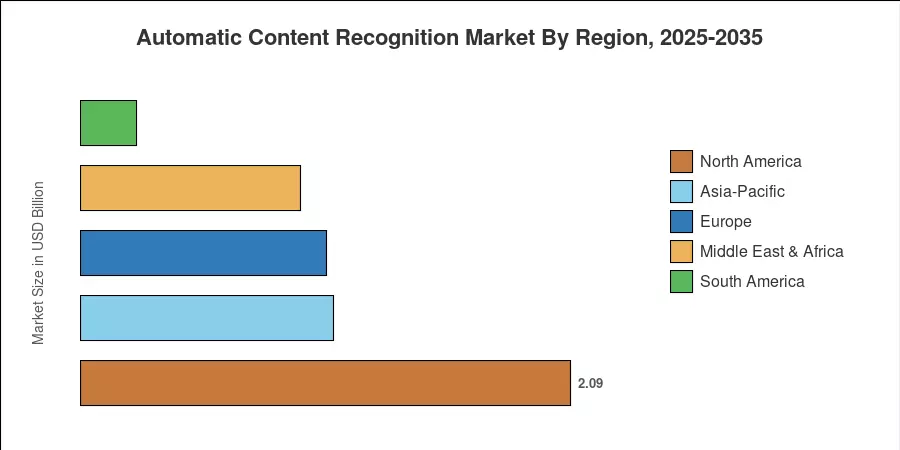

Programmatic TV budgets in the US are the main driver of North America's dominant 44% value share of the Automatic Content Recognition Market. With a 22.7% CAGR, Asia-Pacific is the fastest-growing area due to the spread of connected TV in South Korea, China, and India. Thanks to GDPR-compliant analytics frameworks that provide marketers with confidence in implementing recognition technology at scale, Europe accounts for about 22% of worldwide sales. The Automatic Content Recognition Market is expected to grow steadily in double digits through the mid-2030s as FAST channel economics develop, and vehicle infotainment usage picks up speed.

Key Report Takeaways

• By Component

- Software platforms commanded approximately 59% of the Automatic Content Recognition Market in 2025, reflecting entrenched licensing models for fingerprint databases and matching engines.

- Managed services are forecast to expand at a 22.1% CAGR through 2035, as broadcasters outsource compliance monitoring and model retraining to specialized vendors.

• By Technology

- Audio and video fingerprinting accounted for the largest technology share in the Automatic Content Recognition Market, reaching 48% of revenue in 2025.

- Digital watermarking maintained a stable installed base across pay-TV operators, valued at USD 1.08 billion in 2025.

• By End-User Industry

- Media and entertainment represented 41% of the Automatic Content Recognition Market spend in 2025.

- Automotive infotainment is forecast to register a 21.8% CAGR, fueled by voice-commerce pilot programs across major OEMs.

• By Region

- North America captured 44% of the global value in the Automatic Content Recognition Market during 2025.

- Asia-Pacific is compounding at 22.7% through 2035, the fastest pace among all regions.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates bottom-up revenue estimates from OEM shipment data, content-licensing fee pools, and enterprise software billings against top-down advertising-spend benchmarks published by IAB, Nielsen, and regional broadcasters [4][5].