Automotive Aftermarket Industry Market Summary

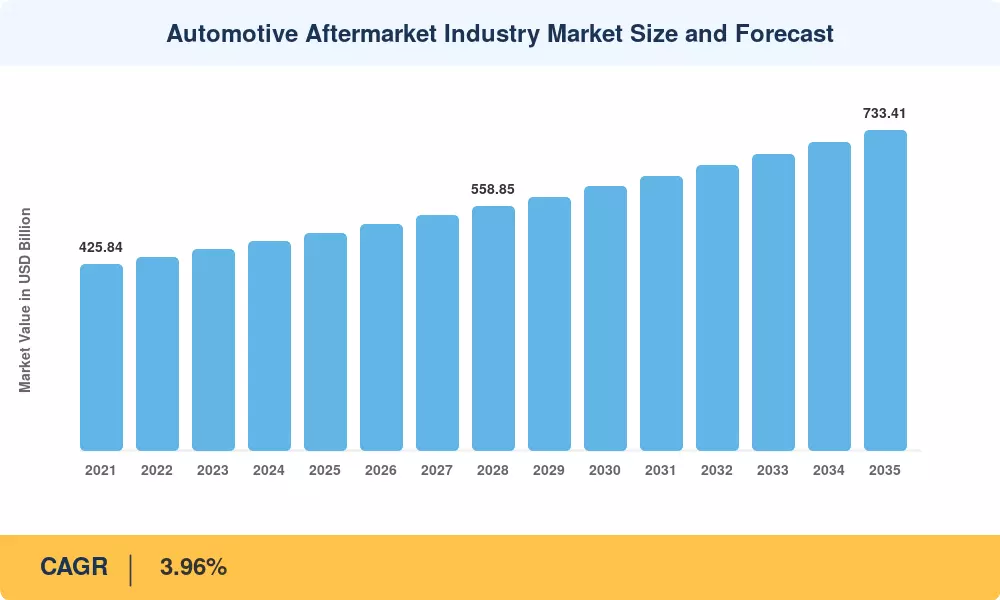

The Automotive Aftermarket Market reached an estimated USD 497.40 Billion in 2025 and is projected to expand from USD 517.09 Billion in 2026 to USD 733.41 Billion by 2035, registering a CAGR of 3.96% during the forecast period (2026–2035). An aging global vehicle parc — now exceeding 1.5 billion units — drives persistent demand for OEM vs aftermarket parts replacement, while digitization of procurement channels reshapes how shops and consumers source components. Government mandates for periodic vehicle inspections in the EU, India, and several U.S. states reinforce replacement cycles and sustain aftermarket revenue visibility.

A technology transformation is rewriting the rules of the Automotive Aftermarket Market. Legacy brick-and-mortar distribution is steadily yielding ground to aftermarket e-commerce platform online models, with digital parts sales crossing USD 72 Billion globally in 2024, according to the Automotive Aftermarket Suppliers Association [3]. Predictive maintenance platforms, powered by OBD-II telematics and cloud diagnostics, are converting reactive repairs into planned service events — a shift that favors independent aftermarket repair shop networks investing in connected tools. At the same time, EV aftermarket service battery motor work is emerging as a high-value niche as global EV parc penetration climbs past 6% [4].

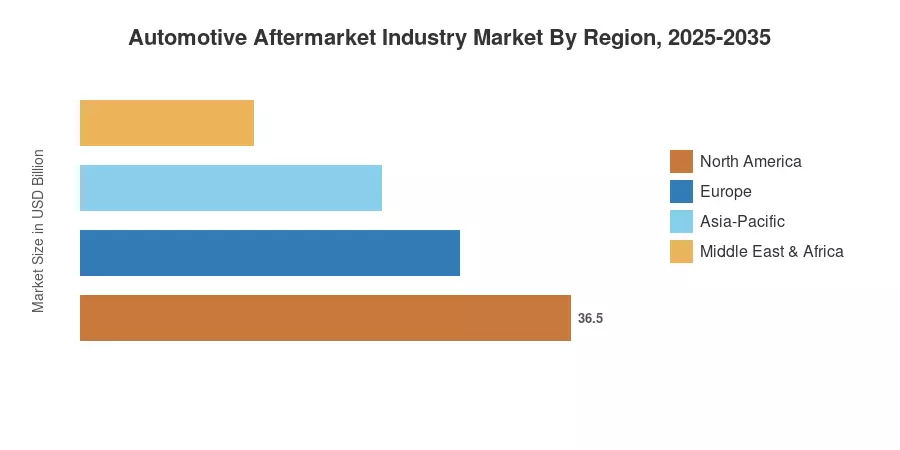

Asia-Pacific commands the dominant share of the Automotive Aftermarket Market at roughly 40.65% of 2024 revenue, driven by surging vehicle registrations in China, India, and ASEAN markets The region also posts the fastest CAGR at 4.02%. North America follows as the second-largest region, contributing approximately 26% of global aftermarket spending, supported by a mature automotive aftermarket distribution channel infrastructure and a vehicle fleet averaging 12.6 years of age [5]. Europe maintains strong value through stringent MOT and emissions-testing regimes. Looking ahead, rising two-wheeler populations in Southeast Asia and Sub-Saharan Africa position these geographies for outsized medium-term growth.

Key Report Takeaways — Automotive Aftermarket Market

By Replacement Part

- Tires held approximately 23.18% of the Automotive Aftermarket Market share in 2024, reflecting high wear-and-replace frequency across all vehicle segments

- Electronics components are projected to grow at a 4.01% CAGR through 2035, spurred by ADAS sensor replacement and infotainment upgrades

By Service Channel

- Independent aftermarket repair shop networks captured about 46.48% of service revenue in 2024, leveraging cost advantages and local proximity

- Fleet maintenance providers record the strongest projected growth within the Automotive Aftermarket Market at a 4.10% CAGR through 2035

By Distribution Channel & Vehicle Type

- Retailers represented approximately 51.35% of aftermarket distribution in 2024, though aftermarket e-commerce platform online sales are advancing at a 4.04% CAGR

- Passenger cars commanded around 54.84% of the Automotive Aftermarket Market in 2024, while two-wheelers are forecast to grow the fastest at a 4.06% CAGR

By Region

- Asia-Pacific accounted for 40.65% of the global Automotive Aftermarket Market in 2024, with a 4.02% CAGR — the highest among all regions

- North America contributed roughly USD 129.32 Billion in 2024, anchored by mature independent aftermarket repair shop density

Automotive Aftermarket Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue analysis from distributor, retailer, and e-commerce transaction data with top-down cross-checks against OE production volumes, vehicle parc aging curves, and per-vehicle aftermarket spend benchmarks. MRFR triangulated figures using trade association data (AASA, MEMA, FIGIEFA), customs databases, and proprietary supply-chain surveys conducted across 32 countries[6].