Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Product Type | Wired Systems; Wireless Systems | Wired Systems | Wireless Systems |

| Vehicle Type | Passenger Cars; Light Commercial Vehicles (LCVs); Heavy Commercial Vehicles (HCVs) | Passenger Cars | Heavy Commercial Vehicles |

| Automotive Backup Camera Market | CMOS Sensor Cameras; CCD Sensor Cameras; Infrared Cameras | CMOS Sensor Cameras | Infrared Cameras |

| Sales Channel | OEM Fit; Aftermarket | OEM Fit | Aftermarket |

| Geography | North America; Europe; Asia-Pacific; South America; Middle East & Africa | North America | Middle East & Africa |

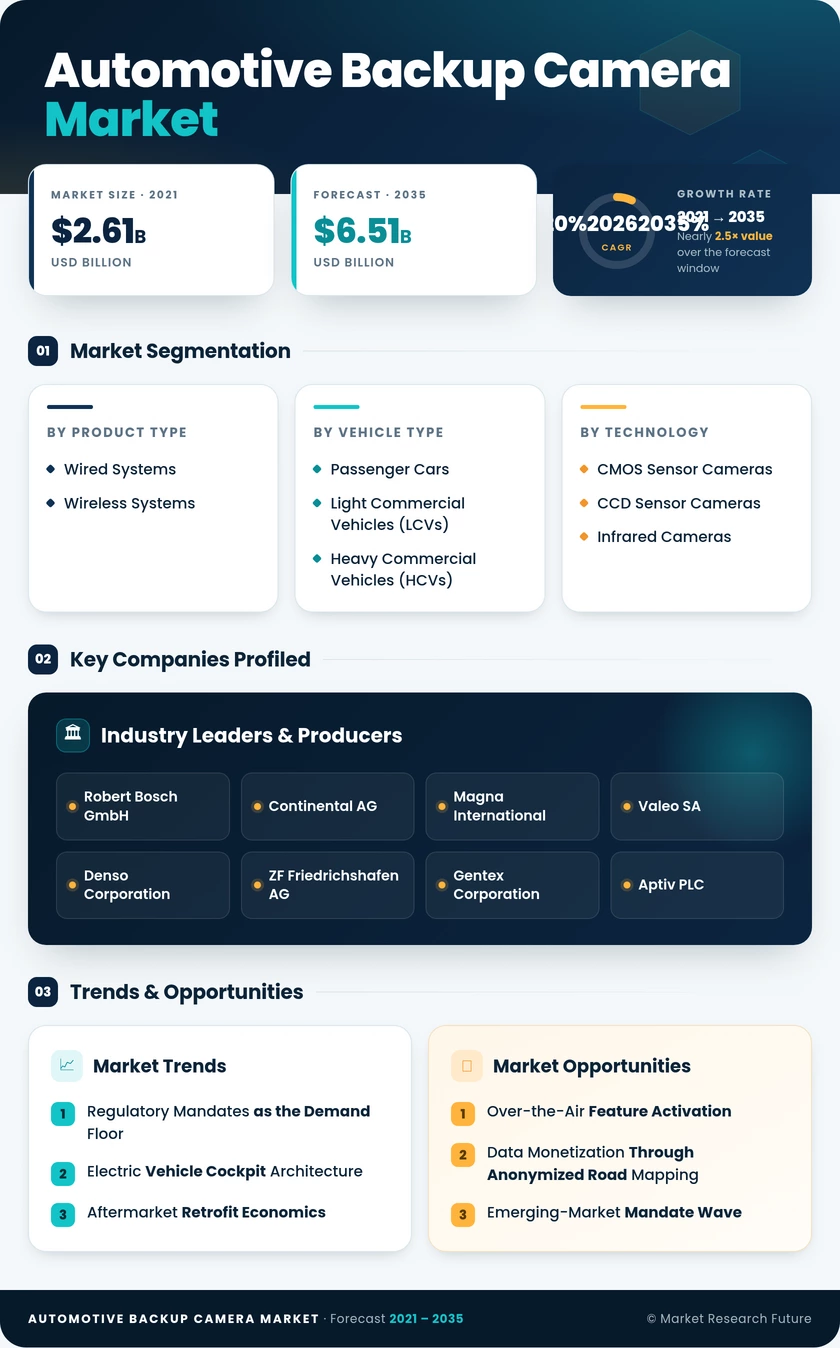

Market Segmentation Overview

By Product Type

| Sub-Segment | Key Trend |

| Wired Systems | Cost-optimized analog modules remain default on high-volume OEM platforms; declining share as EV architectures shift to digital links |

| Wireless Systems | Rapid aftermarket uptake driven by wireless backup camera kit retrofit demand; latency gap narrowing with Wi-Fi 6 chipsets |

Wired systems continue to anchor OEM production lines due to mature tooling and proven reliability, but the wireless segment is closing the gap as electric-vehicle zone architectures reduce wiring complexity and aftermarket consumers prioritize easy self-installation.

By Vehicle Type

| Sub-Segment | Key Trend |

| Passenger Cars | Universal mandate compliance ensures near-100% fitment on new models globally |

| Light Commercial Vehicles (LCVs) | Last-mile delivery fleet expansion increases camera attach rates |

| Heavy Commercial Vehicles (HCVs) | EU GSR Phase II and GCC mandates creating a new compliance wave |

Passenger cars represent the largest installed base by far, yet the heavy-commercial segment is expanding fastest as regulators extend rear-visibility mandates beyond light vehicles into trucks, buses, and specialized construction equipment.

By Automotive Backup Camera Market

| Sub-Segment | Key Trend |

| CMOS Sensor Cameras | Dominant imaging platform with wide angle backup camera 180 degree capability at low BOM cost |

| CCD Sensor Cameras | Legacy technology in gradual decline; sustained by replacement cycles in older fleets |

| Infrared Cameras | Premium night vision backup camera infrared modules gaining traction in ADAS bundles |

CMOS sensors dominate because they deliver high resolution, low power consumption, and on-chip signal processing on a single die. Infrared variants occupy the premium tier and are expected to see the fastest growth as costs decrease and OEMs expand night-vision feature availability.

By Sales Channel

| Sub-Segment | Key Trend |

| OEM Fit | Mandate-driven standard fitment on all new vehicles; backup camera display OEM head unit integration deepening |

| Aftermarket | Aging parc and insurance incentives driving wireless backup camera kit retrofit adoption at double-digit growth rates |

OEM fit accounts for the majority of revenue because regulatory mandates require factory installation. The aftermarket channel is the faster-growth story, fueled by hundreds of millions of pre-mandate vehicles in operation and a growing ecosystem of plug-and-play camera kits.