Automatic Weapons Market Summary

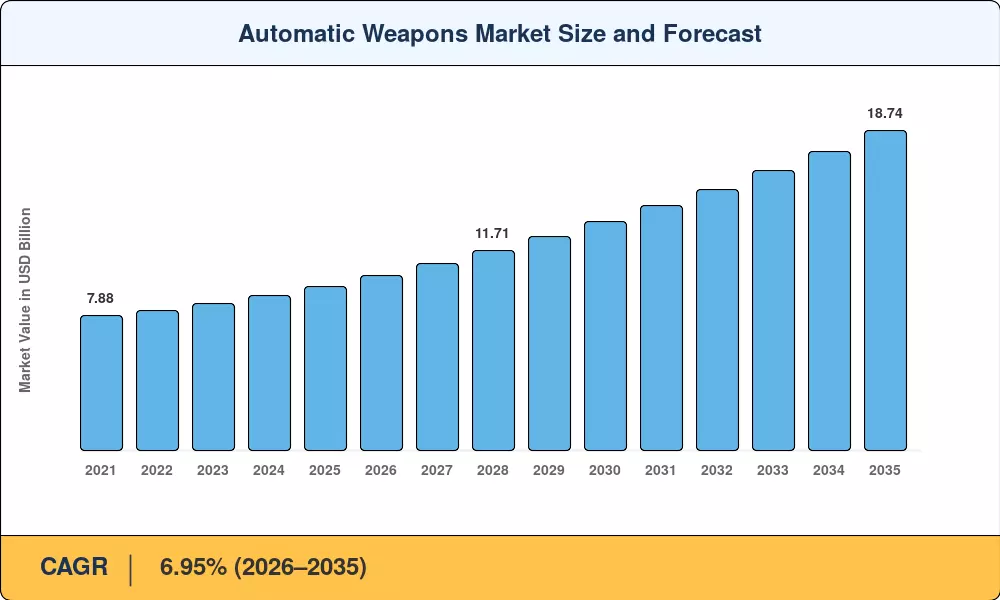

The Automatic Weapons Market stood at USD 9.58 billion in 2025 and is projected to reach USD 10.24 billion in 2026, climbing to USD 18.74 billion by 2035 at a CAGR of 6.95% during 2026–2035. Rising global defense budgets — the United States alone authorized USD 886 billion in its FY 2024 National Defense Authorization Act [1] — and accelerating force-modernization timelines across NATO and Indo-Pacific alliances are the primary spending catalysts fueling expansion of the Automatic Weapons Market.

A generational technology transition is changing procurement priorities. Cold War–era platforms chambered for outdated cartridges are making way to digitally networked, sensor-fused weapon systems capable of autonomous target tracking and real-time data interchange across joint combat networks. This shift towards higher velocity, modular-caliber platforms capable of peer-adversary engagements is seen in the U.S. Army’s Next Generation Squad Weapon (NGSW) program, which is expected to cost over USD 4.7 billion over its lifecycle [2]. EU Defense Industrial Strategy allocations [3] European states are investing in equal amounts in the Future Combat Air System and equivalent land-weapon upgrades.

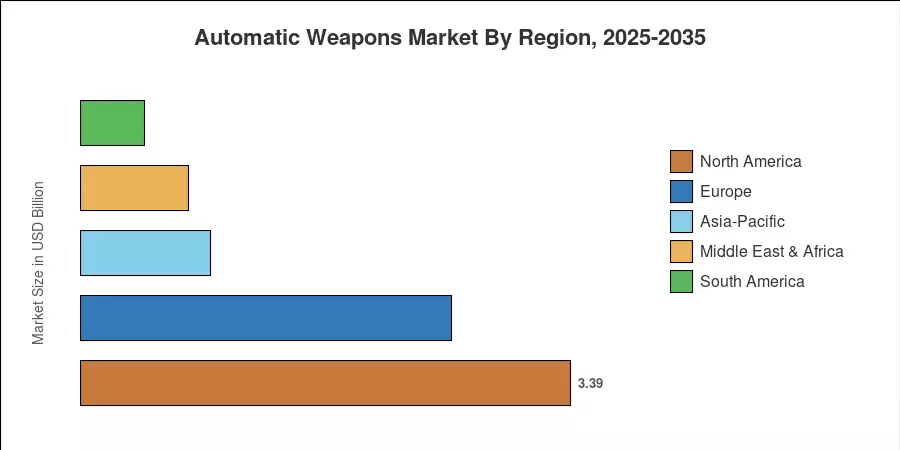

North America commanded the Automatic Weapons Market with a share of 35.40% in 2025, owing to ongoing Pentagon investment and a robust domestic industrial base. Asia-Pacific has the highest CAGR of 9.40% through 2035, with India, South Korea, and Japan in rearmament cycles. Europe was the second largest area, led by post-2022 defense spending hikes in Baltic and Nordic countries. The next decade will depend on the speed with which digitally integrated weapon stations are deployed globally to replace manually controlled older systems.

Key Report Takeaways

• By Type

- Automatic rifles captured 38.40% of the Automatic Weapons Market in 2025, reflecting widespread infantry modernization programs across NATO and allied forces.

- Automatic cannons are expanding at an 8.98% CAGR through 2035, driven by integration into unmanned turrets and remote weapon stations on armored vehicles.

• By Platform

- Land platforms dominated with a 62.30% share of the Automatic Weapons Market in 2025, as ground-force upgrades continue to absorb the bulk of ordnance budgets.

- Naval platforms exhibit the fastest growth at a 9.70% CAGR to 2035, fueled by littoral combat ship programs and corvette fleet expansions.

• By Caliber

- Small caliber systems accounted for USD 4.20 billion in 2025, underpinned by high-volume infantry and special operations demand.

- Large caliber weapons are growing at an 8.72% CAGR to 2035, as counter-drone and air-defense applications gain urgency.

• By End User

- The defense segment commanded 72.90% of the 2025 Automatic Weapons Market revenue.

- Special operations forces recorded a 10.35% CAGR to 2035, reflecting elite-unit modernization and counter-terrorism funding.

• By Geography

- North America retained a 35.40% share in 2025, led by U.S. Army and Marine Corps weapon-system contracts.

- Asia-Pacific posted the quickest 9.40% CAGR, with India, Japan, and South Korea driving regional acceleration in the Automatic Weapons Market.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a triangulated estimation process involving top-down military budget research, bottom-up OEM shipping tracking and government procurement data across 45 nations. Historical estimates (2021–2024) are based on actual delivery and contract data, whereas future values (2026–2035) are projected from the 2025 base year using scenario-weighted CAGR modeling.