Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

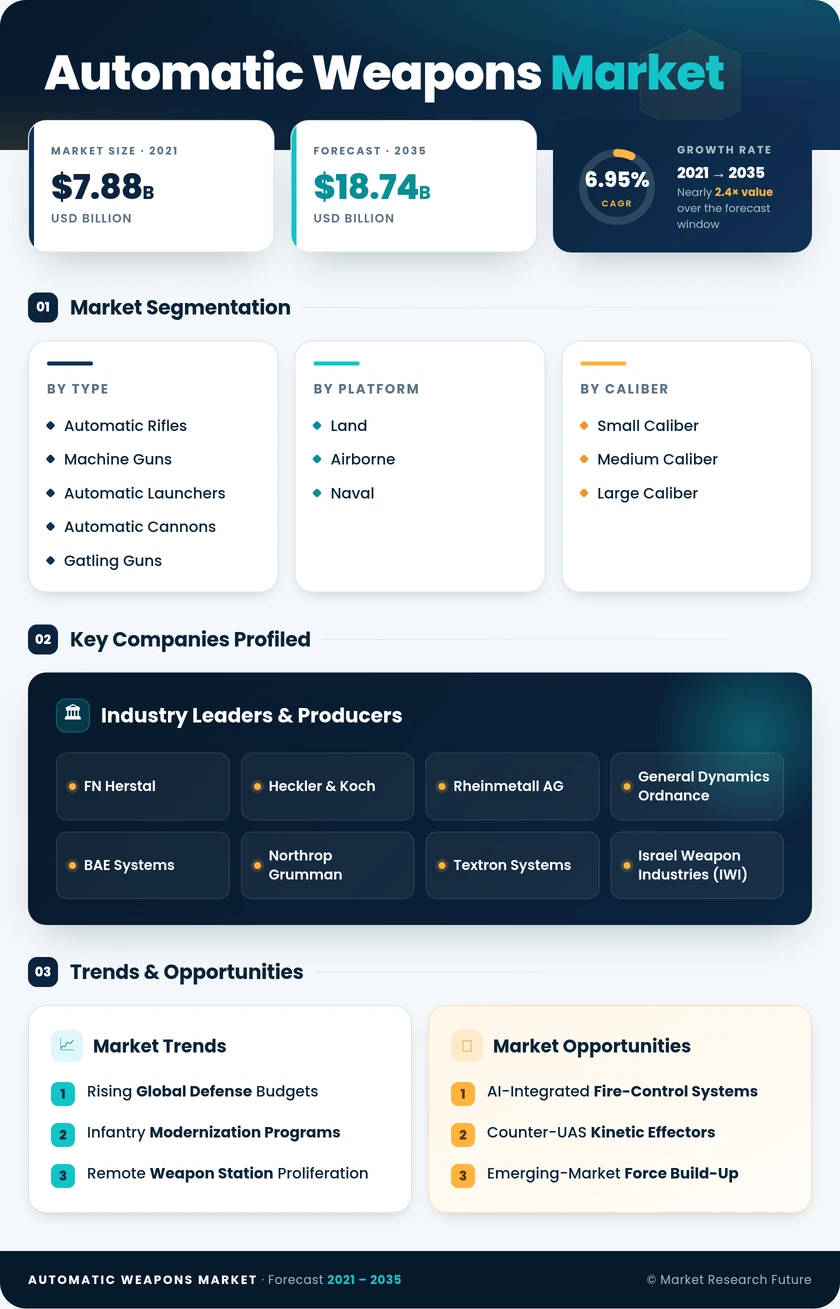

| By Type | Automatic Rifles, Machine Guns, Automatic Launchers, Automatic Cannons, Gatling Guns | Automatic Rifles (38.40% share, 2025) | Automatic Cannons (8.98% CAGR) |

| By Platform | Land, Airborne, Naval | Land (62.30% share, 2025) | Naval (9.70% CAGR) |

| By Caliber | Small Caliber, Medium Caliber, Large Caliber | Small Caliber (43.90% share, 2025) | Large Caliber (8.72% CAGR) |

| By End User | Defense, Law Enforcement | Defense (72.90% share, 2025) | Law Enforcement (higher growth off a smaller base) |

| By Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (35.40% share, 2025) | Asia-Pacific (9.40% CAGR) |

Market Segmentation Overview

By Type

| Sub-Segment | Key Trend |

| Automatic Rifles | Generational replacement cycles (NGSW, HK416 family adoption) are driving sustained volume. |

| Machine Guns | Continued demand for 7.62 mm and 12.7 mm belt-fed systems in mounted and dismounted roles |

| Automatic Launchers | Integration of 40 mm automatic grenade launchers into IFV and naval turret architectures |

| Automatic Cannons | Counter-UAS mission requirements and remote weapon station proliferation are accelerating adoption. |

| Gatling Guns | Niche high-rate-of-fire applications on helicopters, close-in weapon systems, and special-operations platforms |

The type segmentation of the Automatic Weapons Market reflects a clear distinction between high-volume infantry platforms (automatic rifles and machine guns) and high-value vehicle-mounted or naval systems (automatic cannons and Gatling guns). Growth momentum is shifting toward the latter category as platform-integrated, digitally networked weapon systems capture an increasing share of defense budgets.

By Platform

| Sub-Segment | Key Trend |

| Land | Armored-vehicle modernization programs and dismounted infantry re-equipping globally |

| Airborne | Helicopter gunship and tiltrotor door-gun replacement cycles |

| Naval | Corvette, frigate, and OPV fleet expansions across Indo-Pacific and Gulf navies |

Land platforms dominate the Automatic Weapons Market by platform. Still, the naval segment is growing fastest as maritime-security priorities intensify across the Indo-Pacific, the Arabian Gulf, and the Baltic Sea. New-build warships increasingly specify automatic-cannon turrets with programmable ammunition capability for multi-role engagements.

By Caliber

| Sub-Segment | Key Trend |

| Small Caliber (≤12.7 mm) | Volume-driven by infantry rifles and light machine guns; caliber transition from 5.56 mm to 6.8 mm underway |

| Medium Caliber (>12.7 mm – 40 mm) | Core IFV and RWS caliber range: 30 mm and 40 mm families gaining share |

| Large Caliber (>40 mm) | Naval CIWS and ground-based air-defense cannon are driving the fastest growth rate. |

Caliber segmentation within the Automatic Weapons Market tracks closely with platform trends: small caliber aligns with infantry, medium caliber with armored vehicles, and large caliber with naval and air-defense applications. The ongoing debate around optimal intermediate calibers — exemplified by the 6.8 mm transition — will reshape supply chains through the 2030s.

By End User

| Sub-Segment | Key Trend |

| Defense | National armed forces account for the overwhelming majority of procurement spend. |

| Law Enforcement | Growing paramilitary and border-security demand in Latin America, Asia, and Africa |

Defense remains the primary end-user segment of the Automatic Weapons Market, reflecting the capital-intensive nature of military procurement cycles and the volume requirements of national armed forces. Law enforcement demand is rising as governments expand paramilitary border-security and counter-narcotics capabilities, though it remains a fraction of military spending.

By Geography

| Sub-Segment | Key Trend |

| North America | Largest regional market; NGSW rollout and C-UAS investment sustain dominance |

| Europe | Post-2022 rearmament wave driving accelerated procurement across NATO Europe. |

| Asia-Pacific | Fastest-growing region: India, Japan, South Korea, modernization cycles |

| South America | Counter-narcotics and border-security funding underpin steady but modest growth. |

| Middle East & Africa | Gulf-state defense localization and conflict-driven procurement in Sub-Saharan Africa |

North America leads the Automatic Weapons Market by regional share, backed by the world's largest single-country defense budget and a mature domestic industrial base. Asia-Pacific is the fastest-growing region, powered by multi-decade rearmament programs in India, Japan, and South Korea that are creating new production ecosystems and export competitors within the global Automatic Weapons Market.