Automotive Backup Camera Market Summary

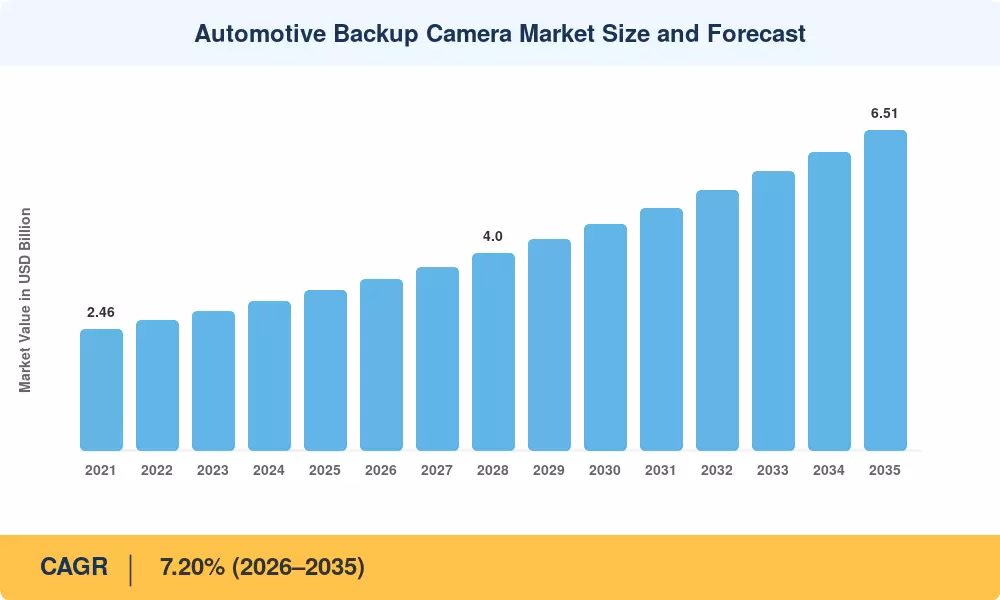

The Automotive Backup Camera Market reached USD 3.25 Billion in 2025 and is set to climb to USD 6.51 Billion by 2035, registering a 7.20% CAGR across the 2026–2035 forecast window. Two catalysts anchor that trajectory: the U.S. FMVSS No. 111 rearview backup camera regulation mandate, which made rear-visibility systems compulsory for all new light vehicles sold after May 2018, and the European Union's General Safety Regulation 2019/2144, which extended similar obligations to heavy commercial vehicles from July 2024 [1]. Together, these policies converted what was once a convenience option into a baseline safety requirement.

The supply side is changing as a result of technology migration. High-resolution CMOS arrays that can provide a wide angle backup camera 180 degree field of view, low-light dynamic range, and pixel-level object categorization are gradually replacing the legacy CCD modules that were the norm ten years ago. In order to enable night vision backup camera infrared overlays without the need for separate ECU hardware, Tier-1 vendors like Bosch and Continental are directly integrating perception algorithms into camera system-on-chip platforms [2]. Reversing feeds now share screen space with surround-view stitching and automated parking guidance in the backup camera display OEM head unit.

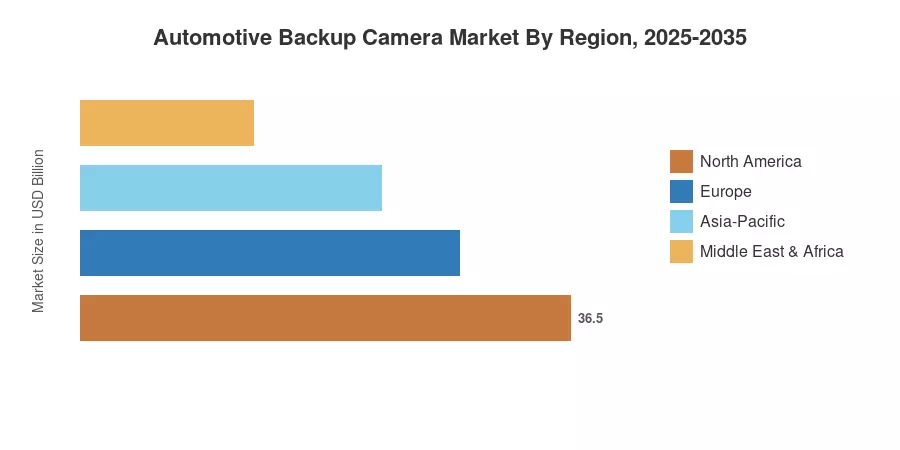

North America's sophisticated rearview backup camera regulations and high pickup truck penetration, which fuel demand for trailer hitch backup camera system accessories, support the region's about 36.8% share of the worldwide automotive backup camera market. With an 8.50% CAGR, the Middle East and Africa market is expanding at the quickest rate as Gulf Cooperation Council nations implement rear-visibility regulations akin to those in Europe [3]. Europe has the second-largest share thanks to fleet-electrification incentives that speed up cockpit digitization and strict type-approval regulations. Growing aftermarket usage and wireless backup camera kit retrofit activities in emerging nations over the next ten years should maintain robust demand until 2035.

Key Report Takeaways

• By Product Type

- Wired backup camera systems held approximately 58% of the Automotive Backup Camera Market in 2024, reflecting their cost advantage in OEM assembly lines

- Wireless systems are projected to expand at a 10.60% CAGR through 2035, fueled by wireless backup camera kit retrofit demand in the aftermarket channel

• By Vehicle Type

- Passenger cars represented the dominant volume category in 2024, driven by universal rearview backup camera regulation mandate compliance

- Heavy commercial vehicles are growing at a 9.30% CAGR, the fastest clip within the Automotive Backup Camera Market vehicle-type dimension

• By Technology

- CMOS sensor cameras captured 72.5% of unit shipments in 2024, offering superior wide angle backup camera 180 degree imaging at lower silicon cost

- Infrared and night vision backup camera infrared variants register the highest projected CAGR at 11.20% through 2035

• By Sales Channel

- OEM fit accounted for roughly 63.8% of Automotive Backup Camera Market revenue in 2024

- The aftermarket channel is advancing at a 12.30% CAGR, propelled by insurance-premium incentives and wireless backup camera kit retrofit adoption

• By Regional

Market Size and Forecast (2021–2035)

MRFR's estimates blend bottom-up supplier shipment data with top-down vehicle production forecasts from OICA and national registration databases. Historical years (2021–2024) reflect audited trade statistics; 2025 is the calibrated base year, and 2026–2035 values are derived from a compound growth model anchored to the 7.20% CAGR.